Introduction

You've been with the same Danish insurer for years, never missed a payment, never filed a claim. Then you finally check what a new customer pays for identical coverage — and your premium is hundreds, sometimes thousands, of kroner higher.

This isn't a billing error. It's the insurance loyalty tax: a systematic pricing gap where long-term policyholders quietly subsidize the discounts offered to new customers.

Danish regulators confirmed in 2025 that 10-year customers pay an average of 7-8 percentage points more than new customers for the same coverage. Most people never compare, never ask, and never realize they're overpaying.

This guide breaks down what the insurance loyalty tax is, how insurers build it in, how to spot it in your own policy, and exactly what to do about it.

Key Takeaways

- Long-term customers in Denmark pay DKK 443 more per year for home insurance than new customers receive for identical coverage

- Insurers use behavioral analytics and auto-renewal defaults to exploit inertia — the longer you stay, the more you overpay

- Warning signs include annual premium hikes with no claims, "loyalty discounts" below 10%, and policies older than three years

- Comparing your current premium against the real market price takes 60 seconds — tools like Inzure show exactly where you're overpaying

What Is the Insurance Loyalty Tax?

The insurance loyalty tax is the pricing gap between what long-term policyholders pay and what new customers are quoted for equivalent coverage. It's not a government levy — it's a structural feature built into how insurers price renewals.

Denmark's Competition and Consumer Authority (Konkurrence- og Forbrugerstyrelsen) confirmed in April 2025 that after 10 years, Danish customers pay significantly more:

- Husforsikring (home insurance): DKK 443 more per year

- Indboforsikring (contents insurance): DKK 240 more per year

- Bilforsikring (car insurance): DKK 425 more per year

The study analyzed 7.4 million private insurance policies across Denmark's ten largest insurers, covering approximately 90% of Danish customers. It found that 10-year customers pay 7-8 percentage points higher margins than new customers on average.

The mechanism behind this gap has a name: price walking — the practice of gradually increasing renewal premiums year-on-year, even when a customer's risk profile hasn't changed.

Price Walking vs. Risk-Based Pricing

There's an important distinction between legitimate premium changes and the loyalty tax:

- Risk-based pricing adjusts your premium when your actual risk profile changes — a new car, a filed claim, or a move to a higher-risk area

- Price walking raises your premium because the insurer knows you probably won't leave, not because your risk has increased

- The loyalty tax is the cumulative result: years of price walking that compounds silently on auto-renewal

This pattern is most visible in home and contents insurance — the policies Danes hold for the longest periods and rarely scrutinize at renewal.

Loyalty Discounts Don't Protect You

Many insurers market loyalty discounts of 5–10% as a reward for staying. In practice, these discounts are applied on top of an already-inflated base rate. The math rarely works in your favor:

| Scenario | Annual Premium |

|---|---|

| Fair market rate (new customer) | DKK 4,200 |

| Inflated renewal rate | DKK 5,000 |

| After 10% "loyalty discount" | DKK 4,500 |

You're still paying DKK 300 more than a new customer — and calling it a reward.

Forbrugerradet Tænk estimated in September 2025 that loyal customers can pay over DKK 5,000 more per year than inflation-adjusted pricing would warrant.

Why Loyal Customers Pay More: The Mechanics Behind the Penalty

Insurers don't raise your premium arbitrarily. They use pricing techniques designed to extract maximum revenue from customers least likely to switch.

Price Optimization and Behavioral Analytics

Price optimization uses customer data and behavioral algorithms to predict the maximum price increase you will tolerate before shopping around. Customers identified as unlikely to switch—because they've been with the same insurer for years, pay on time, and never request quotes—are systematically charged higher premiums.

The European Insurance and Occupational Pensions Authority (EIOPA) warned in March 2023 that "large data sets and increasingly sophisticated analytical tools such as AI enable manufacturers to deploy differential pricing practices on a large scale." EIOPA clarified that when price increases occur repeatedly for reasons unrelated to risk or cost of service, the practice violates the Insurance Distribution Directive (IDD).

Denmark's regulators flagged the same issue. KFST's 2025 analysis found that nearly all Danish insurers use annual wage-linked index adjustments to raise prices—a coordinated practice the authority described as potential "tacit price collusion."

Introductory Discounts That Disappear

Insurers offer attractive first-year discounts to acquire new customers, then gradually roll back those discounts over subsequent renewals. Insurers fund those acquisition discounts through the inflated premiums charged to loyal customers who stay put.

