Switching car insurance can deliver genuine savings, but the actual amount depends on a calculation most guides skip entirely: accounting for cancellation fees, maintaining coverage equivalency, and understanding break-even timing. This article walks through the exact steps to calculate your true net savings, the variables that influence the outcome, and the mistakes that lead to false conclusions.

Key Takeaways

- Calculating real savings requires four inputs: your current annual premium, a like-for-like quote, any cancellation fee, and the break-even timeline

- Long-term customers overpay by an average of 2.400 kr. per year after 10 years — a direct result of loyalty penalties from their insurer

- The most expensive quote can cost 60% more than the cheapest for identical coverage

- Mid-policy switching only makes sense when net annual savings exceed exit costs

- Manual comparison takes 10+ hours; AI-driven analysis tools cut that to 60 seconds

How to Calculate Your Car Insurance Savings: 4 Steps

Step 1: Document Your Current Policy and True Annual Cost

Pull out your declarations page and note your exact annual premium. If you pay monthly, multiply that amount by 12 — this is your baseline, and it must reflect what you actually pay, not a marketing estimate or introductory rate.

Record your coverage details precisely:

- Liability limits: The DKK amounts for bodily injury and property damage

- Deductible amounts: What you pay out-of-pocket before coverage applies

- Coverage tier: Liability-only (ansvarsforsikring), partial comprehensive (delkasko), or full comprehensive (kasko)

- Optional add-ons: Roadside assistance, replacement vehicle, glass coverage, young-driver extensions

These details are essential for a direct comparison in Step 2. Changing any parameter invalidates your savings estimate.

Check how long you've been with your current insurer. Research from the Danish Competition and Consumer Authority found that customers with 10+ years of tenure pay a margin 7–8 percentage points higher than new customers for identical car, home, and contents insurance. In some cases, loyalty penalties on home and contents policies reach 30–35 percentage points. This "loyalty penalty" is a key indicator that savings potential exists.

Step 2: Gather Like-for-Like Comparison Quotes

Request quotes from at least three different insurers using the exact same coverage limits, deductibles, and add-ons you documented in Step 1. Any deviation makes your savings estimate unreliable.

Tools for gathering quotes:

- Direct insurer websites (Tryg, Topdanmark, Alka, Codan, GF, Alm. Brand) — slower, but produce binding quotes

- Comparison platforms — faster, though coverage of all insurers varies

- AI-powered policy analysis tools — upload your existing policy document (PDF or photo) and get a market price assessment in around 60 seconds, replacing hours of manual research

Testing by Forbrugerrådet Tænk showed that the most expensive car insurance quote can cost 60% more than the cheapest for comparable coverage across different customer profiles. The same test found no direct correlation between price and coverage quality, meaning higher cost doesn't guarantee better protection.

Record the lowest equivalent quote you find. This is your "New Annual Premium" figure for the final calculation.

Step 3: Calculate Your True Exit Cost

Contact your current insurer and ask directly whether they charge a cancellation fee and how it is calculated. Common structures include a flat fee or, less commonly, a percentage of your remaining unused premium.

Typical Danish cancellation fee ranges:

- Industry guidance suggests approximately DKK 60 per policy for standard cancellations

- First-year cancellations can incur higher fees — Tryg charges DKK 74 base fee plus DKK 810 for car policies cancelled within the first year

- At normal renewal, cancellation is free

If you paid your premium upfront, ask whether you're entitled to a pro-rata refund on unused months. Danish Insurance Contracts Act §16 mandates that insurers may only keep the portion of premium corresponding to time on risk, meaning unused months must be returned.

Subtract any refund from the cancellation fee to arrive at your net exit cost — in some cases, the refund can turn a fee into a net benefit.

If you have bundled home and car insurance, check whether splitting the bundle will cause your home policy premium to increase. Bundle discounts in Denmark range widely:

- Topdanmark: 8% with 2 policies, 12% with 3

- Tryg: 10% with 3 policies, 15% with 4, 20% with 5

- If: up to 15% bundle savings

If breaking the bundle removes a discount, add the resulting home insurance increase to your exit cost before calculating savings.

Step 4: Apply the Break-Even Formula

The savings formula is:

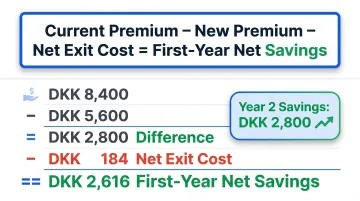

(Current Annual Premium − New Annual Premium) − Net Exit Cost = First-Year Net Savings

Example:

- Current annual premium: DKK 8,400

- New annual premium: DKK 5,600

- Cancellation fee: DKK 884 (base DKK 74 + first-year DKK 810)

- Pro-rata refund: DKK 700 (one month unused)

- Net exit cost: DKK 184 (DKK 884 − DKK 700)

- First-year net savings: DKK 2,616 (DKK 2,800 difference − DKK 184 exit cost)

Introduce the break-even timeline calculation:

Break-Even Months = Net Exit Cost ÷ Monthly Savings

Using the example above: DKK 184 ÷ DKK 233/month = 0.8 months

If your policy renewal is two months away and the break-even is three months, waiting until renewal costs you one month of savings but avoids exit fees entirely. You must weigh the trade-off.

First-year savings and ongoing savings differ. The exit cost is one-time, so savings in Year 2 and beyond equal the full annual premium difference. In the example, Year 2 savings jump to the full DKK 2,800. If the monthly saving looks small, the multi-year total often makes the case clearly.

