Introduction

Most Danish homeowners can switch their home insurance in a matter of days — yet many stay with the same insurer for years, paying far more than necessary. The reason? Insurance companies systematically make switching feel complicated — and loyal customers pay the price.

According to Konkurrence- og Forbrugerstyrelsen, customers who stay with the same insurer for 10 years pay 7-8 percentage points more than new customers for identical coverage. Forbrugerrådet Tænk estimates this loyalty penalty costs the average Danish household over DKK 5,000 per year.

The switching process itself is simpler than most people assume. This guide covers:

- Why so many Danish homeowners end up overpaying

- How to switch insurers, step by step

- When to time your switch for maximum savings

- What to evaluate before committing to a new policy

- The most costly mistakes to avoid

Key Takeaways

- You can switch home insurance any time — renewal is often most cost-efficient but not mandatory

- Secure your new policy before cancelling the old one — a coverage lapse can raise future premiums

- If your property loan requires proof of coverage, notify your bank before the switch completes

- The right question is whether you have adequate coverage at a fair market price — not just whether a competitor is cheaper

- AI-driven tools can analyse your policy for gaps, duplicates, and overpricing in 60 seconds — work that used to take hours of manual research

Why Homeowners Switch Insurance Companies

Danish homeowners switch for three primary reasons:

Rising Premiums and Loyalty Penalties Long-term customers pay more than new ones. The loyalty penalty is real — customers with 10 years' tenure pay DKK 2,400 more annually than new customers with identical coverage. The top five insurers control approximately 80% of the Danish market, giving them room to push through automatic premium increases tied to wage indices rather than actual risk.

Inadequate or Outdated Coverage Insurance needs change after renovations, new valuables, or life changes. With residential construction costs rising 2.6% year-over-year in Q4 2025 according to Danmarks Statistik, a policy taken out five years ago may no longer reflect the home's current replacement cost. Some insurers add exclusions or reduce limits at renewal without notifying policyholders clearly.

Poor Claims Experience or Non-Renewal Notices A slow or disputed claims process is often the moment homeowners realize their insurer isn't working for them. A non-renewal or cancellation notice compounds that frustration — and creates urgency. Finding a new policy quickly matters: a coverage lapse can trigger higher premiums and put you in breach of your mortgage agreement. The sections below walk through exactly how to make that switch without gaps or penalties.

How to Switch Home Insurance: A Step-by-Step Guide

The entire process typically takes less than a week when approached methodically. The order matters — the new policy must be activated before the old one is cancelled.

Step 1: Review Your Current Policy

Start with your homeowners insurance declarations page (forsikringspolice). It lists:

- Current coverage limits for dwelling, contents, and liability

- Deductible (selvrisiko) amounts

- Endorsements and optional add-ons

- Policy expiration date

- Annual or monthly premium

Understanding these details enables an accurate like-for-like comparison. Note whether your dwelling coverage reflects replacement cost (nyværdi) or actual cash value (dagsværdi), as this distinction can significantly affect claim payouts.

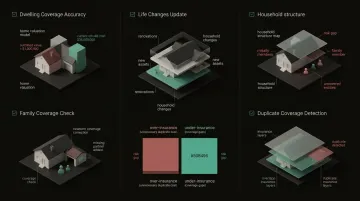

Step 2: Assess Your Actual Coverage Needs

Before comparing quotes, evaluate whether your existing coverage still matches reality:

- Does dwelling coverage reflect today's rebuild cost (not market value)?

- Have renovations, new purchases, or lifestyle changes occurred?

- Are any family members missing from the policy?

- Do you have duplicate coverages across multiple policies?

This step often reveals either over-insurance (paying for unnecessary duplicate protection) or under-insurance (critical gaps that leave you exposed). One Inzure customer discovered his newborn was being charged when children under 2 should be covered free, while his partner was completely missing from three separate policies.

Step 3: Compare Quotes from Multiple Providers

Get at least three quotes using identical coverage parameters. Information typically required includes:

- Property details (size, age, construction type, location)

- Personal information (age, occupation, claims history)

- Current insurer and coverage levels

Compare more than price alone. Evaluate:

- Deductible types (standard vs. peril-specific)

- Coverage method (replacement cost vs. actual cash value)

- Available endorsements (water backup, equipment breakdown, scheduled personal property)

- Insurer financial ratings (check ratings from Finanstilsynet or your insurer's own published solvency ratio)

Platforms like Inzure can shorten this process considerably. Upload your policy documents (PDF or photo), and the platform identifies coverage gaps, duplicate coverages, and pricing anomalies — then benchmarks your situation against real Danish market rates in about 60 seconds.

