The result? Thousands of Danish households are quietly overpaying for coverage they don't need, or dangerously underinsured for risks that matter most. A study by Konkurrence- og Forbrugerstyrelsen revealed that customers loyal to the same insurer for 10+ years pay 443 kr more per year for house insurance and 240 kr more annually for contents insurance compared to new customers with identical risk profiles — all for the exact same coverage.

This article explains exactly how often you should review your insurance coverage, which life events demand an immediate check, what to look for during each review, and what it costs you to skip this critical task.

Key Takeaways

- Review all insurance policies at least once per year, ideally when renewal notices arrive

- Major life changes (marriage, new child, home purchase, job switch) require an immediate review regardless of timing

- A proper review catches coverage gaps and duplicate policies before a claim exposes them

- You likely don't know whether your premiums reflect fair market rates — a review tells you exactly where you stand

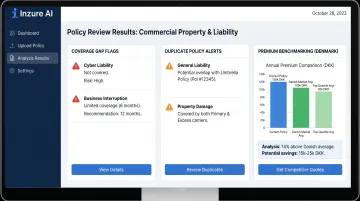

- Inzure's AI reads your policies in 60 seconds and flags gaps, overlaps, and overcharges — free to use, with no obligation to switch

Why Reviewing Your Insurance Coverage Actually Matters

Danish insurance policies are written to protect insurers, not consumers. Terms change quietly at renewal, premiums creep upward for loyal customers, and coverage gaps accumulate over time — often invisible until you file a claim.

According to Konkurrence- og Forbrugerstyrelsen's 2025 market analysis, Danish insurers systematically charge long-term customers 7-8 percentage points more than new customers for identical coverage — a measurable loyalty penalty. House insurance customers with 10+ years tenure overpay by 443 kr per year; home contents customers pay an extra 240 kr annually. Yet 75% of Danish consumers have never negotiated their premiums, and most haven't compared policies in over two years.

Skipping regular reviews creates two-sided financial risk:

- Underinsurance: Your coverage falls short of what you actually need. Construction costs in Denmark have risen 19.3% since 2021 (Danmarks Statistik), yet insurance sums aren't consistently index-regulated. A home valued at 2 million kr for rebuilding in 2021 now costs approximately 2.39 million kr — a 390,000 kr gap if the policy was never updated.

- Overinsurance: You pay for duplicate or unnecessary coverage. Approximately 425,000 Danes hold two or more travel insurance policies simultaneously, according to a YouGov survey for Nordea — wasted entirely when the same protection is already bundled with a credit card or another policy.

Either way, you're paying the wrong amount for the wrong coverage — and insurers won't be the ones to tell you.

Danish insurers are not required to notify you when they quietly increase premiums through index-regulation clauses, nor will they flag when your coverage no longer matches your needs. The responsibility falls entirely on you to proactively check.

Regulators have taken notice. Finanstilsynet sent mandatory letters to all insurers in May 2025 requiring continuous pricing fairness monitoring, while Konkurrencerådet launched a formal market investigation with binding-order powers the following month.

How Often Should You Review Your Insurance Coverage?

The short answer: at least once per year. But the right frequency depends on how stable your life is. Consumers experiencing active change need to review more often.

Based on Life Stability

For stable situations — no new assets, no family changes, consistent income — an annual review at renewal time is the bare minimum. This once-yearly check allows you to:

- Catch premium increases (even those buried in index-regulation clauses)

- Identify newly available discounts you now qualify for

- Verify coverage limits still reflect your actual property and asset values

- Compare your current premium against real market rates

Even in stable years, the market shifts around you — new carriers enter, pricing models change, and the policy you signed three years ago may no longer be competitive.

For periods of active change — buying property, starting a family, changing jobs, or making major purchases — review every 6 months or immediately after each significant event. Insurance needs can shift faster than the annual renewal cycle allows. Waiting 11 months to discover your newborn isn't covered, or that your home renovation increased rebuilding costs beyond your policy limit, leaves you uninsured at the moment you need coverage most.

