Introduction

Danish consumers waste substantial amounts on travel insurance every year. The culprit is usually coverage they already own. According to the European Insurance and Occupational Pensions Authority (EIOPA), double insurance frequently occurs when consumers purchase policies without realising they already hold travel coverage through credit cards or home insurance, with overlaps typically discovered only at the claim stage.

A single-trip policy for a 10-day European holiday typically costs 200–300 DKK. That's not the problem. The costs stack up through avoidable mistakes:

- Insuring refundable bookings that carry no real financial risk

- Duplicating coverage already embedded in home contents insurance

- Accepting default policy options without comparing alternatives

This guide addresses three dimensions of cost reduction: decisions made before buying, how existing coverage is actively managed, and how trip planning choices affect premiums. Work through each section to pinpoint exactly where you're overpaying.

Key Takeaways

- Most travel insurance overspend comes from three avoidable mistakes: over-insuring, duplicating existing coverage, and accepting the first quote

- Price is driven by trip value, traveller age (premiums jump 22% between age 60 and 80), destination, and add-ons like Cancel For Any Reason

- Insure only actual non-refundable losses — not the full trip value if parts are refundable

- Purchase within 14-21 days of first deposit to unlock pre-existing condition waivers

- Check home contents, credit card, and health policies first; most Danes already carry baggage coverage abroad

How Travel Insurance Costs Build Up — and What Drives Them

Travel insurance costs don't appear as a single obvious expense. They accumulate through coverage decisions you make at purchase, add-ons selected during checkout, and unreviewed renewals. The result: many travellers end up with more coverage than needed, at higher costs than necessary.

Primary cost drivers you control:

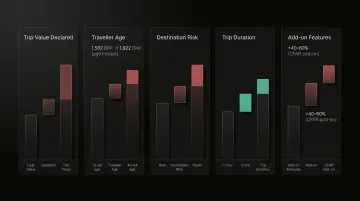

- Trip value declared — premiums scale directly with the total insured amount, so over-declaring refundable bookings inflates costs unnecessarily

- Traveller age — a 60-year-old couple might pay 1,582 DKK, rising to 1,922 DKK at age 80 (a 22% increase)

- Destination healthcare costs — destinations like the USA, Canada, and the Caribbean generate significantly higher premiums than travelling within Europe, due to elevated medical treatment costs

- Trip duration — a two-week policy costs approximately double what a one-week policy costs

- Add-on features — Cancel For Any Reason (CFAR) increases premiums by 40-60% compared to standard comprehensive coverage

Most of these drivers come down to choices made before purchasing — and most can be adjusted.

What makes costs build unnoticed:

Two patterns drive most overspending: locking in coverage without reviewing what you already have elsewhere, and auto-renewing year after year without comparing the market. Structural factors like age and destination matter — but the bigger issue is accepting default coverage without questioning it.

Cost-Reduction Strategies: Smarter Decisions Before You Buy

The most impactful savings in travel insurance come from decisions made before purchase — specifically what is insured, for how much, at what coverage level, and through which channel.

Insure only your actual non-refundable losses

Premiums scale with the declared trip cost. Travelers frequently over-declare by including:

- Refundable hotel bookings

- Airline vouchers or credits

- Costs they can absorb personally

The strategy: Add up only genuinely non-refundable, non-recoverable costs — accommodation deposits, pre-paid tours, non-refundable flights — and insure precisely that amount. If your hotel allows free cancellation up to 48 hours before arrival, exclude it from your insured trip value.

Compare policies across multiple providers before buying

The default option offered at booking — by airlines, tour operators, or travel agents — is rarely the most cost-effective choice. Independent comparison tools expose the same or better coverage at lower prices.

How to compare effectively: Use online comparison platforms to view multiple quotes side-by-side. Sort results from lowest to highest price while verifying coverage quality. Check that medical evacuation limits, cancellation terms, and baggage coverage align with your needs before prioritising price alone.

Be cautious with high-cost optional add-ons

Cancel For Any Reason (CFAR) is the most expensive add-on in travel insurance. Adding CFAR increases the base premium by 40-60%, and it reimburses only 50-75% of non-refundable trip costs.

