Introduction

Most Danish consumers compare insurance policies by glancing at the annual premium—and then choose the cheapest option. That instinct is understandable—but 68% of Danish switchers cite lower price as their primary motivation, and many end up overpaying or underinsured because coverage limits, exclusions, and deductibles never entered the comparison.

Insurers in Denmark intentionally make these metrics difficult to compare — and most online tools don't help, surfacing price while burying the details that determine whether a policy actually protects you. Coverage limits, deductibles, exclusions, and carrier reliability all shape what a policy is worth. Here's how to read past the premium.

Key Takeaways

- Premium is just the starting point — deductibles, coverage limits, and exclusions matter just as much

- Two policies at the same price can offer very different protection once exclusions are factored in

- Insurer reliability matters as much as price—check claims settlement records and satisfaction scores

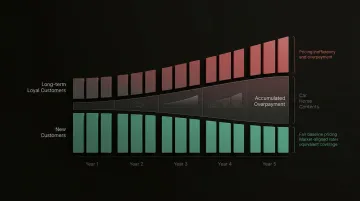

- Loyal customers in Denmark pay on average 1.108 kr. more per year than new customers for identical coverage

- AI tools can now analyse policies across multiple insurers in seconds — no manual comparison needed

Why Comparing Insurance Policies Online Is Harder Than It Looks

The insurance industry structures policies in ways that make direct comparison difficult—even when you're comparing the "same" type of coverage. Different terminology, bundled add-ons, and varying exclusion formats mean that two home insurance policies can look identical at first glance but deliver very different protection.

This creates an apples-to-oranges problem. Two policies may display the same annual premium yet differ significantly in what they actually cover:

- One carries a 5,000 kr selvrisiko (deductible); the other has 1,500 kr

- Bicycle theft coverage might be capped at 6,000 kr on one policy, 19,000 kr on another

- Water damage from an open window may be excluded on one but covered on the other

The cheaper-looking option can easily become the more expensive one when you actually make a claim.

19% of EU consumers report that comparison websites present information in misleading ways, largely because these tools overemphasise price and bury qualitative factors like coverage depth, exclusion clauses, and insurer reliability. EIOPA warns that comparison tools risk misleading consumers by ranking products primarily on cost rather than coverage quality or guarantees. Knowing which metrics actually matter is what separates a good policy decision from an expensive one.

The Key Metrics to Compare Insurance Policies Online

The following metrics, taken together, give a complete picture of policy value. Skipping any one of them can lead to a costly miscalculation.

Premium Price

The annual or monthly premium is the most visible metric, but it should always be evaluated relative to what it covers. A lower premium that comes with a high deductible or narrow coverage may cost significantly more at the point of a claim.

Context matters. Denmark has an annual non-life insurance switching rate of 14.5%—1.5 percentage points higher than the EU average. Yet 33% of Danish switchers make the move without conducting any market research or comparison. This blind switching behaviour often means choosing based on price alone, missing coverage gaps that only show up at claim time.

Deductible and Excess (Selvrisiko)

A deductible (selvrisiko) is the amount you must pay out-of-pocket before your insurer covers the rest. A higher deductible typically lowers your premium but raises your financial risk in a claim scenario.

Evaluate the trade-off with concrete numbers:

- Policy A: 500 kr/month premium with 5,000 kr selvrisiko

- Policy B: 550 kr/month premium with 1,500 kr selvrisiko

Policy A looks cheaper — until you make a claim. File one claim for 10,000 kr in stolen electronics: Policy A costs you 5,000 kr out-of-pocket plus 6,000 kr in annual premiums. Policy B costs 1,500 kr out-of-pocket plus 6,600 kr in premiums. The numbers flip.

Different insurers structure deductibles differently. GF Forsikring sets standard selvrisiko at 1,086 kr per claim, while Topdanmark allows customers to choose deductibles down to 0 kr on certain policies, and Tryg applies the chosen deductible to all claims uniformly.

Coverage Scope and Limits

Coverage scope defines which events and assets are protected — fire, theft, water damage, liability — and coverage limits cap the maximum payout. A policy with a lower limit may leave you partially uncompensated after a major loss.

