Introduction

Every autumn, thousands of Danish homeowners receive their annual insurance renewal notice, glance at the premium, and sign it without reading the fine print. If this sounds familiar, you're not alone — it's what insurers count on.

Your life, home, and risk profile change every year, but your policy stays static unless you actively review it. Unless you push back, the same outdated terms renew automatically.

You might have renovated your kitchen, acquired valuable jewelry, or seen construction costs spike — yet your coverage limits haven't budged. The result? Under-coverage and overpayment often occur at the same time.

According to the European Insurance and Occupational Pensions Authority (EIOPA), only 17% of Europeans hold adequate coverage for property damage from natural catastrophes. Meanwhile, a 2025 report by Konkurrence- og Forbrugerstyrelsen (KFST) reveals that 17% of Danish home insurance customers pay a "high" or "very high" profit margin simply for being inactive, loyal customers.

The five questions below give you a concrete checklist for your next renewal — designed to surface gaps, exclusions, and pricing problems before they cost you.

Key Takeaways

- Your home's rebuild cost and market value are not the same — policies based on outdated estimates leave you exposed

- Flood, earthquake, and sewer backup are commonly excluded from standard policies — most homeowners don't find out until they file a claim

- High-value items like jewelry and electronics have strict sublimits and may need separate coverage

- Long-term customers typically pay more, not less — switching or renegotiating can cut premiums by hundreds of kroner annually

Question 1: Is Your Home Insured for What It Would Actually Cost to Rebuild?

Rebuild Cost vs. Market Value

Your home's market value and its rebuild cost are not interchangeable. Market value includes land, location trends, and buyer demand. Rebuild cost reflects materials, labor, and construction only — and in practice, one can run far higher than the other.

According to Statistics Denmark, residential construction costs surged 24.1% from Q4 2020 to Q4 2025. If your policy was set three years ago and hasn't been adjusted, you're likely underinsured.

Nyværdi vs. Dagsværdi

Danish policies use two main valuation types:

- Nyværdi (Replacement Cost Value): Pays the full cost to rebuild with like materials, no depreciation

- Dagsværdi (Actual Cash Value): Pays rebuild cost minus depreciation for age, wear, and reduced usefulness

Nyværdi typically applies to items less than two years old, purchased new, and undamaged. Older items fall under Dagsværdi, meaning payouts are reduced by strict depreciation schedules. Look for the terms "nyværdi" and "dagsværdi" in your policy's general conditions — the section is usually titled Erstatning (Compensation).

The Co-Insurance Trap

Which valuation method applies matters less if your insured sum is too low to begin with. When the declared value falls significantly below the true rebuild cost, your insurer may apply a proportional reduction — even for partial losses.

Topdanmark's policy explicitly states: "If the value of the entire contents is twice as large as the sum insured, a claim will only be compensated with half of the loss."

Where to check: Your declarations page (policens forside) lists your coverage limit. Compare it against a professional rebuild estimate or your insurer's replacement cost calculator — if the numbers don't match, contact your insurer to adjust the sum before your next renewal.

Question 2: Are Your High-Value Possessions Fully Covered?

Standard home insurance policies impose strict sublimits on specific categories of personal property — commonly jewelry, art, watches, musical instruments, collectibles, and electronics.

Standard Sublimits Across Danish Carriers

| Item Category | Sublimit (Major Carriers) |

|---|---|

| Jewelry, gold, silver, pearls | Max 10% of total sum insured |

| Cash and money equivalents | Max 2% of total sum insured |

| Bicycles | Typically capped around 17,000 DKK |

If you have 500,000 DKK in total coverage, your jewelry protection is capped at just 50,000 DKK — regardless of actual value.

But sublimits aren't the only risk. Where and how theft occurs can reduce your payout further — or eliminate it entirely.

Context Matters: Burglary vs. Simple Theft

Coverage often drops to zero in these situations:

- Items stolen from basement storage or unapproved garages

- Home left unoccupied for more than 2–6 months

- Theft through an unlocked door (simple theft) rather than forced-entry burglary

What to Do

Add a særforsikring (itemized rider) that covers each high-value item individually at its documented replacement value. Maintain a home inventory — video or photo-based — with receipts or appraisals to back up any future claim.

Question 3: What Does Your Policy NOT Cover?

Policy exclusions are among the most misunderstood areas of home insurance. Insurers are not required to explain what is excluded — the burden falls on you.

Universally Excluded Perils

Flooding and earthquakes are excluded from standard policies. Flooding covers heavy rainfall, storm surge, and overflowing waterways — each requiring a separate policy. Extreme events may fall under Denmark's government-backed Naturskaderådet scheme, though it only activates for events occurring less than once every 20 years.

Less Obvious Exclusions

Standard Danish policies exclude:

- Sewer or drain backup (unless caused by a qualifying heavy rain event)

- Mold and dampness damage

- Gradual leaks and wear-and-tear damage

- Pest or rodent damage

- Damage from running a home-based business

The Wear-and-Tear Clause

Insurers only cover sudden, accidental losses — not damage from lack of maintenance or gradual deterioration. A roof that slowly deteriorates? Not covered. A roof destroyed in a storm? Covered.

The same logic applies to heavy rain (skybrud), which has a strict threshold: coverage only applies if precipitation exceeds 15mm in 30 minutes or 40mm in 24 hours. Many homeowners assume any storm qualifies — it doesn't.

Where to check: Find the exclusions section in your policy document. For any gap that concerns you, ask your insurer directly whether a rider (tillægsdækning) exists — not all are advertised.

Question 4: Is Your Liability Coverage Actually Enough?

