Introduction

A cycling accident on Kongens Nytorv. A slip on an icy staircase. A workplace fall that leaves you with a permanent injury. Accidents happen to anyone, at any time — and personal accident insurance (ulykkesforsikring) is what stands between you and serious financial hardship when they do.

Most Danes have heard of personal accident insurance, and many already pay for it. Yet very few actually know what their policy covers, what it excludes, or whether they're paying a fair price for it.

Even fewer realize they may already have accident coverage through their employer, trade union, or credit card — meaning they could be paying for duplicate protection without knowing it.

This guide delivers two promises: first, we'll demystify what personal accident insurance actually is and does. Second, we'll give you practical steps to avoid overpaying — because Danish insurers rarely volunteer the fact that loyal customers routinely pay 20–40% more than new ones for identical cover.

TLDR: Key Takeaways

- Personal accident insurance pays a lump sum for serious accidental injuries — it does not cover illness

- Many Danes already have partial coverage through employer schemes, unions, or credit card perks without realizing it

- Research shows switching penalties are rare, but silent annual premium increases still quietly push costs up

- Comparing policies and mapping your existing coverage is the most direct way to cut costs

What Is Personal Accident Insurance?

Personal accident insurance pays financial compensation if you experience a covered accidental injury — such as permanent disability, loss of a limb, or accidental death. It's distinct from health insurance (which covers medical treatment) or income protection insurance (which replaces lost earnings during illness or injury).

How Payouts Work in Denmark

Most policies offer a lump-sum payment based on injury severity, calculated as a percentage of the insured sum depending on your degree of permanent disability (invaliditetsgrad):

- Losing a finger: 5–10% payout

- Loss of a leg: 40–50% payout

- Full permanent disability: 100% payout

Some policies also cover temporary incapacity or medical costs directly caused by the accident, though this varies significantly between insurers.

The Key Distinction Many Danes Overlook

Personal accident insurance only covers accidental physical injury. Income protection (indkomstforsikring) covers both accidents and sickness. If you assume your accident policy pays out when you fall ill, you may be seriously underinsured.

Where Coverage Comes From

Coverage comes from four main sources in Denmark:

- Private insurers (Tryg, Alka, Topdanmark, and others)

- Employer group schemes (arbejdsgiverforsikring)

- Trade unions (fagforeninger)

- Bank account packages and credit card benefits

Many Danes end up paying for overlapping coverage without realising it — a costly gap worth checking.

Who Is Personal Accident Insurance Designed For?

The policy suits a wide range of people, but it's particularly relevant for:

- Families who need a financial safety net if a parent suffers a serious injury

- Freelancers and self-employed people without employer-provided coverage

- Anyone in physically demanding work — construction, trades, manual labour

- Active people who cycle regularly, play sport, or spend time outdoors

If you fall into one of these categories and don't have employer or union coverage, a standalone accident policy may fill a critical gap.

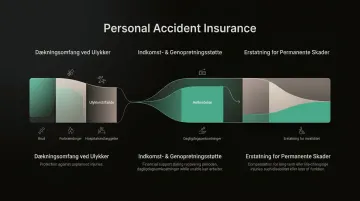

What Does Personal Accident Insurance Cover — and What Doesn't It?

Standard Coverage in Denmark

According to current Danish market standards, personal accident insurance typically covers:

- Permanent disability caused by an accident (with payout proportional to the degree of disability)

- Accidental death (lump sum paid to beneficiaries)

- Medical treatment costs directly caused by the accident (often subject to limits)

- Dental injuries resulting from accidents (e.g., broken teeth in a fall)

Critical Exclusions Most Consumers Overlook

What accident insurance does NOT cover:

- Illness and disease (including mental illness)

- Self-inflicted injuries

- Injuries sustained while under the influence of alcohol or drugs

- Injuries from certain high-risk activities or extreme sports (unless specifically added)

These exclusions are not hidden — they're in your policy terms. But few people read a 32-page policy document, which is exactly what insurers count on.

Understanding "Invaliditetsgrad" (Degree of Disability)

Payouts are proportional to the assessed degree of permanent disability. This means:

- Losing a finger: 5-10% of insured sum (e.g., DKK 5,000-10,000 on a DKK 100,000 policy)

- Losing full use of an arm: 60-70% of insured sum

- Full permanent disability: 100% of insured sum

Minor accident claims often result in smaller payouts than expected — disability assessments tend to be conservative by design.

