Introduction

In Denmark, loyal insurance customers pay 7-8 percentage points more than new customers for identical coverage. The industry hasn't built this complexity by accident — it's the business model.

This guide is for anyone with home, travel, or accident insurance who's seen an unexplained premium increase, received poor service, or simply suspects they're overpaying. We'll cover when to switch, how to do it step by step, what to compare, and which mistakes to avoid.

Switching is simpler than most people expect. Insurance companies count on you not knowing that.

Key Takeaways

- You can switch insurance at any time, not just at renewal

- The process: review your current policy, gather quotes, secure new coverage, then cancel the old one

- Never cancel before securing new coverage to avoid gaps

- Danish law guarantees a pro-rata refund on any unused premium when you cancel

- Bundling all policies with one insurer isn't always the cheapest option — splitting across providers can save more

When Is It Time to Switch Insurance Companies?

The Loyalty Penalty: Why Long-Term Customers Pay More

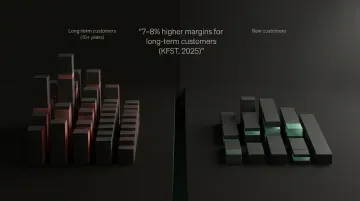

The Danish Competition and Consumer Authority (KFST) confirmed in 2025 that customers who stay with the same insurer for 10+ years pay 7-8 percentage points higher margins than new customers for identical coverage. Insurers price this in deliberately.

Danish home and contents insurance prices have risen 45% more than the EU average since 1996. Most of that increase comes from automatic annual indexation tied to wage growth — adjusted each year without a separate notification, so your bill climbs while your coverage stays identical.

Common Triggers for Switching

Switch when you notice:

- Premium increases at renewal without explanation

- Life changes: moving house, marriage, new valuables

- Poor claims handling or customer service

- No price comparison done in the past 12 months

- Five or more years with the same insurer

There's no fixed schedule. Switch when the numbers justify it — and the sections below show you exactly how to do that without gaps in coverage.

How to Switch Insurance Companies: Step by Step

The full process takes 30 minutes to a few days, depending on your preparation and insurance type. Work through each step below to avoid gaps, fees, and coverage surprises.

Step 1: Review Your Current Policy

Before shopping, know what you have. Locate your policy documents and note:

- Coverage types and limits (what's covered, maximum payouts)

- Deductibles (your out-of-pocket cost before insurance activates)

- Annual premium and renewal date

- Cancellation terms and any fees

Your policy documents must state all of this. If details are unclear, contact your insurer directly.

Step 2: Identify What You Actually Need

Your coverage needs shift over time. Income changes, family size evolves, asset values increase, and risk profiles adjust. Switching to a cheaper policy that no longer matches your situation creates dangerous gaps.

Ask yourself:

- Has my home's value increased since I first insured it?

- Do I have new valuables (electronics, jewelry, bikes) not covered?

- Have I added family members who need coverage?

- Has my travel frequency changed?

Step 3: Gather Quotes from Multiple Providers

Compare at least three quotes—this is the minimum to understand market pricing. Use identical coverage levels and deductibles across quotes to ensure apples-to-apples comparison.

Critical: A 1,500 kr cheaper premium means nothing if the deductible jumps from 2,500 kr to 5,000 kr. You'll pay more out of pocket when you actually need to claim.

Tools like Inzure can scan your existing policy in 60 seconds and benchmark it against the Danish market, showing whether you're overpaying, have duplicate coverage, or critical gaps—before you invest hours researching quotes manually.

Step 4: Buy Your New Policy Before Canceling the Old One

The rule is simple: never create a coverage gap. Have your new policy active before canceling the current one.

Even a one-day gap can result in:

- Higher future premiums (insurers penalize coverage gaps)

- Rejected claims (no coverage = no payout)

- Legal exposure (mandatory insurance like home contents tied to mortgages)

Coordinate the timing so your new policy starts the day your old one ends.

Step 5: Cancel Your Old Policy Properly

Your new insurer cannot cancel your old policy—this is your responsibility.

How to cancel correctly:

- Contact your old insurer in writing (email creates a paper trail)

- Request written confirmation of cancellation and the effective date

- Ask about your refund for unused premium

Under Danish law (Forsikringsaftaleloven §16), insurers must refund the unused portion of your premium when you cancel mid-term. If you cancel at renewal, cancellation is free with one month's notice.

Mid-term cancellation fees:

- Customer for 1+ years: ~60 kr administrative fee

- Customer for less than 1 year: up to 500 kr fee

Step 6: Notify Relevant Third Parties

Some third parties must know about your switch:

Mortgage lenders — If home insurance is tied to an escrow account, notify your lender immediately. Under Forsikringsaftaleloven §86-87, cancellation only takes effect for the mortgagee 14 days after they receive notification.

Financing companies — If you have loans or leases requiring specific insurance, inform the lender and provide new policy details.

Missing this step can trigger forced insurance policies (which the lender buys for you at inflated rates) or contract violations.

What to Compare Before Switching

Price is visible, but coverage quality determines whether a policy actually protects you.

