Introduction

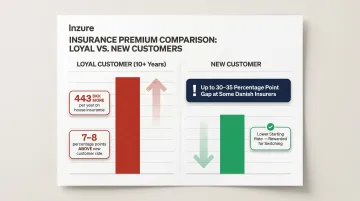

Danish consumers with 10+ years of loyalty pay an average of 443 DKK more per year for house insurance and 240 DKK more for contents insurance compared to new customers with identical risk profiles, according to the Danish Competition and Consumer Authority's 2025 findings. This loyalty penalty isn't an accident—it's part of a broader structural problem in which insurance complexity, automatic renewals, and invisible policy overlaps systematically drain money from Danish households.

Insurance complexity is the business model, not a side effect of it. Policies are written in dense legal language, distributed across multiple products, and renewed annually using wage-indexed pricing clauses that rarely require individual notice.

The result: consumers routinely pay for duplicate travel coverage already included with credit cards, accident protection their employer already provides, or comprehensive coverage on assets whose replacement value no longer justifies the premium.

This guide targets the specific waste that accumulates quietly — overlapping policies, coverage that no longer fits your life, and the pricing penalty insurers impose on long-term customers. You'll learn how to audit what you already have, identify what to cut, and challenge your insurer's pricing before the next renewal.

Key Takeaways

- Unnecessary insurance costs accumulate gradually — through duplicate policies, auto-renewals, and loyalty price inflation — not from one obvious mistake

- Overlapping coverage, policies left unchanged after major life events, and quiet premium hikes on loyal customers are where most overpayment hides

- Audit what you already have before buying, bundling, or renewing — that single step prevents most unnecessary spending

- Switching providers, adjusting coverage levels, and monitoring annual price changes are the actions that produce real savings

- A 60-second AI analysis can surface duplicates and overpricing that most manual reviews overlook

How Unnecessary Insurance Costs Typically Build Up

Unnecessary insurance spending rarely announces itself as one obvious mistake. Instead, it compounds through auto-renewals, policy stacking, and incremental premium increases that go unnoticed year after year. The Danish Competition and Consumer Authority notes that most Danish consumers haven't obtained new quotes or considered switching in the last two years, letting these costs compound unnoticed.

Three cost drivers typically do the most damage:

- Duplicate coverage — a credit card travel benefit, an employer's accident policy, or a home contents clause can duplicate coverage you're already paying for separately

- The loyalty tax — insurers index premiums to the private sector wage index, which historically rises faster than consumer price inflation, so loyal customers pay more every year without realising it

- Static coverage sums — while premiums climb, the actual protection often stays fixed, meaning you pay progressively more for coverage that's worth progressively less in real terms

Most of these overlaps are invisible at the point of purchase. European insurance regulators found that duplicate coverage is typically identified only at claims stage — meaning consumers pay multiple premiums for protections they'll never fully use.

The loyalty tax compounds this further. Price-regulation clauses don't require individual notice, so premiums rise quietly each renewal cycle while most customers never think to question it.

Key Drivers of Unnecessary Insurance Spending

Policy Overlap: Paying Twice for the Same Protection

The most common driver of unnecessary spending is policy overlap. Many Danish consumers hold standalone insurance products that duplicate protection already embedded elsewhere:

- Travel coverage via credit card or sundhedskort: Danish consumer advisors note that travel insurance is commonly duplicated through credit card benefits or the yellow health card (det gule sundhedskort) for EU travel

- Accident coverage via employer: Workplace occupational injury insurance often covers scenarios consumers assume require private accident policies

- Roadside assistance via car manufacturer: New vehicle warranties and manufacturer programs frequently include roadside protection that duplicates standalone policies

European regulators found that insurers and distributors often don't assess overlaps at point of sale, leaving consumers to discover duplicates only at claims time — after years of unnecessary premiums.

Policy overlap is the most visible problem, but it's not the only one. Coverage that once made sense can quietly become the wrong fit as your life changes.

Life Event Misalignment: Coverage That No Longer Fits

Policies purchased at one life stage often remain unchanged through marriage, homeownership, or vehicle replacement, resulting in coverage that no longer matches your risk profile or asset value. Common mismatches include:

- Comprehensive coverage on a paid-off older vehicle whose replacement value doesn't justify the premium

- Contents insurance sums that don't reflect actual household valuables after moving or downsizing

- Family policies that haven't been updated to include newborns (who should be covered for free until age two under most Danish policies)

- Single-person accident coverage maintained after marriage when a partner's employer policy already provides protection

The result is either excess coverage you're paying for unnecessarily, or gaps in protection you don't realize exist — sometimes both at once. And even when coverage fits your life, passive renewal behavior means you're likely paying more than you should be for it.

