Introduction

Most people buy insurance and forget about it — and that's exactly what insurance companies count on. Keeping policies complicated makes it harder for customers to compare options or notice when they're overpaying.

The result is predictable: you pay more for less coverage as time goes on.

The timing of an insurance review directly determines whether you're financially protected or left with gaps you won't discover until you file a claim. This article explains when to review, what warning signs to look for, and what it typically costs Danish households to ignore the problem.

Key Takeaways

- Review your insurance annually or after major life changes to avoid overpaying or being underinsured

- Life events like marriage, moving, or having a child immediately trigger coverage changes

- Inflation shrinks your coverage value each year, even when your life stays the same

- Skipping reviews leads to coverage gaps, duplicate policies, and loyalty penalties costing thousands of kroner

- AI tools like Inzure can now analyse all your policies in 60 seconds instead of 10 hours

What Is an Insurance Policy Review (and Why Most People Skip It)

An insurance policy review is a systematic check of all your active policies — home, travel, accident, liability — to verify that your coverage still matches your life, assets, and risk exposure today — not the life you had when you first signed up years ago.

Why people avoid it:

Insurance documents are deliberately complex. According to Denmark's Competition and Consumer Authority (KFST), the majority of Danish consumers have not obtained new insurance quotes or considered switching providers within the last two years. One documented case showed a 32-page policy document that had never been opened since purchase.

Insurers don't proactively flag when your coverage has become outdated or overpriced — because keeping you unaware is profitable.

The core risks of never reviewing:

- Being underinsured when you file a claim — In a 2023 case before the Danish Insurance Complaints Board, a consumer claimed 1.1 million DKK after a total fire loss. The insurer reduced the payout to 423,534 DKK due to depreciation and missing receipts.

- Duplicate coverage goes unnoticed — travel insurance is a common example, where consumers pay for a separate policy while already covered through their credit card or bundled home insurance.

- House insurance prices increased by an average of 26% since October 2022, with some insurers raising prices by up to 75% — yet most customers never notice.

The loyalty penalty:

KFST research shows that loyal customers with 10+ years of tenure pay an average of 7-8 percentage points more than new customers for identical coverage. Some companies charge loyal customers up to 30-35 percentage points more. The average annual overpayment is 240 DKK for contents insurance and 443 DKK for house insurance — and that gap grows every year you stay without reviewing.

That's why a review doesn't automatically mean switching. Sometimes it confirms you're well-covered. Other times, it gives you the market data you need to negotiate better terms with your existing insurer — without going anywhere.

The Best Time to Review Your Insurance Policy

While an annual review is always recommended, certain moments make a review especially urgent and valuable.

After a Major Life Event

These life changes immediately trigger coverage adjustments:

- Marriage or cohabitation — When moving in together, you only need one shared contents insurance and one travel insurance, making this a good moment to consolidate and cut duplicate policies.

- Having or adopting a child — Family coverage needs shift immediately. One Inzure customer found they were incorrectly paying for a newborn who should have been covered free until age 2 — a common billing error worth checking.

- Buying or selling a home — Moving from an apartment to a house requires purchasing a new standalone house insurance, and contents insurance prices fluctuate based on the new address and square footage.

- Starting a business or changing jobs — Employment changes may affect income replacement needs and available group coverage.

- Retirement — If a partner moves to a nursing home, standard Danish contents insurance covers belongings at both locations, but other coverage types may no longer be necessary.

- Divorce or separation — Joint policies must be split. Both parties require individual contents and travel insurance to ensure proper liability and claims payouts.

Each of these events changes what you own, who depends on you, and what you're legally liable for — all of which affect what your policy should actually cover.

At Your Annual Renewal

The annual renewal notice is the most natural — and most ignored — opportunity for a review. Instead of auto-renewing, use this moment to:

- Compare your current coverage against market rates

- Check for new discounts you may now qualify for

- Assess whether coverage limits still reflect current replacement costs

Make it a habit: Tie your review to a fixed date like your birthday, anniversary, or the renewal date itself. Even 20 minutes spent comparing rates at renewal can reveal whether you're paying above market — something Inzure's analysis surfaces in about 60 seconds.

Personal timing matters, but your coverage can also erode without any change in your circumstances.

When External Market Conditions Change

Your coverage can become inadequate even when nothing in your personal life changes:

- Inflation and construction costs — Construction costs for residential buildings in Denmark rose 0.2% in Q4 2025, and renovation costs surged 4.3% in 2025.

- Rising property values — The policy you took out three years ago may now leave you significantly underinsured because insurers do not automatically adjust coverage limits to reflect market changes.

- Material shortages — Insurers like If warn that rising raw material prices increase the risk of underinsurance, meaning the cost to rebuild after fire or major damage exceeds your existing policy limits.

Clear Signs Your Insurance Coverage Needs a Review Right Now

Even without a life event or renewal notice, certain signals indicate your coverage is likely misaligned.

Your premium increased without explanation

If your premium has risen at renewal without any corresponding change in your behavior, risk profile, or claims history, you're likely experiencing a loyalty penalty. This is an immediate signal to compare market rates.

