Introduction

Most Danes never compare their insurance prices — not because they don't want to save money, but because the industry makes it deliberately difficult to compare like-for-like. This complexity isn't a design flaw; it's a feature that benefits insurers.

Loyal customers pay for that trust. Staying with the same insurer without comparing can cost you DKK 2,400 more per year than the actual market price — and after a decade, that gap often comes with coverage holes you never knew existed.

This guide covers:

- What drives insurance prices in Denmark

- A step-by-step process for comparing policies accurately

- Common mistakes that cost consumers money

- How to stop overpaying for good

Key Takeaways

- Identical coverage can cost thousands of kroner more at one insurer than another — comparing quotes is the fastest way to cut premiums

- Your price is shaped by coverage level, personal profile, asset type, and how long you've stayed with the same insurer

- Comparing correctly means using identical coverage parameters across all quotes, not just finding the lowest headline number

- Loyal customers routinely pay thousands of kroner more per year than new customers for the exact same policy

- Tools like Inzure compare your current premiums against the Danish market in 60 seconds — for free

Why Most People Pay Too Much for Insurance

The insurance industry's complexity is partly structural and partly strategic. Policies are written in dense legal language, coverage terms differ by insurer, and comparing apples to apples requires significant time investment that most consumers simply can't make.

The loyalty penalty — a phenomenon where long-term customers receive automatic annual price increases that have nothing to do with their risk profile. According to Denmark's Competition and Consumer Authority (DCCA), a customer with 10 years of tenure pays on average 7-8 percentage points more than a new customer for identical car insurance, house insurance, or contents insurance. This analysis covered 7.4 million private insurance policies linked to individual-level data from Statistics Denmark.

The DCCA found that insurers earn higher margins from customers aged 65 and older, those with lower educational backgrounds, and those with limited financial literacy — the groups least likely to compare prices or switch providers.

Two other problems quietly add to the financial damage:

- Duplicate coverage — travel insurance bundled with a credit card stacked on top of a standalone policy, paying twice for the same protection

- Coverage gaps — missing protection that only surfaces when someone actively audits their policies, often after a claim is denied

What Factors Determine Insurance Prices

Insurers use a range of personal and asset-related data points to calculate premiums. Understanding these factors helps you know which variables you can control, which you can't, and where price differences between providers are likely to be largest.

Coverage Type and Level

The type of coverage (liability-only vs. comprehensive) and the specific limits and deductibles you choose have the largest direct impact on premium cost. Higher deductibles generally lower premiums, but increase your out-of-pocket risk when a claim occurs.

The math is straightforward:

- Choose a DKK 5,000 deductible instead of DKK 2,000, and your annual premium might drop 15–20%

- File a claim, and you'll pay DKK 3,000 more before insurance covers anything

- The savings only make sense if you can afford the higher deductible and rarely need to use it

Comparing insurance prices only makes sense when coverage parameters are held constant: same type, same limits, same deductible. Mismatched coverage levels are the most common cause of misleading price comparisons.

Personal Profile and Risk History

Personal factors — age, claims history, location of residence, and in some insurance types, credit history — are used by insurers to model future risk. Risk-based pricing means two people with identical coverage at the same address can receive very different quotes.

How your history affects pricing:

- A clean claims record typically results in lower premiums

- Recent claims, even minor ones, can trigger rate increases across most insurers

- Danish insurers layer demographic factors on top of expected claims costs, which widens quote variation between providers

Asset Characteristics

The insured asset itself is a major pricing variable. For home insurance, property age, construction type, and flood or fire risk in your area all drive pricing directly. Older properties or those in high-risk areas face higher premiums — this is worth researching before purchase, not after.

Some assets are notably cheaper to insure than others. A newer property in a low-risk area will almost always carry a lower premium than an older home in a flood-prone postcode — even with identical coverage terms.

Duration with the Same Insurer (The Loyalty Penalty)

One of the least-discussed pricing factors is tenure with an existing insurer. Many insurers apply incremental price increases at renewal that aren't tied to risk : the loyalty penalty.

Consider a Danish household paying DKK 3,200/year for contents insurance as a new customer. After five years of auto-renewal — no claims, no coverage changes — their premium rises to DKK 3,850/year, a 20% increase. A new customer buying identical coverage today still pays DKK 3,200. That DKK 650 gap is pure loyalty penalty.