Three details determine real-world outcomes:

- Which perils and scenarios are actually covered (fire, theft, water damage, liability)

- The maximum payout ceiling — both overall and per category

- Whether the insurer pays replacement value (today's purchase price) or actual cash value (depreciated worth)

These differences dramatically affect real-world outcomes. For example, Topdanmark covers bicycles up to 19,649 kr per bike, while Tryg's standard coverage caps bicycle theft at 6,000 kr. If your bike costs 15,000 kr and gets stolen, one policy fully covers you; the other leaves you 9,000 kr short.

Valuation methods matter too. Topdanmark and Tryg both offer "nyværdi" (replacement value) for items purchased new and less than two years old, meaning they'll pay the current purchase price for an equivalent new item. Older items are typically valued at "dagværdi" or "nytteværdi" (actual cash value), which factors in depreciation.

Policy Exclusions

Exclusions are the conditions, events, or circumstances explicitly NOT covered by the policy. These clauses are often buried in fine print, yet they're where most claim disputes and rejections originate.

Common exclusions Danish consumers frequently overlook:

- Home insurance: Water damage from open windows or doors, theft from unlocked homes (except trick theft), forgotten or misplaced items

- Travel insurance: Lost or left-behind luggage, functional errors on electronics over four years old, software and data loss

- Bicycle insurance: Theft when the bike wasn't locked properly or stored securely

Two policies with identical-looking coverage descriptions can have vastly different exclusion lists. Topdanmark excludes water damage from gutters and downpipes; another insurer might cover it. One travel policy excludes items over four years old; another might not. These differences are invisible when you're comparing price alone.

In 2024, the Danish insurance complaints board (Ankenævnet for Forsikring) received 1,898 complaints — home/property insurance accounted for 8.2% and family/contents insurance for 7.4%. Misunderstood exclusions drive a significant share of these disputes, which is why reading the fine print before a claim beats discovering gaps after one.

Claims Satisfaction and Insurer Reliability

Claims satisfaction measures how reliably and fairly an insurer pays out when you make a claim. It matters more than price. An insurer with low payout rates or long settlement times makes the policy effectively worthless.

Check publicly available data:

- Claims settlement ratios: What percentage of claims does the insurer approve?

- Customer satisfaction scores: Independent ratings from consumer organisations or aggregator reviews

- Average claims processing times: How long does it typically take to settle a claim?

According to the 2025 EPSI Rating Denmark (B2C customer satisfaction), the industry average for private customer satisfaction fell to 72.5 in 2025. Performance varies significantly by insurer:

| Insurer | EPSI Satisfaction Score | Change vs. 2024 |

|---|---|---|

| Vestjylland Forsikring | 84.4 | -1.1 |

| GF Forsikring | 83.3 | -1.2 |

| Topdanmark | 70.4 | -4.2 |

| Alm. Brand | 68.8 | -2.7 |

| Codan | 68.2 | -4.0 |

| Tryg | 68.0 | -4.7 |

A policy with a low premium but a satisfaction score of 68 may cost you far more in frustration, delays, and disputes than a slightly higher-priced policy with a score above 80.

Contract Flexibility and Price Adjustment Clauses

Contract flexibility covers cancellation notice periods, lock-in terms, and whether the insurer can raise premiums mid-term or at renewal without meaningful justification.

Check these details:

- Minimum notice period to cancel: Can you switch easily if you find a better deal, or are you locked in?

- Renewal pricing guarantees: Does the insurer commit to renewal rates, or can they increase prices arbitrarily?

- Unilateral term changes: Can the insurer change coverage or exclusions without your consent?

Loyal customers in Denmark frequently face "loyalty penalties" where annual price increases accumulate without corresponding improvements in coverage. Customers with 10+ years of seniority pay on average 7-8 percentage points more than new customers, which works out to roughly 1,108 kr more annually for car, home, and contents insurance combined.

This pricing behaviour has prompted regulatory scrutiny. In May 2025, Finanstilsynet required all private non-life insurers to continuously monitor pricing and implement measures to counter unreasonable pricing towards existing customers.

How to Avoid Common Comparison Mistakes

The Duplicate Coverage Trap

Many households hold multiple policies—home, contents, travel, car, health—that overlap in certain areas, meaning they're paying twice for the same protection.

Example: Your home contents policy already covers electronics theft up to 50,000 kr worldwide. But you also buy standalone travel insurance that covers electronics theft up to 20,000 kr. You're paying for overlapping coverage.

Approximately 11% of Danes hold at least two travel insurances, often due to credit card benefits they've forgotten about. Nearly one-third of Danish adults have a credit card that includes built-in travel and purchase insurance, yet many buy standalone policies on top of it.