Based on Policy Type

Different policies operate on different timelines:

- Home insurance (indboforsikring) renews annually — use that date as your review trigger

- Travel insurance (rejseforsikring) should be checked before any major trip or change in travel habits

- Accident and liability insurance warrants a review after family composition changes (new child, elderly relative moving in)

- Bicycle theft coverage is easy to overlook — verify limits if you've upgraded your bike

- Bundled or family plans need assessment together to catch overlapping or missing coverage across your full portfolio

Forbrugerradet Tænk recommends Danish consumers compare and re-shop insurance policies at least every two years to avoid loyalty penalties and pricing drift.

The "Renewal Notice" Trigger

A renewal notice is not administrative paperwork to ignore — it's your signal to actively compare pricing and coverage. Danish insurers frequently change terms or increase premiums at renewal without explicit notification beyond the renewal document itself. Consumers who auto-renew without reading miss these changes entirely.

When the renewal notice arrives:

- Read the entire document (don't just check the payment amount)

- Compare the new premium to last year's

- Check whether coverage limits or terms changed

- Benchmark against current market rates

Inzure users who run an analysis at renewal typically spot premium increases of 8–15% that appeared with no direct notification — catching these early is the difference between paying market rate and subsidizing someone else's discount.

Life Events That Should Trigger an Immediate Insurance Review

Certain events change your risk profile overnight, leaving your existing policy inadequate well before your next scheduled review.

Marriage or Divorce

Combining households changes both assets and liabilities. When you marry:

- Policies may need to be merged under one provider to capture bundle discounts

- Beneficiaries and named persons must be updated across accident and liability insurance

- Duplicate coverages (two separate travel policies, overlapping liability insurance) should be eliminated

Divorce has the opposite effect. Coverage previously shared now needs separation. Partners must be removed from policies, beneficiaries updated, and individual coverage gaps filled where shared protection previously existed.

Having or Adopting a Child

A new dependent dramatically increases financial risk. When a child arrives:

- Accident insurance (ulykkesforsikring) coverage amounts typically need to increase to protect the child's financial security

- Family coverage plans must be reviewed to include the new family member

- Liability coverage becomes more critical as children introduce new risks

Many Danish families only discover coverage gaps after the fact — a new child often changes what your existing policy covers, and the details vary significantly between carriers.

Buying, Renovating, or Selling a Home

Property transactions change what needs to be insured and for how much. Each scenario requires a different action:

- Buying requires new property insurance with accurate rebuilding cost estimates. Many buyers accept the lender's suggested coverage amount without verifying it reflects actual construction costs.

- Renovating increases rebuilding cost. A kitchen renovation adding 200,000 kr in value means your insured sum must increase by the same amount — or you'll be underinsured if damage occurs. With construction costs up 19.3% since 2021, even minor improvements can create significant gaps.

- Selling means your property policy must be cancelled or transferred. Overlapping coverage on a sold property wastes money. Insufficient coverage on a new one creates risk.

Significant Income Change or Job Switch

Two scenarios demand immediate review:

Salary increase means more income to protect and potentially higher-value assets requiring updated coverage limits. Your accident insurance from five years ago likely no longer reflects your current earning capacity.

Job change often means employer-provided group insurance doesn't transfer. This is one of the most commonly overlooked gaps. Danes switching jobs frequently lose coverage for weeks or months between employers without realising it, or discover their new employer's coverage is inferior to what they previously had.

Major Purchases (Bicycle, Jewelry, Electronics, Art)

High-value items often exceed the standard limits in most home contents policies. A 30,000 kr bicycle, expensive jewelry, or a valuable art collection typically requires a separate rider or endorsement to be properly covered. Standard policies cap coverage for these categories — often at just 15,000 kr — leaving the remainder uninsured.