Step 4: Purchase the New Policy and Set the Start Date

The new policy's effective date should align exactly with (or slightly before) the cancellation date of the old policy. Never allow a gap between the two dates — even one day without coverage can:

- Raise your future premiums (insurers treat coverage gaps as risk flags)

- Violate your mortgage agreement

- Leave your home completely unprotected

Some homeowners set the new policy to begin the same day the old one expires to avoid both a lapse and duplicate premium payments.

Step 5: Cancel the Old Policy and Request Written Confirmation

Cancellation typically requires contacting the insurer directly by phone or in writing. Under Danish law, you have two cancellation options:

| Cancellation Type | When | Fee |

|---|---|---|

| Ordinary (Hovedforfald) | At least 1 month before annual renewal | None |

| Short-Rate (Kort Opsigelse) | Any time with 30 days' notice to month-end | DKK 74–81 (after year 1); DKK 484–810 (year 1) |

Request written confirmation of your cancellation date and any refund owed. Mid-term cancellation yields a prorated premium refund minus cancellation fees.

Step 6: Notify Your Mortgage Lender

If your home is mortgaged, notify your lender and provide a copy of the new declarations page. Danish mortgage lenders strictly require continuous building fire insurance (bygningsbrandforsikring) to protect their collateral. If insurance is paid through an escrow account, the lender will update payment instructions and adjust your monthly mortgage payments accordingly.

Skipping this step risks force-placed insurance (tvangsforsikring) — a lender-chosen policy that costs significantly more and protects only the lender's interest, not your equity or contents.

Key Factors to Evaluate Before Switching

Coverage Type and Limits

Replacement Cost (Nyværdi) vs. Actual Cash Value (Dagsværdi):

Replacement cost pays to repair or replace damaged property with new materials at current market prices without deducting for depreciation. Actual cash value pays replacement cost minus depreciation for age and wear. Choosing ACV purely to save on premiums can be financially damaging during a major claim.

Dwelling coverage must reflect current rebuild costs, not purchase price or market value. With construction costs rising 2.6% annually, a fixed-sum policy that isn't actively adjusted creates a dangerous protection gap.

Deductible Structure

Some policies include separate deductibles for specific perils (wind, hail, flood) that may not be immediately obvious when comparing headline premiums. A lower premium can obscure a much higher out-of-pocket cost during a claim.

According to Forbrugerrådet Tænk, raising a deductible from DKK 0 to DKK 3,000 reduces annual premiums by 24.4%, but increasing from DKK 3,000 to DKK 5,000 only yields an additional 9.5% reduction. The financial benefit diminishes at higher tiers.

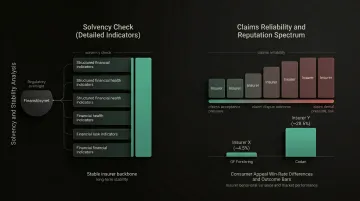

Insurer Financial Strength and Claims Reputation

Check insurer solvency via Finanstilsynet and review independent claims satisfaction data before committing. Ankenævnet for Forsikring data reveals significant variation in claims handling quality across Danish insurers.

Consumer win rates on appealed claims range from 4.5% (GF Forsikring) to 28.6% (Codan) — a gap that reflects how aggressively some insurers deny claims upfront. A lower premium from an insurer with poor claims handling creates risk that can easily outweigh the savings.

Endorsements and Exclusions

Not all policies cover the same perils or offer the same optional add-ons. Switching purely on price may inadvertently lose endorsements you relied on:

- Water backup coverage

- Equipment breakdown protection

- Scheduled personal property coverage (jewelry, art, electronics)

- Legal aid insurance (Retshjælp)

Many Danish insurers now offer "sumløs" (sum-less) contents insurance where you don't set a total maximum coverage limit. However, these policies still contain strict sub-limits — often just DKK 15,000 per piece of jewelry. Verify these sub-limits before switching.

Timing Relative to Policy Renewal

Switching at renewal avoids early cancellation fees (DKK 74-81 for most policies) and simplifies the refund process. However, if the premium increase at renewal is significant, the savings from switching immediately may outweigh cancellation costs.

Under Danish consumer protection law, you have a statutory 14-day cooling-off period when purchasing insurance via distance selling (online or phone). This period begins when you receive the policy conditions. If you cancel within this window, the purchase is voided without penalty.