The DCCA's analysis confirms that Danish insurers contractually index premiums to private-sector wage growth (approximately 3.5% for 2025). Insurers are not required to notify customers of annual price increases that stay within the indexation benchmark — only increases exceeding it trigger a notification obligation.

This means most loyal customers never realize they're drifting above market price.

Switching insurers, or even signaling that you're about to, can sometimes produce immediate price corrections. That's why regular comparison matters at every renewal, not just when you first buy a policy.

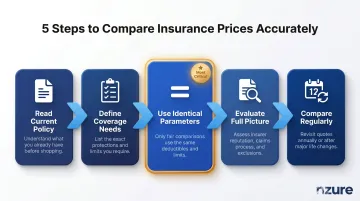

How to Compare Insurance Prices: Step-by-Step

Step 1: Gather and Read Your Current Policy Documents

Reading your existing policy is the essential starting point. Most people don't know what they're currently covered for, what their deductible is, or what exclusions apply. You can't compare effectively without knowing your baseline.

This is where many people discover they are either:

- Underinsured: Missing coverage they assumed they had (e.g., bicycle theft not included in contents insurance)

- Overinsured: Paying for overlapping coverage from multiple sources (e.g., travel insurance in both credit card benefits and standalone policy)

Step 2: Define the Coverage You Actually Need

Before requesting any quotes, decide on the coverage level that reflects your actual risk exposure — not just the minimum required or the maximum available.

How to assess this:

- Value of the asset you're insuring

- Financial ability to absorb a loss (can you afford a DKK 10,000 unexpected expense?)

- Legal minimums (mandatory for car insurance and dog ownership in Denmark)

- Specific risks relevant to your situation (e.g., high-value e-bike requires explicit theft coverage)

Defining coverage needs upfront prevents the common mistake of unconsciously downgrading coverage to get a lower price when comparing.

Step 3: Use Identical Coverage Parameters Across All Quotes

Valid price comparison requires comparing the same coverage type, the same limits, and the same deductible from every provider. A lower quote that comes with reduced coverage or a higher deductible is a trade-off, not a saving — and it's easy to miss if you're only scanning the premium figure.

What information you'll typically need to provide:

- Asset details (property age, car model, etc.)

- Claims history (past 5 years)

- Personal information (age, occupation, postcode)

- Current policy details (coverage limits, deductible)

Step 4: Look Beyond the Premium — Evaluate the Full Picture

The cheapest premium is not always the best value. Four factors matter beyond the price:

- Claims handling reputation: The Danish Insurance Complaints Board (Ankenaevnet for Forsikring) processed 2,074 complaints in 2025, up 58% since 2021. Consumer win rates range from 4.3% (Alka) to 28.6% (Codan) — a difference worth knowing before you sign.

- Financial stability: Verify the insurer has sufficient reserves to pay claims during major events. Nordic insurers generally carry strong balance sheets, but individual company health varies.

- Policy exclusions: A policy that routinely disputes or delays claims delivers less value than a slightly pricier one with a strong track record.

- Transparency: How clearly written is the policy document? How quickly does the insurer respond to inquiries before you're a customer?

Step 5: Compare Regularly — Not Just at Renewal

Insurance markets change constantly. The price you were quoted 12 months ago may no longer reflect the market. Loyal customers are especially exposed: annual indexation increases and renewal creep push premiums above market rate without any change to your coverage.

When to check prices:

- At least annually, even if you're satisfied with current coverage

- After major life changes (new address, new vehicle, marriage, newborn)

- When you receive a renewal notice with a price increase

Automated monitoring removes the manual effort entirely. Instead of remembering to check once a year, continuous comparison keeps you informed whenever your premium drifts above what the market actually offers.

Common Mistakes to Avoid When Comparing Insurance

Comparing Apples to Oranges

Many consumers get excited about a lower quote without checking whether the coverage is actually the same.

Example: You receive a quote for contents insurance at DKK 2,400/year compared to your current DKK 2,900/year. Looks like a DKK 500 saving. But closer inspection reveals:

- Current policy: DKK 2,000 deductible, DKK 1 million liability coverage, bicycle theft included

- New quote: DKK 5,000 deductible, DKK 500,000 liability coverage, bicycle theft excluded

A higher deductible alone can cost you DKK 3,000 more out of pocket on a single claim — wiping out years of "savings" at once.

