Introduction

Most Danish consumers pay more for insurance than they should — not because they picked the wrong product, but because they never compared. Without benchmarking, there's no way to know if your premiums reflect current market rates or simply exploit your loyalty. Loyal customers with 10+ years of tenure at the same insurer pay an average 443 DKK extra annually for house insurance and 240 DKK extra for contents insurance compared to new customers with identical coverage.

Insurance peer analysis is the process of comparing your policy's price and coverage to what others pay for equivalent protection. Most consumers skip this step entirely. Skipping it costs thousands of kroner each year.

The Danish insurance market is structured to discourage that comparison. Policy documents average 32 pages, filled with terms designed to prevent you from asking questions. The complexity isn't accidental — it's a business model built on your confusion.

This guide walks through how peer analysis works, what to compare, and how to use benchmarking data to stop overpaying.

Key Takeaways

- Insurance peer analysis shows whether you're overpaying by comparing your policy against equivalent options on the market

- Loyal customers routinely overpay — 79% who negotiate their premiums achieve reductions, yet most never try

- Compare annual premium, sum insured, deductible, and coverage inclusions — including auto-renewal terms

- Platforms like Inzure automate the entire process in 60 seconds

What Is Insurance Peer Analysis?

Insurance peer analysis is a structured process of comparing your existing insurance policy against similar policies available in the Danish market to determine whether you're paying a fair price for the coverage you receive. It answers a simple question: are you getting good value, or are you paying a loyalty penalty?

The process applies to all common policy types:

- Home insurance (husforsikring)

- Contents insurance (indboforsikring)

- Accident insurance (ulykkesforsikring)

- Bundled family packages

Wherever you pay a recurring premium, peer analysis reveals whether that premium reflects current market pricing or an outdated rate that has crept up steadily without notice.

This article focuses on the consumer perspective — comparing your personal policies to market alternatives. Institutional peer analysis, used internally by insurers to benchmark their own products, follows different methodologies and serves different purposes.

Why Insurance Peer Analysis Matters for Danish Consumers

The Danish insurance market is deliberately opaque, making it difficult to see whether your premium reflects current pricing or a years-old rate that has quietly increased. This structural opacity creates four core consumer risks:

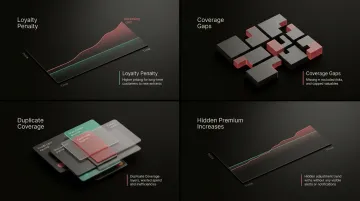

- Loyalty penalties: Insurers earn profit margins 7-8 percentage points higher on customers with 10+ years of tenure compared to new customers — long-term loyalty is penalised, not rewarded.

- Coverage gaps: Basement water damage from rising damp (grundfugt) is strictly excluded from most policies, and jewellery is typically capped at just 15% of your total sum insured. Policies that look comprehensive routinely exclude key scenarios.

- Duplicate coverage: 13% of Danes rely on travel insurance via credit cards without realising these policies carry strict limitations — and may overlap with standalone coverage they're already paying for.

- Unjustified premium increases: Premiums adjust annually against the private sector wage index, which historically outpaces standard inflation. Because this indexation is buried in standard contract terms, insurers face no legal obligation to notify customers directly of these increases.

Each of these risks compounds quietly over time. Peer analysis gives you the market context to spot them before they cost you more.

How Insurance Peer Analysis Works – Step by Step

Peer analysis follows a clear, repeatable process. Most consumers fail because they compare only price (ignoring coverage) or compare policies that aren't actually equivalent.

Step 1 – Document Your Current Position

Gather all existing insurance documents and record:

- Annual premium (the total you pay each year)

- Sum insured (the maximum payout amount)

- Deductible/excess (selvrisiko, meaning what you pay before the insurer covers anything)

- Key inclusions (what events are covered)

- Exclusions (what events are specifically not covered)

This baseline is critical. Without it, you can't measure whether alternatives offer better value or just different trade-offs.

Step 2 – Define Your Peer Group

Comparable means policies that cover the same risk type, similar sum insured amounts, and similar customer profiles. Comparing a contents policy with a 20,000 DKK sum insured to one with a 100,000 DKK sum insured produces a useless result — you'll end up optimizing for the wrong policy entirely.

Step 3 – Gather Market Data

Collect premium quotes and policy terms from multiple Danish insurers for equivalent coverage. This is where most consumers abandon the process: manually gathering quotes from Tryg, Topdanmark, Alm. Brand, Gjensidige, and GF Forsikring can take 10+ hours.

Step 4 – Compare Coverage and Price Side by Side

Evaluate not just the headline premium but coverage breadth:

- What events are included and excluded?

- What is the deductible?

- What does the claims process look like?

- Are there sub-limits on valuables, electronics, or specific categories?

The cheapest policy is rarely the best value. A policy that costs 500 DKK less annually but excludes water damage or caps jewellery claims at 10,000 DKK may leave you severely under-insured when you need protection most.

Step 5 – Act on the Findings

Use your comparison to:

- Renegotiate with your existing insurer (79% who try achieve reductions)

- Switch to a better-value provider

- Close gaps in coverage you've identified

Note why you made your decision, then schedule a reminder to repeat the analysis each year. Insurance markets shift, and your coverage needs change — a one-time comparison won't protect you long-term.