Common Mistakes to Avoid When Switching

Creating a Coverage Lapse

Cancelling the old policy before the new one is active — even for a single day — is the most common and costly mistake. A coverage lapse can:

- Leave your home completely unprotected

- Invalidate mortgage agreement terms

- Result in higher premiums from the new insurer (coverage gaps are treated as risk flags)

- Trigger force-placed insurance from your lender at your expense

In Denmark, this isn't just good practice — it's a regulatory requirement. Insurers will not allow you to cancel building fire insurance unless you provide documented proof that a replacement policy has already been bound with a new carrier.

Switching Based on Price Alone

A lower premium may reflect reduced coverage limits, higher deductibles, or the absence of key endorsements. 2025 testing by Forbrugerrådet Tænk found no correlation between high premiums and superior coverage in the Danish market. Compare policies on a like-for-like basis, not just the headline figure.

Failing to Check Cancellation Fees

Some insurers charge a short-rate cancellation penalty where the refund is less than the pro-rata amount. Confirm exact refund and fee terms with your current insurer before switching. First-year cancellation fees can reach DKK 810, which significantly erodes any savings you expected to make.

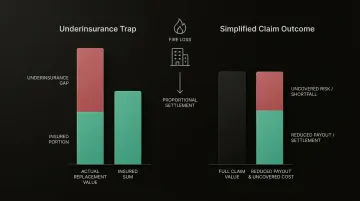

Ignoring the Underinsurance Trap

If your insured sum is lower than the actual replacement value, Danish insurers apply a proportional settlement rule:

Payout = (Insured Sum ÷ Actual Replacement Value) × Cost of Damage

Example: If your home's contents have a true replacement value of DKK 2,000,000 but your policy limit is DKK 1,000,000, you're 50% underinsured. In the event of a DKK 400,000 fire loss, the insurer will only pay DKK 200,000 (50% of the claim), leaving you to cover the rest.

This is known as "underforsikring" in Danish, and it applies the moment your coverage falls below 80% of full replacement cost. At that threshold, insurers will reduce every claim payout proportionally — not just total losses.

Conclusion

Switching home insurance is a manageable, well-defined process that most Danish homeowners can complete in under a week. The main risk isn't the act of switching itself, but doing it without proper preparation — particularly around coverage continuity and mortgage lender notification.

The decision to switch should begin with an honest check of whether your current policy delivers fair value — not a quote comparison. For many loyal policyholders paying the DKK 5,000 annual loyalty penalty, the answer is no. Platforms like Inzure turn that check from a 10-hour research project into a 60-second analysis, identifying gaps, duplicates, and overpricing before you even start comparing alternatives.

The Danish insurance market is designed to reward inertia and punish loyalty. Breaking that pattern starts with a single action: uploading your current policy and finding out what you're actually paying for.

Frequently Asked Questions

Does it cost money to switch homeowners insurance?

Switching itself is typically free, but cancelling a policy mid-term may incur a short-rate fee (74–81 kr. for policies held over a year, 484–810 kr. in the first year). Unused prepaid premium is usually refunded on a prorated basis, and new insurers don't charge start-up fees.

Can I switch my homeowners insurance at any time?

Yes, you can switch at any point during the policy term — not just at renewal. However, switching at renewal avoids potential cancellation fees and simplifies the transition, making it the preferred timing unless mid-term savings justify the cancellation cost.

Do I need to cancel home insurance when switching provider?

Yes, the old policy must be formally cancelled — it will not automatically lapse when a new policy is purchased. Always cancel after the new policy is active, obtain written confirmation of cancellation, and verify whether a refund is owed.

How to switch insurance companies with a mortgage?

Homeowners with a mortgage must notify their realkreditinstitut or bank, provide the new policy documentation, and ensure insurance payments are redirected accordingly. Skipping lender notification can trigger force-placed insurance at your expense.

Do I have to tell my mortgage lender if I change insurance?

Yes, this is typically a requirement under Danish realkreditaftaler. The lender needs proof of continuous adequate coverage. Failure to notify them can result in the lender purchasing their own policy (tvangsforsikring) on your behalf at your expense.

What is the 80% rule for homeowners insurance?

The 80% rule (or "underforsikring") means insurers require homes to be insured for at least 80% of full replacement cost value for claims to be paid in full. Insuring below this threshold triggers proportional settlement, meaning the insurer pays only a proportional share of any claim and the homeowner covers the rest.