Introduction

Most people choose insurance based on price alone—yet two policies at the same premium can offer drastically different protection. A €500/year home insurance policy from one carrier might cover burst pipe damage, while an identical-priced competitor excludes it entirely. Pick the wrong one, and a single claim could leave you with a €15,000 out-of-pocket expense.

Insurance companies have historically made policies complicated to compare, and that complexity is deliberate. Dense 32-page documents, opaque coverage limit notations, and buried exclusions all serve the same purpose: ensuring consumers cannot easily see what they're actually buying.

This guide shows you how to work through that complexity. You'll learn how to read coverage limit numbers, what elements to compare side by side, and how to avoid the most costly comparison mistakes. The goal: decisions that actually protect your assets.

Key Takeaways

- Coverage limits cap what an insurer pays per claim — set them too low and you're exposed; set them too high and you overpay for coverage you don't need

- Compare limits, exclusions, sublimits, deductibles, and check for duplicate coverage across policies

- Sublimits within a policy (such as a 10,000 kr cap on valuables inside a home contents policy) often matter more than the headline coverage amount

- Good limits match your assets and risks, not just legal minimums

- Inzure analyzes your existing policies in 60 seconds, spotting coverage gaps, duplicate cover, and whether you're paying above market rate

What Are Insurance Coverage Limits?

Coverage limits define the maximum payout an insurer will make for a covered claim. Every policy contains two fundamental limit types that govern how much protection you actually have:

Per-occurrence limits cap the maximum payout for a single claim event. If your home insurance has a 200.000 kr per-occurrence limit and a fire causes 250.000 kr in damage, you cover the 50.000 kr shortfall out of pocket.

Aggregate limits cap the total payout across all claims during the entire policy period (typically one year). Once you exhaust this total, you bear all remaining costs out of pocket until the policy renews.

Coverage Categories Carry Separate Limits

Most policies divide protection into distinct categories, each with its own independent limit:

- Bodily injury liability - Medical costs and legal damages when you injure someone

- Property damage liability - Repair costs when you damage someone else's property

- Personal property - Your belongings (furniture, electronics, clothing)

- Legal liability (ansvarsforsikring) - Protection against claims where you are held responsible for damages to others

You must evaluate each category independently when comparing policies. A policy might offer strong property damage protection but inadequate bodily injury coverage—and you won't know unless you check each limit separately.

Split Limits vs. Combined Single Limits

Split limits assign separate maximums to each category. A home insurance policy might provide 500.000 kr for property damage, 1.000.000 kr for personal liability per incident, and 50.000 kr for personal belongings—each capped independently.

Combined single limits (CSL) pool all coverage into one flexible total amount—for example, 500.000 kr that can be allocated however needed across different damage types. CSL policies typically carry higher premiums due to this flexibility, but they eliminate the risk of exhausting one category while others remain unused.

Key Elements to Compare Across Insurance Policies

When two policies appear similar in name and price, the real differences live in four core areas that most consumers never read.

Coverage Inclusions vs. Exclusions

What a policy does NOT cover is just as important as what it does. Two home insurance policies (indboforsikring) may both cover fire damage, but only one might cover water damage from burst pipes. A travel policy might cover trip cancellation for illness but exclude cancellations due to work obligations — a common gap that catches people off guard.

Identify your most likely risk scenarios first, then confirm those are actually included — not just implied by the policy name. A "comprehensive" policy sounds complete, but the term has no legal definition. Read the exclusions section to verify your specific risks are covered.

Coverage Limits and Sublimits

Top-level limits tell only part of the story. Sublimits impose smaller caps within broader coverage categories — and they're the most overlooked element in policy comparison.

A home policy might advertise 50.000 kr jewelry coverage, but a sublimit caps individual items at 5.000 kr. If you own a 15.000 kr engagement ring, you'll only recover 5.000 kr after a theft unless you purchase additional scheduled coverage.

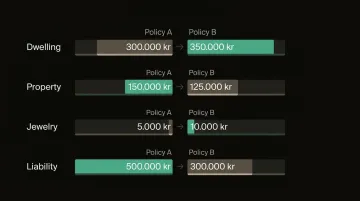

Compare per-occurrence and aggregate limits (per-claim cap and total annual cap) across equivalent policy categories side by side — not just the total premium. A simple table makes the gaps visible immediately:

| Coverage Type | Policy A Limit | Policy B Limit |

|---|---|---|

| Dwelling | 300.000 kr | 350.000 kr |

| Personal Property | 150.000 kr | 125.000 kr |

| Jewelry (sublimit) | 5.000 kr | 10.000 kr |

| Liability | 500.000 kr | 300.000 kr |

Deductibles and Their Relationship to Limits

A higher deductible lowers your premium but increases your out-of-pocket cost before insurance activates. The combination of deductible plus limit tells the true story of protection value.