Liability coverage (ansvarsdækning) protects you financially if someone is injured on your property or if you accidentally cause damage to a neighbor's property. Standard policies include a default liability limit — often set when you first signed up, and rarely reviewed since.

When Standard Limits Fall Short

These situations come up more often than most homeowners expect:

- A guest slipping on icy steps

- A neighbor's fence damaged by a fallen tree

- A dog bite incident requiring medical treatment

Standard Danish liability limits typically include:

| Coverage Type | Typical Limit |

|---|---|

| Personal injury | Up to 10,000,000 DKK |

| Property damage | 2,000,000 - 3,000,000 DKK |

| Legal defense | Up to 225,000 DKK (with 10% deductible, minimum 2,500 DKK) |

If a single legal case runs past these limits — and complex personal injury claims can — the remaining costs come out of your own pocket.

Umbrella or Excess Liability

Standalone umbrella policies are not standard consumer products in Denmark. Your best protection is a comprehensive indboforsikring paired with any mandatory statutory insurances your situation requires — for example, dog owners must carry hundeansvarsforsikring by law. When reviewing your policy, check both the liability limits and whether any specific risks in your household are covered separately.

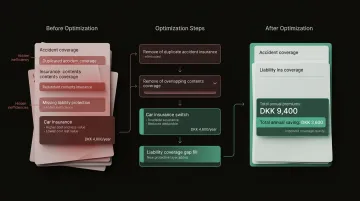

Question 5: Are You Paying What Your Policy Should Actually Cost?

The Loyalty Penalty

Insurers offer their best prices to attract new customers, while long-standing customers see premiums creep up each year. This is not a coincidence — it's a structural feature of the market.

A 2025 KFST report reveals that 17% of Danish home insurance customers pay a "high" or "very high" profit margin for being inactive. After 10 years with the same provider, customers can pay up to 2,400 DKK more annually than new customers for identical coverage.

The Opacity Problem

Your insurer will not proactively tell you that you're paying above-market rates. Comparing policies manually across providers is time-consuming and confusing. That complexity is not accidental — it's what keeps customers from switching.

Discount Categories

Insurers rarely apply these discounts automatically. Common categories include:

- Bundling home and auto policies

- Installing security systems or smoke detectors

- Maintaining a claims-free history

- Paying annually rather than monthly

You must often request these discounts explicitly.

What Is the Real Market Price?

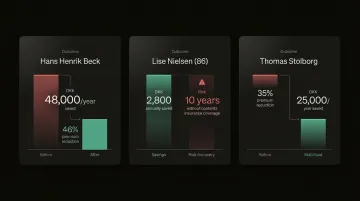

The real market price is what a new customer with your risk profile would pay today for equivalent coverage. Knowing this number is the only way to determine whether your renewal quote is fair.

Inzure is an independent platform that analyzes your existing policy in 60 seconds and shows you what the same coverage would cost from other Danish carriers today — with no obligation to switch. For homeowners who suspect they're overpaying but aren't sure where to look, that kind of neutral comparison gives you a concrete starting point.

What to Do Once You Have the Answers

Prepare Before Contacting Your Insurer

Document each gap or concern identified from the five questions. Structure the conversation around specific issues rather than vague inquiries — vague questions tend to result in vague answers.

When to Review Beyond Annual Renewal

Conduct a mid-year check after major life events:

- Renovations or home improvements

- New valuable purchases (jewelry, art, electronics)

- Marriage or divorce

- Taking on a lodger or tenant

- Starting a home-based business

Failing to notify your insurer after these changes can leave you underinsured — or give them grounds to dispute a claim.

Your Insurer Is Not a Neutral Advisor

Your insurer's interest is in retaining the policy at the current premium — not in finding you the best outcome. Before accepting renewal terms, cross-check your coverage and pricing using an independent source. Platforms like Inzure analyze your existing policy against the Danish market without any affiliation to the insurers themselves, giving you a clearer picture of what you're actually getting — and what you're overpaying for.

Frequently Asked Questions

What should I avoid saying when filing a home insurance claim?

Avoid admitting fault, speculating about the cause of damage, accepting the first settlement offer without review, or giving statements before understanding your rights. Many Danish policy terms include clauses where admitting fault may affect your coverage — always check your specific betingelser before speaking with your skadebehandler.

How often should I review my home insurance policy?

Review annually at renewal, or immediately after significant life changes such as renovations, new valuable purchases, marriage, divorce, or starting a business. These events directly impact coverage needs and should trigger an immediate policy check.

What is the difference between replacement cost and actual cash value coverage?

Replacement cost (Nyværdi) pays the full amount to rebuild or replace with comparable materials, while actual cash value (Dagsværdi) deducts depreciation based on age, wear, and reduced usefulness. Nyværdi typically costs more in premiums but delivers higher payouts at claim time.

What does standard home insurance typically not cover?

Most standard policies exclude flooding, earthquakes, sewer backup, mold, pest damage, and wear-and-tear damage. Each of these risks requires either a separate policy or an added rider to your existing coverage.

Can I lower my home insurance premium without cutting coverage?

Yes. Install security systems, increase your deductible, ask about claims-free discounts, bundle complementary policies (such as indboforsikring with rejse- or ulykkesforsikring), and use an independent platform to benchmark your premium against market rates. Data from Denmark's Consumer and Competition Authority (KFST) suggests most existing customers who negotiate can secure a meaningful discount.

What happens if I'm underinsured when I make a claim?

If your insured sum is below the rebuild cost, your insurer may only pay a proportional share of the claim — leaving you to cover the shortfall out of pocket, even for a partial loss. In Denmark, this is governed by the underforsikringsreglen (proportional settlement rule).