Standard trip cancellation already covers the most common scenarios:

- Illness or injury preventing travel

- Death of a close family member

- Severe weather disrupting flights

CFAR is worth the cost premium only if you have a specific, non-standard reason to cancel that wouldn't otherwise be covered.

Purchase early to unlock time-sensitive benefits

Most providers require purchase within 14-21 days of your first trip deposit to access two benefits that aren't available later:

- Pre-existing condition waivers (your condition must be stable for at least 60 days prior to booking)

- CFAR eligibility, which is unavailable after the early purchase window closes

Early purchase won't always lower the base premium, but it locks in coverage for pre-existing conditions and keeps CFAR as an option — both of which disappear once the window passes.

Look for group, family, or membership discounts

A few channels consistently offer lower premiums than the default booking-page option:

- Some providers include children at no extra cost under a parent's policy

- Existing policyholders may qualify for multi-policy discounts when adding travel coverage

- Buying directly online typically costs less than purchasing through a travel agent who earns commission on the sale

Cost-Reduction Strategies: Managing What You're Actually Covered For

Significant savings come from actively reviewing coverage against what is already in place — rather than accepting a standard policy at face value and paying for protection that already exists elsewhere.

Check what your credit card already covers before adding standalone coverage

Many premium credit cards in Denmark include travel insurance benefits when the trip is paid with that card:

- Trip cancellation

- Travel delay

- Lost baggage

- Emergency medical evacuation (sometimes)

Travellers who purchase separate standalone coverage without checking this are paying twice. Double insurance is most common with travel insurance, particularly when consumers hold coverage through credit cards without realising it.

What to verify: Read the exact terms of your card's travel insurance policy. Pay attention to:

- Coverage limits (e.g., maximum medical expenses covered)

- Whether medical evacuation is included

- Geographic restrictions (some cards cover only Europe)

For lower-risk domestic or short-haul trips, credit card coverage may be sufficient.

Review whether your home contents insurance covers travel

Danish home contents insurance (indboforsikring) typically extends coverage to personal belongings (rejsegods) taken abroad. According to the Danish Insurance & Pension Federation, private luggage is usually insured during travels and temporary stays abroad for up to three months, offering the same coverage as at home.

Carrier-specific coverage:

| Insurance Carrier | Coverage Extension Abroad | Limits |

|------------------|---------------------------|---------|

| Topdanmark | Covers belongings taken on the trip, sent ahead as luggage, or purchased during the trip | Maximum 130,990 DKK for baggage |

| Alka | Covers belongings during travel to, from, and in foreign countries | Valid for up to 3 months from departure |

| Tryg | Requires active "Bagage" add-on selection on home insurance | Coverage only applies if add-on is selected |

Critical limitation: Home contents insurance covers only physical belongings. It does not cover medical evacuation, emergency healthcare, or trip cancellation.

What to do: Verify your home contents insurance limits before purchasing baggage coverage through a standalone travel policy. If your indboforsikring already covers 130,000 DKK of belongings abroad, adding separate baggage cover is redundant.

Calibrate medical coverage limits to actual risk, not the maximum available

Emergency evacuation coverage ranges widely in cost depending on the limit selected. The right amount depends on:

- Destination

- Planned activities

- Age

- Existing health coverage

Example: A 35-year-old travelling to Spain for a week-long beach holiday doesn't need the same evacuation limit as a 65-year-old trekking in Nepal. Adjust coverage to match genuine risk exposure.

Consider annual (multi-trip) policies if you travel frequently

For travellers taking three or more trips per year, an annual policy is significantly more cost-effective than purchasing separate single-trip policies each time.

Cost comparison: A 10-day single-trip policy to Europe typically costs 200-300 DKK. An annual policy covering the same region costs 500-700 DKK. The annual policy breaks even after just two short trips per year.

Trade-offs: Annual policies typically cover evacuation and baggage protection across all trips, but may not include deep customisations like CFAR or adventure sports add-ons.

Use an independent analysis tool to identify duplicate coverage and hidden overlap

Paying for the same coverage through multiple policies simultaneously is one of the most common and costly mistakes Danish travellers make.