For frequent small claims — water damage, bicycle theft, minor travel disruptions — the deductible gap compounds fast. Consider two policies with identical 100.000 kr limits:

| Policy A | Policy B | |

|---|---|---|

| Deductible | 500 kr | 2.500 kr |

| Effective coverage | 99.500 kr | 97.500 kr |

| Out-of-pocket on a 3.000 kr claim | 500 kr | Full cost (below deductible) |

The lower-deductible policy pays out on claims the higher-deductible policy simply absorbs.

Duplicate and Overlapping Coverage

Many consumers hold multiple policies with overlapping coverage — and pay twice for the same protection. Travel insurance (rejseforsikring) and credit card travel benefits, for example, often duplicate trip cancellation and lost luggage coverage.

To identify overlap:

- List every active policy you hold

- Document what events each policy covers

- Cross-reference to find duplicate protection

- Eliminate or reduce redundant coverage

Similarly, accident insurance (ulykkesforsikring) and liability coverage (ansvarsforsikring) can overlap on certain injury scenarios. Spotting these duplicates is one of the fastest ways to reduce your total insurance spend without losing any real protection.

How to Read and Decode Coverage Limit Numbers

Coverage limits appear as number series like 100/300/100 or 25/50/25. Reading them correctly is essential for accurate comparison—the three-number format in liability insurance is the most common example, used primarily in auto liability contexts abroad, but the underlying logic applies to liability coverage more broadly.

Split Limits Decoded

In the three-part format:

- First number = Maximum payout per injured person

- Second number = Total bodily injury maximum per accident

- Third number = Maximum for property damage

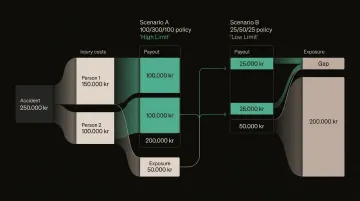

Example: 100/300/100 policy (illustrative)

If a crash injures two people with total medical costs of kr. 250,000:

- Person 1 injuries: kr. 150,000 (policy pays kr. 100,000 maximum)

- Person 2 injuries: kr. 100,000 (policy pays kr. 100,000)

- Total policy payout: kr. 200,000

- You pay out of pocket: kr. 50,000

Now compare that to a 25/50/25 policy covering the same accident:

- Person 1 injuries: kr. 150,000 (policy pays kr. 25,000 maximum)

- Person 2 injuries: kr. 100,000 (policy pays kr. 25,000 maximum)

- Total policy payout: kr. 50,000 (capped by the per-accident limit)

- You pay out of pocket: kr. 200,000

That kr. 150,000 gap in out-of-pocket exposure comes from a single limit choice — which is why reading these numbers carefully before signing matters.

Proportional Underinsurance in the Danish System

Denmark uses strict proportional underinsurance (underforsikring) — and unlike the U.S. system, there is no safe-harbor threshold. According to Forsikring & Pension, if your sum insured falls below the actual replacement value, every claim is reduced proportionally:

Compensation = Loss × (Sum Insured ÷ Total Value)

Danish Example:

- Contents actual value: kr. 200,000

- Sum insured: kr. 160,000 (80% of actual value)

- Loss: kr. 50,000

- Payout: kr. 50,000 × (160,000 ÷ 200,000) = kr. 40,000

- Out of pocket: kr. 10,000

This applies to every single claim — not just large ones. There is no minimum coverage percentage that shields you from the penalty.

For contrast: in the United States, property insurers typically require coverage of at least 80% of replacement value before applying a similar penalty. Denmark has no such threshold — underinsurance starts affecting payouts from the first krone of shortfall.

What Are "Good" Coverage Limits?

Good limits depend on your net worth, asset exposure, and income. A practical starting point: liability limits should roughly match your total household net worth — so a judgment against you doesn't reach personal assets beyond what the policy covers.

Recommended benchmarks:

- Auto liability: 100/300/100 as baseline for most consumers

- Home dwelling coverage: Full replacement cost, not market value

- Liability coverage: Match or exceed total household net worth

If you hold kr. 400,000 in assets but carry only kr. 100,000 in liability coverage, a kr. 250,000 judgment leaves kr. 150,000 of your personal wealth exposed — uncovered by your policy.