Comparing Only at Renewal

Most people only compare at renewal, which means they've been paying above-market prices for months or years before acting. By the time the renewal notice arrives, the loyalty penalty has compounded for years.

The data backs this up: EIOPA's 2024 research found only 8% of EU insurance purchases happen through comparison platforms. Nordic insurers hold retention rates of 85–90%, with average customer relationships lasting 8–10 years. Most consumers never compare at all — and insurers count on it.

The "Too Much Information" Trap

Many comparison platforms require a phone number or personal details before showing any prices — which leads to sales calls, not quotes. Watch for these red flags before entering your information:

- Requires phone number before displaying any price

- Shows only a "request a callback" option instead of live quotes

- Asks for contact details before letting you see coverage comparisons

Choose a platform that shows market prices first. Tools like Inzure analyze your existing policy and surface comparisons before asking for any personal commitment.

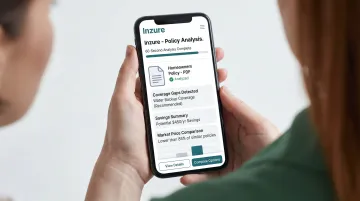

How Inzure Can Help

Inzure is Denmark's first AI-driven, independent insurance platform built to give consumers the pricing clarity the insurance industry rarely volunteers. It works for the consumer, not the insurer — with no affiliation to any insurance company.

Upload a policy document — PDF or screenshot — and the platform returns a full analysis in 60 seconds: actual market price for your current coverage, missing protections, duplicate policies, and unjustified price increases. It works across all major Danish insurers, including Tryg, Topdanmark, Alka, Codan, GF, Alm. Brand, If, and Lærerstandens Brandforsikring.

Key features:

- Analyzes any Danish policy document in 60 seconds — PDFs and screenshots accepted

- Independent and unaffiliated — no referral fees from insurers, no conflicts of interest

- Detects coverage gaps, duplicate policies, and loyalty-penalty price increases automatically (for example, missing bicycle theft coverage or redundant travel insurance)

- GDPR-compliant EU data storage — your information is never sold

- Free to use — Inzure earns 20% of first-year savings only if a better deal is found; switching for better coverage at the same price is free

- Ongoing market monitoring sends automatic alerts when a better deal appears, so you never drift above market price again

Real verified savings from early users range from DKK 2,800/year to DKK 48,000/year, with one customer achieving a 46% premium reduction while improving coverage.

Conclusion

The people who consistently save on insurance aren't necessarily the most financially savvy — they're the ones who compare regularly and systematically. The process itself isn't complicated. The industry just benefits when it feels that way.

The real goal is making sure what you pay accurately reflects the market price for the coverage you actually need. Danish households spend an average of nearly 16,000 DKK per year on non-life insurance — 4.4% of total consumption. Even a 10% improvement on that figure is 1,600 DKK back in your pocket annually.

To put that into practice, the core habits are simple:

- Compare at renewal, not just when something goes wrong

- Check coverage gaps and duplicates, not just price

- Treat your insurance portfolio as a whole, not individual policies in isolation

Frequently Asked Questions

How can I compare insurance policies?

Effective comparison requires using the same coverage type, limits, and deductible across multiple providers, and reading each policy's terms rather than just the headline premium. Hold all variables constant except the insurer and price.

What is the best website to compare insurance quotes?

Look for platforms that are independent from insurers, require no obligation to purchase, and analyze your existing policy rather than just generating new quotes. Avoid platforms that require phone numbers before showing prices.

What are the 4 types of insurance coverage?

The four main coverage types are liability (ansvarsforsikring), home/contents (indboforsikring), accident (ulykkesforsikring), and travel (rejseforsikring). The specific types you need depend on your life situation and existing policies.

Can I get a car insurance quote without giving my phone number?

Many platforms allow price estimates without personal contact details. Prioritize platforms that show price ranges or perform analysis without requiring upfront contact information to avoid unwanted sales calls.

What is a quick quote in insurance?

A quick quote is a preliminary price estimate based on minimal information — useful for initial comparisons but less accurate than a full quote, which requires detailed personal and asset information for a binding offer.

What should you not tell your insurance company?

Always be truthful on insurance applications (misrepresentation can void your policy under Forsikringsaftaleloven § 4). Be cautious about volunteering information beyond what is directly asked, particularly during a claim, before consulting your policy terms.