Coverage Limits, Deductibles, and Exclusions

Coverage limits set the ceiling on payouts. A policy capping home contents at 100,000 kr looks fine until you need to replace 150,000 kr worth of belongings after a fire.

Deductibles determine your out-of-pocket cost when something goes wrong. Choosing a 7,500 kr deductible over 2,500 kr to lower your premium means paying 5,000 kr more every time you file a claim.

Exclusions are where policies quietly diverge. Two policies at identical prices can differ dramatically — one might exclude water damage entirely, the other cover it fully.

Claims Handling Reputation

In 2024, Denmark's Ankenævnet for Forsikring received 1,898 complaints about claim disputes. Claims service quality varies widely between providers — some pay quickly and fairly, others dispute aggressively.

Before switching, research:

- Average claim processing time

- Complaint rates and resolution outcomes

- Customer reviews specifically about claims (not sales)

The Bundling Trap: When "Discounts" Cost More

Insurers heavily market "samlerabat" (bundling discounts), but Forbrugerrådet Tænk found that bundling home, car, accident, and contents insurance with one provider costs up to 5,700 kr more per year than splitting policies across the cheapest individual providers.

Bundling benefits the insurer by locking you in — not necessarily your wallet. Always compare:

- Total cost of bundled policies with current provider

- Total cost of best individual policies from different providers

Using AI Analysis to Benchmark Before Shopping

Before spending hours gathering quotes, it helps to know exactly what your current policy is — and isn't — doing for you. Tools like Inzure upload and analyze your policy documents in 60 seconds, surfacing:

- Overpayment relative to current market rates

- Duplicate coverage across multiple policies

- Gaps where you're underinsured

That baseline tells you what to fix, not just what to replace.

Common Mistakes and Misconceptions About Switching Insurance

Misconception: Switching Is Difficult or Penalized

Most switches take under an hour. Cancellation fees are minor (60 kr for established customers) or non-existent, and Danish law guarantees your right to cancel at almost any time with a pro-rata refund. Insurers profit when you assume switching is complicated — but the process is straightforward once you know the steps.

Switching on Price Alone Without Checking Coverage

A new policy with a 20% lower premium might include:

- 50% higher deductibles

- Lower coverage limits

- More exclusions (water damage, theft, liability caps)

These differences only surface at claims time, which is exactly when you can't fix them.

The Open Claims Myth

Many believe you cannot switch insurers during an active claim. This is false.

Your current insurer must process claims filed during your active policy period, even after cancellation. However, some new insurers delay coverage activation until existing claims resolve.

Best practice: Wait until major claims settle before switching. For minor claims, confirm your new insurer's policy on open claims before finalizing the switch.

When Switching Insurance May Not Be the Right Move

Large Cancellation Fees vs. Small Savings

If you're canceling within your first year and face a 500 kr fee, switching to save 300 kr annually doesn't make financial sense. Calculate total first-year cost including fees.

Losing Valuable Loyalty Benefits

Some insurers offer genuine loyalty benefits:

- Accident forgiveness (first accident doesn't raise premiums)

- Vanishing deductibles (deductible decreases annually without claims)

- Member bonuses (customer-owned mutuals like TryghedsGruppen pay annual profit-sharing bonuses)

If TryghedsGruppen pays you a 1,000 kr annual bonus but switching saves 400 kr, you lose 600 kr net.

Bundling Discounts You'd Lose by Splitting Policies

Loyalty bonuses aren't the only hidden value worth protecting. If you currently bundle multiple policies with one insurer, splitting them might eliminate multi-policy discounts that offset savings on individual products. Always calculate total cost across all policies before deciding.

Switching Too Frequently

Switching too often can work against you. Some Danish insurers factor frequent switching history into their risk profiling, which may affect the rates you're offered. A practical rule of thumb:

- Wait at least 12 months between switches

- Only switch sooner if your circumstances change significantly (new home, life event, major price hike)

- Review your policies annually rather than reacting to every new offer

Frequently Asked Questions

How do I switch from one insurance company to another?

Review your current policy, gather quotes from at least three providers, purchase your new policy first, then cancel the old one in writing. Most people complete the process in under an hour once they've gathered quotes.

How long does it take to switch insurance providers?

New policies often start the same day you purchase them. The full process from research to receiving cancellation confirmation typically takes a few days to a week, depending on insurance type and how quickly you gather quotes.

Do you get penalized for switching insurance companies?

Many insurers charge no cancellation fees at all. Those that do typically charge modest amounts, and the savings from switching usually exceed them. Check your policy terms before assuming there's a cost.

What happens if I switch insurance companies during a claim?

Your current insurer must process any claim filed while your policy was active, even after cancellation. However, new insurers may delay coverage activation until open claims resolve, so waiting until the claim settles is usually the safer move.

Can you switch home insurance providers at any time?

Yes, home insurance can be switched at any time, not just at renewal. If your premiums run through a mortgage escrow account, notify your lender and share the new policy details. Note that cancellation takes effect for the mortgagee only after a 14-day notice period.

When should you change insurance companies?

Switch when you experience an unexplained premium increase at renewal, a significant life change, poor claims service, or discover you could get the same or better coverage for significantly less. Benchmark your policy against the market every 12-18 months to catch loyalty penalties early.