Comparing Policies at Different Coverage Levels

A fair comparison requires that both policies cover the same set of risks, at equivalent limits, with comparable deductibles. Otherwise, the comparison produces a misleading price difference that disappears once you equalize the terms.

What this looks like in practice:

- Policy A covers bicycle theft up to 19,000 kr with a 1,500 kr deductible

- Policy B covers bicycle theft up to 6,000 kr with a 5,000 kr deductible

Policy B costs 200 kr less annually, but it's not the same product. You're comparing unequal coverage. Adjust both to the same limits and deductibles before making a price-based decision.

Ignoring the Renewal Price

The introductory rate offered to new customers is frequently lower than what the same policy costs at renewal. Forbrugerrådet Tænk found that house insurance premiums rose by an average of 26% over two years for existing customers.

Insurers adjust prices annually in line with wage developments — a pattern that pushes premiums up with little competitive pressure on loyal customers. If you haven't compared market rates in over a year, you're almost certainly overpaying.

How Inzure Makes It Easier to Compare the Right Metrics

Most Danish consumers never get a true multi-metric comparison of their insurance — not because the information doesn't exist, but because extracting it from policy documents takes hours. Inzure was built to fix that.

Inzure's platform reads and analyses existing insurance policies in 60 seconds. Upload your policy documents as PDFs or photos, and the AI identifies missing coverage, duplicate protections, and unjustified price increases, delivering the kind of multi-metric comparison that would otherwise take hours of manual research.

Key advantages for policy comparison:

- Works for you, not insurers — no affiliation with any Danish insurance carrier

- Stores your documents within the EU under GDPR-compliant data standards

- No obligation to switch — analyse your policies and walk away if you choose

- Monitors the market continuously and alerts you when a better deal appears

- Free to use, with a 20% commission only if you switch and actually save money

That combination of independent analysis and transparent pricing is what makes metric-based comparison actionable — not just informative. Early users have saved between 2,800 kr and 48,000 kr annually by acting on what the platform surfaces.

Conclusion

Choosing an insurance policy online requires comparing across at least six distinct metrics: premium, deductible, coverage scope, exclusions, insurer reliability, and contract flexibility.

At a glance, the metrics that matter most:

- Premium — what you pay monthly or annually

- Deductible — your out-of-pocket cost when you claim

- Coverage scope — what situations are actually covered

- Exclusions — where your protection ends

- Insurer reliability — how the company performs when it counts

- Contract flexibility — your ability to adjust or exit

Relying on price alone is the most common and most costly mistake Danish consumers make.

Policy comparison is not a one-time exercise, either. Coverage needs change, insurers raise prices at renewal, and the market shifts. Review your policies at minimum once a year — ideally before your renewal date — to catch price hikes and coverage gaps before they cost you. Platforms like Inzure automate this monitoring, flagging changes across Danish carriers so you always know what your coverage is actually worth.

Frequently Asked Questions

What are the key metrics of insurance?

The key metrics for consumers comparing insurance include premium price, deductible/excess, coverage scope and limits, policy exclusions, insurer claims reliability, and contract flexibility. Evaluating all six together gives a complete picture of policy value.

What should I compare when looking at insurance policies online?

Go beyond price and compare deductibles, what is and isn't covered, coverage limits, exclusion clauses, and the insurer's claims satisfaction record. These factors determine the real value you receive when you actually need to make a claim.

What is a deductible and how does it affect my premium?

A deductible is the amount you pay out-of-pocket before your insurer covers the rest. In Denmark, this is called selvrisiko. Policies with higher deductibles typically carry lower premiums, but expose you to greater financial risk at claim time.

How do I know if I'm paying too much for my insurance?

If your premium has increased at renewal without a change in your coverage or risk profile, or you haven't compared market rates in over a year, you're likely overpaying. Running a quick market comparison—using a tool like Inzure—takes about 60 seconds and shows what your current coverage actually costs elsewhere.

What does it mean if two policies have the same premium but different coverage?

Identical premiums with different coverage typically means one policy has a higher deductible, narrower scope, lower limits, or broader exclusions. That policy is effectively more expensive when you actually make a claim, even though the monthly cost looks the same.

How often should I compare my insurance policies?

Compare at least once a year, ideally before your renewal date. Insurers frequently apply price increases at renewal, and the market regularly offers better terms than what existing customers are charged.