You've made significant purchases or renovations

New kitchen, home office, solar panels, or valuable electronics? If these aren't reflected in your policy, you're automatically underinsured. Your contents insurance won't cover what it doesn't know about.

You're holding multiple policies across different providers

Duplicate travel insurance is common — one through your employer, one purchased separately, and one bundled with your credit card. You're paying three times for the same protection.

It has been more than two years since your last review

According to Forbrugerrådet Tænk, the average Danish household pays over 5,000 DKK more annually for non-life insurance than they would if prices had tracked general inflation. Two years of inaction is all it takes to fall significantly behind the market.

If any of these signs look familiar, your policy is overdue for a closer look. Inzure monitors your policies continuously and flags these issues automatically — no manual tracking required.

What Happens When You Never Review Your Insurance

The financial result is counterintuitive: customers who never review their policies consistently end up both overinsured (paying for coverage they don't need) and underinsured (lacking coverage where they actually need it) at the same time.

The worst-case scenario:

You discover at claim time that your policy limits haven't kept up with replacement costs. You receive a payout that covers only a fraction of your actual loss. This is the moment the omission becomes visible and most costly. In the Danish Insurance Complaints Board case mentioned earlier, the customer expected full replacement of their home contents but received less than 40% due to depreciation and insufficient documentation.

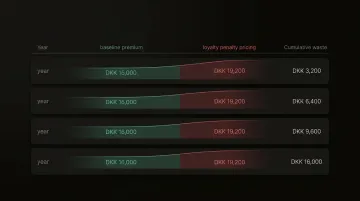

The compounding cost of inaction:

A premium that's even 15-20% above market rate, unchecked for several years, amounts to thousands of kroner in unnecessary spending. Loyalty penalties accumulate quickly:

| Year | Baseline Premium | Cost at +20% Penalty | Cumulative Waste |

|---|---|---|---|

| 1 | 16,000 DKK | 19,200 DKK | 3,200 DKK |

| 2 | 16,000 DKK | 19,200 DKK | 6,400 DKK |

| 3 | 16,000 DKK | 19,200 DKK | 9,600 DKK |

| 5 | 16,000 DKK | 19,200 DKK | 16,000 DKK |

Based on the average Danish household spending approximately 16,000 DKK annually on non-life insurance.

The numbers behind the table become concrete when you look at actual cases. One Inzure user had been without home insurance for at least 10 years without realizing it. Another paid for a spouse missing from three separate policies. These aren't edge cases — they're predictable outcomes of a system designed to discourage active review.

How to Review Your Insurance Policy the Right Way

Step-by-step self-directed review:

- **Gather all active policy documents** — Declaration pages, terms and conditions, and endorsements

- Note your coverage limits and exclusions — What's covered, what's not, and up to what amount

- Compare against your current asset values — Is your home insured for its current rebuild cost? Do your contents limits reflect recent purchases?

- Check the current market rate — What would equivalent coverage cost from other providers today?

Independent tool or direct agent?

Once you have your documents in hand, the next question is who should help you interpret them. Agents working for a specific insurer have an incentive to keep you with that insurer. Independent platforms analyse your actual policies across all providers without that bias.

Inzure works this way: upload your policy PDFs or screenshots, and the platform runs an AI analysis in 60 seconds — comparing your current coverage against live Danish market rates, flagging gaps and duplicate coverage, and showing where you're overpaying. No insurer affiliation, no obligation to switch.

Build a simple review routine

That analysis is most useful when it's part of a regular habit, not a one-off scramble at renewal time.

- Set a calendar reminder at renewal time

- Keep a running record of new purchases or renovations

- Note any life changes as they happen so your next review has a clear starting point

Frequently Asked Questions

What is an insurance policy review?

It's a structured check of all your active policies to verify that coverage still matches your current life, assets, and financial situation. A proper review reveals gaps, duplicates, and overpriced premiums that accumulate silently over time.

How often should I review my insurance coverage?

Review at least once a year, typically at renewal. You should also review immediately after any major life event — marriage, a new home, a new child, or a significant income change.

When should I review my home insurance?

Review after buying or renovating your home, when property values or construction costs in your area have risen significantly, and at each annual renewal. Given that construction costs rose 4.3% in 2025, your rebuild coverage may already be outdated.

How does the insured sum work on Danish home insurance?

Danish home insurance uses an indexed "Nyværdisum" — a replacement-cost sum that adjusts annually to track construction price changes. Most major Danish insurers waive underinsurance clauses on these policy types, but it's still worth confirming your sum keeps pace with rising rebuild costs.

What are the policy documents I need for a review?

You need the declaration page (summarizing coverage limits, deductibles, and premium), the full policy terms and conditions, and any endorsements or riders attached to the base policy. Under EU regulations, you should also have received an IPID (Insurance Product Information Document) at purchase.

What happens if I never review my insurance policy?

Without regular reviews, coverage limits fall behind real-world costs and you continue paying loyalty premiums well above market rates. Gaps tend to surface only when you file a claim — by then, it's too late to fix them.