What to Look for During an Insurance Review

A review isn't glancing at the premium amount and moving on. It's a structured check of what you're actually paying for and whether it still makes sense.

Coverage Limits vs. Current Asset Value

Coverage limits set years ago rarely reflect current replacement costs. Construction costs in Denmark rose 19.3% between 2021 and Q4 2025, while general business-to-business prices actually declined 1.6% in the same period — creating a 4.1 percentage point gap.

The problem: Danish insurers consistently index-regulate premiums (what you pay goes up), but insurance sums are not consistently index-regulated (what's covered stays flat). You pay more each year for coverage that's actually shrinking in real purchasing power.

What to check:

- Does your home's insured sum match current rebuilding costs (not market value)?

- Have you updated coverage for renovations, additions, or improvements?

- Do personal property limits reflect what you actually own?

With 94% of Danes holding home insurance, the gap between insured value and actual replacement cost is one of the most expensive mistakes to discover after a claim.

Duplicate or Overlapping Coverage

Many Danes unknowingly pay for the same coverage twice. Approximately 425,000 people — 11% of the population — hold at least two travel insurance policies simultaneously. Around 20% already have travel coverage via credit cards (Mastercard Gold/Platinum), yet pay separately for standalone policies.

Common duplicates to check:

- Travel insurance through credit cards, employer benefits, and standalone policies

- Liability coverage bundled into multiple products

- Accident insurance overlapping between family and individual policies

- Contents insurance on items already covered under other policies

A proper review surfaces all active policies and eliminates redundancies that directly reduce your annual premium without sacrificing protection.

Gaps in Coverage

The most common and dangerous gap: extended water damage coverage (udvidet vandskadedækning). Only 63% of home-insured Danes had purchased this protection by 2024, up from just 40% in 2020 — still leaving over one-third exposed. Between January 2023 and June 2025, over 131,000 weather-related claims were reported to Danish insurers, with 3 out of every 100 adult Danes experiencing home damage during this 2.5-year period.

Other frequent gaps:

- No liability umbrella policy despite rising net worth

- Missing coverage for high-value personal items (bicycles, jewelry, electronics)

- Excluded flood or water damage (often not included in standard home policies)

- Absent legal aid coverage (retshjælpsforsikring)

- Family members not properly included

Gaps are invisible until you file a claim and discover you're not covered — at which point the only option is to pay out of pocket.

Premium Fairness Check

Loyal customers frequently pay more than new customers for identical coverage. Insurers reserve competitive pricing for new sign-ups, then quietly increase premiums for existing customers over time through index regulation and annual adjustments.

After 10 years with the same insurer, Danish customers pay an average loyalty penalty of 443 kr per year on house insurance and 240 kr per year on contents insurance — a combined 683 kr annually just for staying put. One documented case showed a Tryg customer loyal for 20 years who saved 8,000 kr per year by switching to equivalent coverage elsewhere.

The central question your review needs to answer: are you paying the actual market rate, or a loyalty-penalised one? This step alone typically uncovers the largest savings.

That comparison used to require hours of manual research across multiple carriers. Inzure's AI runs the same analysis in 60 seconds — free, with no obligation to switch — and flags whether your current rate holds up against the market.

The Real Cost of Skipping Your Insurance Review

Underinsurance creates out-of-pocket disaster risk. If a claim occurs and your coverage limit is too low — because your property value increased, construction costs rose, or you made improvements without updating the policy — you personally pay the difference.

Example: Your home was insured for rebuilding at 2 million kr in 2021. Construction costs rose 19.3% by late 2025, meaning actual rebuilding now costs 2.39 million kr. A total loss leaves you 390,000 kr short unless you updated your insured sum. That's not a theoretical gap — it's money directly out of your savings.

Overpayment builds quietly across years. The loyalty penalty documented by KFST — 683 kr per year across house and contents insurance — becomes 6,830 kr over 10 years on just those two policies. The more extreme case of 8,000 kr annual overpayment translates to 80,000 kr wasted over a decade.