Fine-Print Clauses That Vary Between Insurers

Not all policies are created equal. Watch for:

- Pre-existing conditions that quietly void a claim you assumed was covered

- Age cutoffs where coverage terminates or shrinks at 65 or 70 — often without a reminder

- Activity exclusions that remove coverage for specific sports or occupational risks unless you've paid to add them

Always read the exclusion list in your specific policy — or use an analysis tool that reads it for you.

Before buying additional coverage, though, it's worth checking whether you're already protected. Many Danes carry accident insurance they've never deliberately purchased.

Coverage You Might Already Have Without Knowing It

Common sources of existing accident coverage include:

- Employer group policies (arbejdsgiverforsikring): Most full-time employees are covered during work hours, and sometimes 24/7 — check your employment contract or HR documentation

- Trade union membership (fagforening): Unions like IDA, 3F, and HK include basic accident coverage as a standard membership benefit

- Premium bank accounts and credit cards: Gold and platinum cards often bundle worldwide accident insurance as a perk most cardholders never activate

Buying a standalone policy without checking these sources first means you could be paying twice for the same protection. Inzure's platform cross-references your existing policies against the full Danish market in 60 seconds — identifying exactly where you're double-covered and where you have genuine gaps.

Is Personal Accident Insurance Worth It?

There's no blanket yes or no answer — it depends on your individual circumstances.

Key Variables to Consider

1. How much existing coverage do you already have? If your employer provides comprehensive 24/7 accident coverage, or your union membership includes a solid accident policy, buying an additional standalone policy may be redundant.

2. How risky is your occupation and daily routine? Office workers face lower accident risk than construction workers or delivery cyclists. If you work in a physically demanding job or cycle daily in Copenhagen traffic, accident insurance becomes more relevant.

3. Could you absorb months of lost income if something went wrong? Could you cover months of lost income, rehabilitation costs, or home adaptations if an accident left you permanently disabled? If not, accident insurance provides a real financial safety net.

4. Does your family depend on your income? If your family relies on your income, accident insurance adds a layer of protection in case the worst happens.

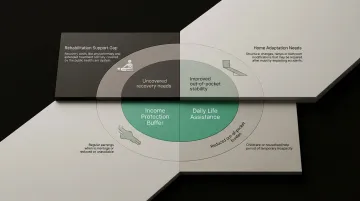

The Case FOR Personal Accident Insurance

Accident insurance provides a financial buffer for costs that fall outside what the Danish public healthcare system or employer schemes cover — such as:

- Rehabilitation and physiotherapy not covered by the public system

- Home adaptations (wheelchair ramps, modified bathrooms)

- Lost income during recovery if no other protection is in place

- Covering childcare or household help during incapacity

According to a 2025 report by Finans.dk, insurance costs in Denmark have risen three times faster than general consumer prices over the last three years, yet the financial consequences of a serious accident can dwarf these premiums.

The Case AGAINST (or for Reviewing Your Coverage)

If you already have:

- Solid employer coverage (24/7, not just during work hours)

- Union accident insurance

- A health insurance policy with rehabilitation benefits

...then adding another personal accident policy may be redundant. The money might be better spent increasing an existing policy limit rather than buying a new one.

Evaluate Your Total Coverage Picture First

The biggest mistake Danes make is buying new policies without first auditing what they already have. That's how people end up paying for overlapping coverage while missing gaps elsewhere.

Inzure's platform shows your complete insurance picture in 60 seconds, identifying gaps and overlaps across all your policies. You upload your documents as PDFs or screenshots, and the AI reads them, including the fine print, to show you what you're actually covered for and what you should be paying. If you're overpaying or under-insured, you'll know right away.

Why Many Danes Are Overpaying for Personal Accident Insurance

The Loyalty Penalty — But Not for Accident Insurance

Danish insurance operates with a systemic problem called the "loyalty penalty" (loyalitetsstraf). A 2025 report by the Danish Competition and Consumer Authority (KFST) found that loyal customers with 10+ years of seniority pay margins 7-8 percentage points higher than new customers for car, house, and contents insurance. Forbrugerrådet Tænk notes this costs the average loyal consumer around DKK 1,200 extra annually.

The same KFST report explicitly found no clear loyalty penalty for personal accident insurance. Margins remain relatively stable over time — unlike car or home insurance, where loyal customers are systematically overcharged.