Automatic Renewal and Passive Loyalty

Most insurance policies renew without active consumer consent or comparison. Danish insurers routinely raise premiums at renewal — testing by Forbrugerrådet Tænk found house insurance premiums increased by an average of 26% over two years, with some travel insurance increases reaching 50%.

The cost adds up fast: customers with 10+ years of seniority pay 7–8 percentage points more on average than new customers for identical risk profiles, with some firms showing 30–35 percentage point differences. Consumers who never review or switch are systematically paying a loyalty penalty — not a loyalty reward.

Over-Specification: Insuring More Than Necessary

Over-specification occurs when coverage scope exceeds realistic claim value:

- Insuring home contents for 1,500,000 DKK when actual replacement value is 500,000 DKK

- Maintaining comprehensive coverage on a vehicle worth less than the annual premium cost

- Paying for "unlimited" contents coverage that still applies strict per-item sub-limits — meaning jewelry, electronics, and valuables may be capped well below their actual value

The premium paid annually often exceeds what any realistic claim would recover, making excess coverage a net financial loss over time.

Strategies to Avoid Unnecessary Insurance Costs

Eliminating unnecessary insurance spending requires acting on three levels: the decisions made when selecting coverage, the habits used to manage policies over time, and the structural dynamics of how insurers price loyalty.

Strategies That Reduce Costs by Changing Coverage Decisions

Conduct a Pre-Purchase Overlap Check

Before purchasing any new insurance, list all existing policies and identify protections already embedded in credit card benefits, employer group plans, professional memberships, or other financial products. This single step often eliminates the need for standalone travel, accident, or legal protection policies.

Common embedded protections to check:

- Travel insurance via Mastercard, Visa, or Eurocard

- EU medical coverage via the yellow health card (det gule sundhedskort)

- Accident coverage through employer occupational insurance

- Legal aid through union membership

Match Coverage Scope to Current Asset Value

Avoid insuring assets for more than their replacement cost. For vehicles, reassess whether comprehensive or collision coverage is still justified on older models. For home contents, verify that your sum insured reflects actual valuables—not an inflated estimate from years ago.

Resist Point-of-Sale Add-Ons

Insurance distributors—banks, car dealerships, travel agencies—frequently bundle low-value or duplicate protections into products. Train yourself to identify and decline these rather than assuming they add meaningful coverage. Most add-ons duplicate existing protections or cover risks you wouldn't pay to insure separately.

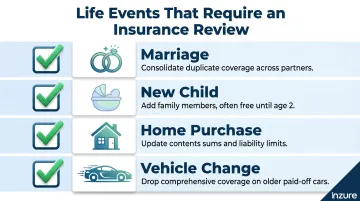

Reassess Coverage at Every Major Life Event

Marriage, divorce, a new child, a home purchase, or a vehicle change are all trigger points where current policies may be over-scoped in some areas and under-scoped in others. Build a habit of reviewing coverage rather than auto-renewing at these moments:

- Marriage: Consolidate duplicate coverage across partners

- New child: Add family members to policies (often free until age 2)

- Home purchase: Update contents sums and liability limits

- Vehicle change: Drop comprehensive coverage on older paid-off cars

Strategies That Reduce Costs by Changing How Policies Are Managed

Establish an Annual Policy Audit as Non-Negotiable

Once a year, pull together all active insurance documents, map what each policy covers, and explicitly compare overlapping protections. This process surfaces duplicates that persist for years simply because no one looks.

Create a simple audit checklist:

- What does each policy cover?

- Where do protections overlap?

- Have asset values or life circumstances changed?

- Are premiums increasing faster than inflation?

Treat Renewal Notices as Comparison Triggers

Every renewal is an opportunity to request a competing quote. Among Danish customers who negotiated their current agreement, nearly 80% obtained a lower price, and 86% of new customers who negotiated achieved savings. Switching or negotiating consistently delivers lower premiums than passive continuation, even for satisfied customers.