Put that in context: Danish households spend an average of nearly 16,000 kr per year on non-life insurance — 4.4% of total household consumption. Even a modest 10% reduction saves 1,600 kr annually, or 16,000 kr over a decade — enough for a family holiday or a solid emergency fund contribution.

The emotional cost of discovering gaps during a crisis cannot be quantified in kroner. Finding out — when you need it most — that any of these apply hits harder than the financial loss alone:

- Your newborn isn't covered under your existing policy

- Your bicycle theft falls outside your current plan

- Your renovated kitchen exceeds your policy's coverage limit

By the time you discover the gap, the window to fix it has already closed.

How to Make Your Insurance Review Faster and Easier

Set up your review system once:

- Create a recurring calendar reminder tied to your main renewal date each year

- Keep a running log of life changes throughout the year: new purchases, address changes, family events, renovations

- Store all policy documents in one digital folder (PDFs and summaries)

This preparation means your annual review doesn't start from scratch — you already know what changed.

Before each review, gather:

- All current policy documents and coverage summaries

- Premium invoices from the past 12 months

- Basic inventory of major assets (home value, vehicle value, high-value possessions)

- Notes on any life events since your last review

Many consumers discover during this step that they have policies they'd forgotten about — or that they're missing coverage they assumed they had.

Done manually, this process takes 10+ hours — reading dense policy documents, decoding terminology, comparing pricing across carriers, and tracking down gaps or duplicates. Inzure cuts that to 60 seconds.

Upload your policies as PDFs or screenshots and the AI handles the rest:

- Extracts and analyses your coverage details across all policies

- Benchmarks your premiums against real-time data from Tryg, Topdanmark, Alka, and other Danish carriers

- Identifies gaps such as missing bicycle theft coverage, absent legal aid, or excluded family members

- Flags duplicates like overlapping travel insurance or redundant liability coverage

- Shows you the actual market price for your coverage — with no obligation to switch

The analysis is free. Inzure only charges if you switch and save (20% of the annual savings achieved). If no better deal exists, the service costs nothing.

Because Inzure operates independently of all insurers, recommendations are based on your interests alone. Your data is GDPR-compliant, stored within the EU, and never shared with insurers unless you explicitly authorise a switch.

Frequently Asked Questions

How often should I review my insurance policy?

Review all policies at least once per year when renewal notices arrive. Major life changes — marriage, children, property purchases, or job switches — require an immediate review regardless of when you last checked. Stable situations allow annual reviews; active life changes demand checks every 6 months.

How often should you review your homeowners insurance policy?

Homeowners insurance needs annual review at renewal, plus immediate checks after any renovation, major purchase, or significant property value change. Construction costs in Denmark rose 19.3% between 2021 and 2025, so rebuilding cost estimates become outdated faster than most homeowners expect.

What is an insurance coverage review?

An insurance review is a structured check of your policies to confirm that coverage limits, exclusions, and premiums still match your actual situation. It surfaces dangerous gaps, duplicate coverage across policies, and loyalty-penalty overpayment compared to current market rates.

What life events should trigger an immediate insurance review?

Marriage or divorce, having or adopting a child, buying or renovating a home, changing jobs, significant income changes, and major purchases like bicycles, jewelry, or valuable electronics all warrant an immediate review.

What should I check when reviewing my insurance coverage?

Focus on four areas:

- Coverage limits — do they reflect current replacement costs?

- Dangerous gaps — missing liability, flood coverage, or high-value item riders

- Duplicate coverage — overlapping travel or accident policies you're paying for twice

- Premium fairness — whether your rate reflects the market or punishes long-term loyalty

See what your insurance actually costs on the open market. Upload your policies to Inzure for a free 60-second analysis — no obligations, no hidden fees, just a clear picture of your coverage gaps and whether you're overpaying.