Silent Premium Increases Still Drive Costs Up

Even without a loyalty penalty, accident insurance premiums still creep upward. All major Danish insurers index-regulate their premiums using the private sector wage index (lønindeks) from Danmarks Statistik — a mechanism called "indeksregulering" (indexation).

Because indexation is written directly into standard policy terms, insurers raise prices every year without sending explicit warning letters. The result: insurance costs in Denmark have risen three times faster than general consumer prices over the last three years, according to Danmarks Statistik data.

Duplicate Coverage You're Already Paying For

Many Danish consumers pay for a personal accident policy that duplicates coverage they already hold through an employer, union, or bundled bank product. Most never realize it. Inzure frequently identifies users with overlapping accident coverage — protection they were entitled to elsewhere but had never been told about.

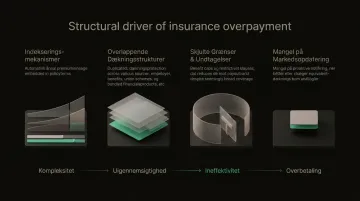

Policy Complexity Works Against You

Insurers use dense policy language that makes it genuinely difficult to compare what you're getting. That information gap benefits the insurer, not the policyholder. The average personal accident policy runs 32 pages — and most people never read them.

This complexity isn't accidental. It creates the conditions for overpayment:

- Indexation clauses buried in standard terms that auto-raise premiums annually

- Overlapping coverage across employer, union, and bank-bundled policies

- Benefit caps and exclusions written in ways that obscure their real impact

- No obligation to notify customers when cheaper equivalent coverage becomes available

How to Save Money on Personal Accident Insurance

Tip 1: Audit Your Existing Coverage Before Buying or Renewing

Before committing to a standalone policy, list all the places where you may already have accident coverage:

- Employer group insurance (check your HR department or employment contract)

- Trade union membership (review your membership benefits package)

- Bank account perks (premium accounts often include insurance)

- Credit card benefits (gold and platinum cards frequently bundle coverage)

Only after completing this audit can you identify whether a gap exists that needs filling.

Tip 2: Compare the Market — On Coverage AND Price

Don't just compare headline premiums. Examine:

- Insured sum (how much the policy pays out for full disability)

- Disability scale (invaliditetsdækning) — how different injuries are assessed

- Exclusions — what activities or circumstances void your coverage

- Claim process — how easy is it to actually get paid?

Use an independent comparison tool. Inzure analyzes policies across Danish insurers and shows the real market price for your specific situation. Upload your current policy as a PDF or screenshot, and the AI reads it (including the fine print) to show you what you're covered for and what you should be paying. If a better deal exists, you'll see it in 60 seconds.

The service is free. If Inzure finds savings and you choose to switch, you pay 20% of what you save. If no better deal exists, the analysis costs nothing. The model is straightforward: Inzure only profits when you do.

Tip 3: Review and Renegotiate at Renewal

Don't let your policy auto-renew without checking whether the premium has increased. If it has:

- Contact your current insurer and reference the KFST findings on silent premium increases

- Request a price match with rates offered to new customers

- If they refuse, gather quotes from competitors

Forbrugerrådet Tænk advises that simply threatening to switch is often enough to secure a better rate, but having real quotes gives you genuine leverage.

Frequently Asked Questions

Is personal accident insurance worth it?

For most people, the answer hinges on three factors: your occupation, existing coverage, and financial buffer if you couldn't work. It's most valuable for those without employer or union accident coverage, people in physical jobs, and families with dependants. Start by mapping what you already have — you may be more covered than you think.

Is personal accident cover on car insurance worth it?

Personal accident cover added to car insurance pays a fixed sum if you're killed or seriously injured in a road accident. It can be worth it if you have no other accident coverage, but may be redundant if you already hold a comprehensive personal accident policy.

What is NOT covered by personal accident insurance?

Key exclusions include illness, disease, self-inflicted injury, injuries linked to alcohol or drug use, and often certain high-risk activities. Always check the specific exclusion list in your policy documents.

How much does personal accident insurance typically cost in Denmark?

Standard adult personal accident policies in Denmark typically range from DKK 800 to DKK 2,500 annually, depending on the insured sum, your age, occupation, and activity level. Prices vary significantly between insurers.

Can I already have accident coverage without knowing it?

Yes — many Danes have partial accident coverage through employer insurance, trade union membership, or credit card and bank account benefits. Cross-check all existing agreements before buying a new policy; duplicate coverage is one of the most common (and costly) mistakes Inzure identifies during policy analysis.