Key Metrics to Compare in an Insurance Peer Analysis

Annual Premium vs. Coverage Scope

Two policies priced identically may offer vastly different protection. One may cover burst pipes and theft with no sub-limits. Another excludes basement damage entirely and caps electronics claims at 15,000 DKK.

The comparison must factor in what events, amounts, and conditions are actually covered — before price becomes the deciding variable.

Deductible and Excess Levels

A lower annual premium often comes with a higher deductible, meaning you absorb more risk when claiming. Raising a contents insurance deductible from 0 DKK to 3,000 DKK yields an average 24.4% premium saving, but increasing it further to 5,000 DKK only saves an additional 9.5%.

The true value trade-off:

If a policy saves you 800 DKK annually but raises your deductible by 2,000 DKK, you need to avoid claims for 2.5 years just to break even. For low-frequency risks like home contents, a higher deductible often makes financial sense. For high-frequency risks like bicycle theft in Copenhagen, it may not.

Inclusions and Exclusions

Most consumers only discover exclusion gaps at claim time. Common exclusion categories in Danish policies include:

- Basement water damage from rising damp (grundfugt): claims are frequently denied when the cause is construction-related moisture rather than a sudden cloudburst

- Simple theft (simpelt tyveri) carries much lower limits than burglary (indbrudstyveri), which requires proof of forced entry — cash and jewellery are often excluded entirely

- Valuables such as jewellery and gold are typically capped at 15% of total sum insured per incident, with individual item limits often set at 15,000 DKK

Automatic Renewal Terms and Price Increase Clauses

Danish policies are subject to automatic annual price indexation, typically tied to the private sector wage index. Because this is a standard contract term, insurers aren't required to send explicit notifications when prices increase according to this index. Over years, these silent increases compound significantly — comparing renewal terms, not just current premiums, is critical to avoiding long-term overpayment.

How Inzure Can Help You Benchmark Your Insurance

Inzure is Denmark's first AI-driven, independent insurance platform that performs the entire peer analysis process in 60 seconds. The platform reads and analyses policies across all major Danish insurers — including Tryg, Alka, Topdanmark, Gjensidige, and others — without bias toward any provider.

Upload your policies as PDF documents or screenshots, regardless of which insurer issued them. Inzure's AI extracts coverage scope, premiums, deductibles, inclusions, and exclusions, then benchmarks them against current market alternatives. It consistently surfaces problems that manual comparison misses:

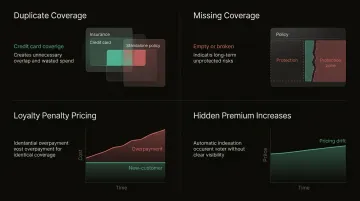

- Duplicate coverage across policies (such as overlapping travel insurance via credit cards and standalone policies)

- Missing coverage categories (customers have discovered they lacked home contents insurance for 10+ years)

- Loyalty-penalty pricing (identifying when you're paying more than new customers for identical coverage)

- Unjustified year-on-year premium increases from automatic indexation

Documented Savings

Customer savings range from 2,800 DKK annually (an 86-year-old who added missing coverage and still reduced costs by 24%) to 48,000 DKK annually (a 62-year-old family with 8 years at Tryg who achieved a 46% reduction).

How the Pricing Works

Inzure charges nothing upfront. The model is straightforward:

- Free to use with no insurer affiliations

- GDPR-compliant EU data storage

- 20% commission only if Inzure finds and facilitates a switch to a better deal

- If it finds better coverage at the same price — no charge

- If it finds no better option — no charge

You pay only when Inzure saves you money.

After the initial analysis, Inzure monitors the market continuously and notifies you only when pricing shifts or a better alternative appears — so you don't have to check manually every renewal cycle.

Frequently Asked Questions

What is the insurance peer analysis process?

Insurance peer analysis involves documenting your current policies, identifying comparable market alternatives, and systematically comparing coverage scope and pricing to determine whether you're receiving fair value. The process turns complex policy documents into side-by-side comparisons you can actually act on.

What is the purpose of insurance peer analysis?

The purpose is to give consumers an objective view of whether their premiums reflect current market rates, to expose coverage gaps or duplicates, and to support informed decisions about switching, renegotiating, or keeping existing policies.

How often should I benchmark my insurance policies?

Benchmark at least annually, ideally timed before policy renewal when you have maximum negotiating leverage. Significant life events — moving home, buying a car, having children, or retiring — should also trigger a fresh comparison, as your coverage needs and risk profile change.

What metrics matter most when comparing insurance policies?

Focus on annual premium, coverage scope, deductible level, exclusions, and renewal terms as core comparison variables. Price alone is an unreliable benchmark — a cheap policy with broad exclusions or high deductibles may cost far more when you actually need to claim.

How do I know if I'm overpaying for my insurance?

Without active comparison, there's no reliable way to know. Loyal customers tend to overpay due to loyalty penalties and incremental renewal increases that compound quietly year over year. If you haven't compared in over a year, there's a good chance you're paying above current market rates.

Can I do insurance peer analysis without a financial adviser or broker?

Yes. Consumers can benchmark independently using direct quotes and policy documents, though the manual process typically takes 10+ hours. Alternatively, platforms like Inzure automate the entire process in 60 seconds, with no obligation to switch and no commission tied to which policy you choose.