What Factors Should Determine Your Coverage Limits?

Selecting coverage limits means connecting your financial circumstances to real risk exposure—rather than accepting whatever the insurer suggests or the legal minimum requires.

Your Assets and Net Worth

The more you own, the more you stand to lose in a lawsuit or large claim. Higher assets justify higher limits, especially for liability coverage.

If you own a home, retirement accounts, and savings totaling kr. 3,700,000, carrying only the legal minimum liability coverage (often kr. 185,000–370,000) leaves over kr. 3,300,000 exposed to lawsuits. Minimum legal coverage rarely protects what you've actually built.

Your Risk Profile and Life Stage

Life changes directly affect what coverage levels are appropriate:

- Adding a teen driver increases accident likelihood

- Buying a home raises property coverage needs

- Starting a business creates new liability exposures

- Retiring may reduce income replacement needs but increase asset protection requirements

A policy adequate for a single renter can become dangerously insufficient once you own a home and have children. Reassess at each major life event — not just at renewal.

Budget vs. Long-Term Cost of Underinsurance

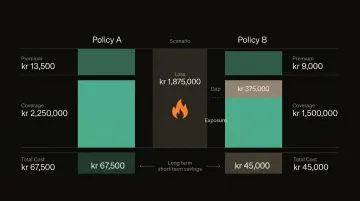

A policy costing kr. 7,500 less annually but leaving a kr. 1,500,000 gap in a claim is not savings — it's catastrophic financial risk.

Real-world example:

| Policy A | Policy B | |

|---|---|---|

| Annual premium | kr. 13,500 | kr. 9,000 |

| Dwelling coverage | kr. 2,250,000 | kr. 1,500,000 |

| 5-year premium total | kr. 67,500 | kr. 45,000 |

A kr. 1,875,000 fire loss under Policy B:

- Insurance pays: kr. 1,500,000

- You pay out of pocket: kr. 375,000

- Total 5-year cost: kr. 45,000 in premiums + kr. 375,000 gap = kr. 420,000

Policy A covers the entire loss for kr. 67,500 over five years. The "cheaper" policy ends up costing you kr. 352,500 more.

How Inzure Simplifies Insurance Comparison

Inzure is Denmark's first AI-powered, independent insurance platform—built because the insurance industry's complexity works against consumers, not for them. It operates as a neutral third party, with no ties to any insurer.

What Inzure Does in Practice

- Not affiliated with any insurer — analysis is fully independent

- GDPR-compliant EU data storage keeps your information secure

- No obligation to switch after receiving your recommendations

- Free to use; you only pay 20% of annual savings if you choose to switch

- Automated alerts notify you when better coverage or pricing becomes available

Real customer Hans Henrik Beck saved 48,000 DKK annually (a 46% reduction) after 8 years with Tryg. Lise Nielsen, 86, not only saved 24% but discovered critical coverage gaps across three policies, upgrading her protection while still paying less overall.

Frequently Asked Questions

What do policy limits like 100.000 kr./300.000 kr./100.000 kr. mean?

The three-number format shows: 100.000 kr. maximum per injured person, 300.000 kr. total per-incident bodily injury cap, and 100.000 kr. property damage maximum. If one person's claim exceeds 100.000 kr., the insurer pays no more than that cap — even if the per-incident total hasn't been reached.

What is the 80% rule in insurance coverage limits?

Danish policies use proportional underinsurance: if your insured value is lower than the actual replacement value, the insurer pays only a proportional share of any claim. There is no safe harbor threshold — any underinsurance reduces your payout. The "80% rule" is a U.S. concept that does not apply in Denmark.

What are good insurance coverage limits to choose when comparing policies?

Good limits depend on your personal assets and risk exposure. For home contents insurance (indboforsikring), coverage should meet or exceed the full replacement value of your belongings — underinsuring by even 20% can significantly reduce a payout. Review limits annually as circumstances change.

What is the difference between per-occurrence and aggregate coverage limits?

Per-occurrence caps the maximum paid for a single claim event; aggregate caps the total paid across all claims during the entire policy period. Once the aggregate is exhausted, you bear remaining costs out of pocket.

What happens if damages exceed your policy limits?

You become personally responsible for costs above the limit, meaning you pay out of pocket or face lawsuits against personal assets. Reviewing your limits regularly — and increasing them when your assets grow — is the most effective way to avoid this exposure.

How often should you compare and review your insurance policies?

At minimum, annually at renewal — but also after major life events like home purchases, income changes, or adding family members. Inzure monitors the Danish market continuously and alerts you when better coverage or pricing becomes available.