Key Variables That Change How Much You Actually Save

The same switching process produces wildly different savings for different drivers. Four variables consistently explain why — and knowing which ones apply to you determines how hard you should push to compare.

How Long You've Been with Your Current Insurer

Insurers price new customers competitively to win market share but raise renewal rates incrementally for existing customers. The longer you've stayed, the larger the gap between what you pay and what the market would charge a new customer for identical coverage.

KFST data shows long-term customers (10+ years) pay 7–8 percentage points higher margins than new customers, with some insurers charging 30–35 percentage points more for certain coverage types. Five or more years without comparing? Your savings potential is likely higher than you'd expect.

Your Coverage Type and Deductible Level

The premium gap between insurers is largest for comprehensive (kasko) and full-coverage policies. Liability-only policies have smaller absolute differences.

Deductible level adds another layer. Raising yours (say, from DKK 2,000 to DKK 5,000) when switching can amplify premium savings — but also increases your out-of-pocket exposure in a claim. A lower premium means nothing if you can't cover the deductible when you need it.

Your Risk Profile at the Time of Comparison

Your current insurer's renewal price reflects your history with them — not necessarily who you are today. A recently cleared driving record, reduced annual mileage, or improved payment history can make you a better risk to a new insurer than when you first signed.

New insurers price based on your current profile — so timing matters. Profile improvements that count in your favor:

- Two or more clean years since your last claim

- Meaningfully lower annual mileage than when you first enrolled

- Improved payment history in markets where insurers factor this in

Bundling and Multi-Policy Discounts

Many drivers receive a discount for bundling home, contents, and car insurance with one provider. KFST found that 92–93% of multi-policy customers keep all policies at one company — making bundling one of the most effective retention tools insurers use.

The correct calculation compares total insurance costs across all policies, not just the car premium in isolation. If breaking a bundle removes a 12% discount from your home insurance, that cost belongs in your switching calculation too.

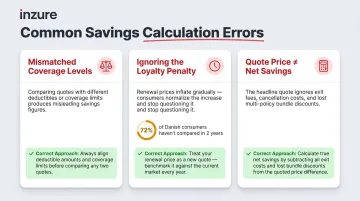

Common Mistakes That Distort Your Savings Estimate

Three errors account for most inflated or misleading savings estimates. Knowing them before you run the numbers prevents a false conclusion from driving a bad decision.

Comparing premiums at different coverage levels. The most common error is accepting a lower quote that carries a higher deductible, lower liability limits, or missing add-ons. This inflates apparent savings while reducing actual protection. Verify that every parameter matches before calculating the difference.

Ignoring the loyalty penalty in your baseline. Many policyholders underestimate how much they're overpaying because they've normalized the cost over time. Long-term customers are systematically overcharged — and most never check. 72% of Danish consumers had neither considered switching, obtained a quote, nor switched any private insurance in the last two years, according to the Danish Competition and Consumer Authority.

Calculating savings from the quote, not the net cost. A lower monthly premium does not equal net savings if you're paying a cancellation fee, losing a bundling discount, or forfeiting a pro-rata refund. The real savings figure only emerges after all exit costs are subtracted from the premium difference.

When Switching Makes Financial Sense (and When to Wait)

Situations where switching is clearly worthwhile:

- Your rate increased at renewal without any change in your driving record or claims history

- You've been with the same insurer for more than two years and have never compared quotes

- Your break-even point is less than six months away

- You've had a meaningful profile improvement (clear record, reduced mileage) that your current insurer hasn't reflected in your price

Situations where it makes sense to wait:

- Your cancellation fee exceeds six months of projected savings

- You have an open claim; a pending claim can affect how a new insurer prices your policy

- Your policy renewal is within 30 days, at which point waiting costs nothing and avoids exit fees entirely

A simple rule of thumb: if your first-year net savings exceed two months of your current premium, switch now. If not, set a calendar reminder to shop 30 days before your next renewal — you'll avoid exit fees entirely and still capture the savings.

Frequently Asked Questions

How does switching insurance work?

Switching involves buying a new policy first, then cancelling the old one. The process typically takes under an hour. The new policy must be active before canceling the old one to avoid a coverage gap, as Danish law requires continuous motor liability coverage.

What is the 80/20 rule in insurance?

In the insurance context, the 80/20 rule often refers to coinsurance requirements, where insurers expect coverage for at least 80% of a property's replacement value. It has limited relevance to standard car insurance premium calculations.

What does 250/500/100 mean in insurance?

This notation is used in US markets to describe liability coverage limits and is not applicable in Denmark. Danish minimum motor liability insurance must cover at least DKK 153 million per accident for personal injury and DKK 30 million for property damage.

Will switching car insurance affect my credit score?

Insurers in Denmark may check payment history through RKI (credit registry), but quoting alone does not affect your credit standing. Compulsory motor liability insurance must be offered regardless of RKI registration status.

When is the best time of year to switch car insurance?

The cleanest time to switch is at renewal, avoiding cancellation fees entirely. However, switching mid-policy is worthwhile when the break-even calculation confirms net savings within six months.

Can I switch car insurance if I have an open claim?

You can, but waiting until the claim is resolved is the better move. A pending claim can push up your new insurer's pricing, and having an active claim span two insurers creates disputes over which policy applies.