Use Technology to Automate What Manual Audits Miss

Platforms like Inzure can analyze your full insurance portfolio in 60 seconds, automatically detecting duplicate coverage, loyalty price inflation, and areas where you're paying above market rate. What used to take 10+ hours of manual comparison now happens in under a minute, which means annual reviews actually get done.

Monitor Claims History Before Filing Small Claims

Filing frequent minor claims triggers premium increases at renewal that often cost more over three to five years than the original claim payout. Danish consumer guidance suggests that typical deductibles around 3,000 DKK make it financially preferable to self-pay small claims rather than accept multi-year premium hikes.

Strategies That Counter How Insurers Price Loyalty

Address Insurer Pricing Behavior Directly

Loyalty is financially penalized in the Danish insurance market. Consumers who have been with the same insurer for three or more years statistically pay more than new customers for identical coverage. This isn't passive drift—it's deliberate pricing strategy.

The only reliable counter-strategy is to request competing quotes at every renewal or use an independent comparison tool. One Danish consumer saved nearly 8,000 DKK per year after 20+ years of loyalty simply by switching providers—a clear demonstration that tenure doesn't earn better pricing.

Understand That Bundling Is a Tool, Not a Rule

While multi-policy discounts can reduce individual premiums, bundling with a single insurer sometimes means accepting inferior coverage on one policy to get a discount on another. Evaluate each bundled policy on its own merits before committing. If one policy in the bundle is priced above market or provides weaker coverage, the discount on the other policy may not offset the total cost.

Recognize When Broader Setup Is the Real Cost Driver

Consumers who purchased all their insurance through the same distributor at one time (a bank, mortgage provider, or employer partnership) may have an entire portfolio priced above market without any single policy being obviously wrong. Running a full portfolio comparison across multiple carriers is the only way to surface this kind of systemic overpricing — and it's worth doing even if no individual policy looks obviously wrong.

Conclusion

Avoiding unnecessary insurance coverage isn't about taking risks or lowering protection—it's about identifying where money goes to coverage that either duplicates something else, no longer fits current circumstances, or is priced above what the open market offers.

The difference between smart and wasteful insurance spending is consistent, informed review. The Danish insurance market penalizes loyalty, hides overlaps, and auto-renews policies that no longer match your life. Tools like Inzure exist because this complexity is genuinely hard to navigate alone. What used to take 10 hours of manual policy comparison now takes 60 seconds — identifying duplicate coverage, price inflation, and gaps without the legwork.

The next renewal notice you receive is the right moment to compare, negotiate, or switch. Treat it that way.

Frequently Asked Questions

What types of insurance coverage are most commonly unnecessary or duplicated?

Travel insurance via credit cards, accident coverage via employers, and roadside assistance via car manufacturers are the most common duplicates. European regulators note these overlaps typically surface only at claims stage — meaning consumers pay for years without realizing they're covered twice for the same risk.

How do I know if I am paying too much for my insurance?

Two key signals: paying above the current market rate for your risk profile, and holding coverage that overlaps with protections embedded in other policies you already own. Danish Competition Authority data shows loyal customers with 10+ years pay 443 DKK more annually for house insurance than new customers with identical risk — tenure alone is a reliable overpayment signal.

Is it risky to reduce my insurance coverage to save money?

Not all cuts are equal. Removing duplicate or irrelevant coverage carries little risk; dropping essential protection creates real exposure. The goal is precision — eliminating a standalone travel policy your credit card already covers is smart, but cutting liability insurance to save money is not.

What is the loyalty tax in insurance and how can I avoid it?

The loyalty tax is the premium increase long-term customers pay relative to new customers for identical coverage. Danish insurers charge loyal customers 7-8 percentage points more on average, with some firms showing 30-35 point gaps. Request competing quotes at every renewal, or use an independent comparison tool to benchmark your current premium against the market.

How often should I review my insurance policies?

At minimum, once per year at renewal. Also review immediately after any major life event — a move, marriage, new child, or change in employment status. Research shows 80% of Danish customers who negotiated obtained lower prices, making an annual review one of the highest-return tasks on your calendar.

Can bundling insurance policies increase rather than decrease my total costs?

Yes. A bundle discount can be offset by one policy priced above market. If a bundled policy costs 15% more than the standalone alternative but saves you 10% on another, you're paying more overall — evaluate each policy independently against current market rates.