Platforms like Inzure analyse existing insurance policies in 60 seconds, identifying:

- Where travel-related coverage already exists (home insurance, credit card policies)

- Duplicate costs across policies

- The real market price for what you actually need

The platform accepts policy documents as PDFs or screenshots, reads the fine print, and flags overlaps that most travellers overlook.

Cost-Reduction Strategies: Using Trip Structure and External Factors to Lower Premiums

Not all premium drivers come from the coverage you choose. Destination, duration, and trip type each affect what you pay — and adjusting them can cut costs just as effectively as trimming your policy.

Choose destinations strategically when comparing costs

Medical treatment costs vary significantly by country, and travel insurance premiums reflect this directly.

High-cost destinations:

- United States

- Canada

- Parts of the Caribbean

These generate substantially higher premiums than comparable destinations with lower medical cost environments.

If you have flexibility on destination, check insurance quotes before finalising the booking. A comparable holiday in Portugal may cost half as much to insure as a trip to the USA.

Limit trip duration to what is genuinely needed

Travel insurance premiums scale with duration. A two-week policy typically costs about double a one-week equivalent.

Avoid including buffer days or extra nights that aren't strictly necessary — these extend the insured period without adding real coverage value.

Match the policy type to the trip type

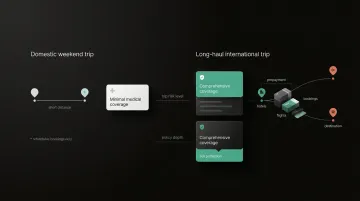

Different trip profiles require different policy types:

- Domestic weekend trip with refundable bookings — minimal medical cover only

- Long-haul international trip with significant non-refundable prepayments — comprehensive coverage

Over-insuring a low-risk, low-cost trip is one of the most avoidable ways premiums become disproportionate to actual exposure.

A two-night Copenhagen city break with a refundable hotel and a low-cost flight doesn't warrant the same coverage level as a three-week safari in Tanzania with non-refundable lodge bookings.

Conclusion

Saving money on travel insurance comes down to one thing: knowing what you actually need and what you are already paying for. Most overspending happens not from buying too much, but from buying blindly — duplicating coverage, missing gaps, or staying with a policy long after better options emerged.

Insurance costs are not static. Markets shift, travel habits change, and a policy that made sense two years ago may now overlap with your home or credit card coverage. Inzure's AI analysis reads your existing policies, compares them against current Danish market rates, and flags exactly where you are overpaying or underinsured — so you stop relying on what your insurer claims is fair and start seeing what coverage actually costs.

Frequently Asked Questions

How can I reduce the cost of travel insurance?

Insure only non-refundable costs, compare policies across providers rather than accepting the default option, and check for existing coverage through credit cards or home insurance. Many Danes already have baggage coverage abroad through their home contents insurance, making some standalone coverage redundant.

Can I get travel insurance if I have a pre-existing medical condition?

Yes, coverage is available for travellers with pre-existing conditions, but premiums will be higher to reflect increased medical risk. Declaring conditions accurately is essential — failure to do so can invalidate a claim. Some providers offer pre-existing condition waivers if you buy within 14-21 days of your first trip deposit.

Is norovirus covered by travel insurance?

Norovirus is typically covered under the medical expenses section if you require medical treatment abroad. It is generally not covered as a trip cancellation reason unless the illness is severe enough to prevent travel. Check policy wording carefully for the specific threshold required.

Does my credit card travel insurance give me enough coverage?

Credit card travel insurance varies significantly by card and provider. Some offer robust coverage for cancellations, delays, and baggage, while others provide only minimal protection. Check your card's exact terms — particularly coverage limits and whether medical evacuation is included — before deciding if additional coverage is needed.

Is it cheaper to buy annual travel insurance or single-trip policies?

Annual policies are generally more cost-effective for travellers taking three or more trips per year, as the combined cost of multiple single-trip policies typically exceeds the annual premium. However, annual policies offer less flexibility for customisation, so the right choice depends on travel frequency and trip type.

What coverage should I never cut to save money on travel insurance?

Emergency medical coverage and medical evacuation should never be cut, particularly for international travel where domestic health insurance does not apply. A single medical emergency or evacuation abroad can cost more than most travellers can pay out of pocket.