This creates a two-tier pricing structure:

- New customers: receive teaser rates 20–40% below standard pricing

- Renewal customers: pay full rates plus incremental loyalty surcharges year-on-year

The discount rollback is one mechanism — but older policyholders face a separate structural problem: they're often locked into pricing tiers that no longer exist.

Legacy Pricing and Closed Tiers

Many older home and contents insurance policies sit on legacy pricing structures that are no longer competitive.

The insurer has closed that pricing tier to new customers but continues charging renewals at those rates. Danish regulators confirmed that home and car insurance policies show a clear tendency for insurers to achieve higher average margins on loyal customers compared to new customers.

Case example: In February 2026, Denmark's Supreme Court ruled that Tryg Forsikring lawfully raised prices by 3.1–3.8% above index annually from 2016 to 2020 without providing prior notice to customers. The Court found these increases "not significant" under Danish contract law—this normalized silent price escalation as standard practice.

The Auto-Renewal Trap

Auto-renewal is designed to benefit the insurer, not the customer. Under Denmark's Insurance Contracts Act (Forsikringsaftaleloven), policies automatically renew unless either party gives notice—typically one month before the end of the insurance period.

Renewal notices require no action to continue. Until recently, many Danish renewal notices did not display the previous year's premium alongside the new price, making it nearly impossible to spot increases at a glance.

No regulatory requirement exists in Denmark mandating insurers to show prior-year premiums on renewal documents. The Tryg Supreme Court ruling confirmed that insurers are not legally obligated to notify customers of annual price increases below the "significant" threshold, effectively removing the wake-up call that would prompt comparison shopping.

Warning Signs You're Being Charged a Loyalty Tax

Concrete Red Flags

Check your policy for these signals:

- Annual premium increases with no change to your claims history or risk profile

- "Loyalty discount" below 10% while new-customer offers from the same insurer are 20–40% lower

- Immediate discount offered when you call to cancel—if the insurer can match a competitor instantly, you've been overpaying

- Policy in place for more than three years without a market comparison

The Benchmark Test

The clearest signal is comparing your current premium against what a new customer would pay for identical coverage, limits, and deductibles—not a rough estimate, but an exact apples-to-apples comparison.

That kind of comparison used to take hours of manual research across multiple insurers. Inzure reads your existing policy documents and returns the real market price in 60 seconds — extracting your coverage types, limits, deductibles, and exclusions, then benchmarking them against current rates from Tryg, Topdanmark, Alka, Codan, and other Danish insurers.

Self-Assessment Checklist

Answer these yes/no questions:

- Has your premium increased in the past two years without a claim or coverage change?

- Have you been with the same insurer for more than three years?

- Have you received a renewal notice without seeing last year's premium listed?

- Do you receive "loyalty discount" messaging but no actual price reduction?

- Have you not compared quotes in the past 12 months?

If you answered yes to three or more, you are likely affected by the loyalty tax.

The Psychology of Staying: Why We Keep Overpaying

Three behavioral traps keep loyal customers stuck paying too much:

Inertia and Decision Fatigue

Shopping for insurance feels like a chore. Most people avoid it. KFST's 2012 study found that approximately 10% of Danish consumers switch private household insurance providers annually—meaning 90% do not switch in any given year.

Even more telling: 43% of insurance customers consider switching but stop somewhere in the process, and 25% refrain from switching because they cannot obtain an overview of available solutions. One in six consumers who have never switched state they "prefer to spend their time on other things."

The more time customers spend studying the insurance market, the more complex it appears—a "complexity paradox" that discourages action.

The Relationship Illusion

Insurer slogans and long-term familiarity create an emotional bond that feels like a real relationship. In legal terms, it is simply a contract subject to annual renewal. Insurers exploit this illusion through:

- Image-based advertising focused on emotion, not price

- Automatic renewal defaults that require no action to stay

- Friction-heavy cancellation processes designed to discourage leaving

The Switching Myth

Many people incorrectly believe that changing insurer is complicated, risky, or creates coverage gaps. In practice, switching typically takes 15–30 minutes and carries no credit impact. KFST's research confirmed that customers who have switched report the administrative process as "easy"—but finding and comparing alternatives is hard.

The Cost of Inertia

That difficulty has a real price tag. KFST's 2025 analysis, reported in Berlingske, found that:

- 80% of customers who negotiated their price received a lower rate

- 86% of customers who switched obtained cheaper insurance

- Yet the majority of customers have not requested new quotes or switched providers within the last two years

Three groups pay disproportionately more: loyal customers who do not switch, consumers over 65 years of age, and consumers with limited education levels.

How to Stop Overpaying: A Practical Action Plan

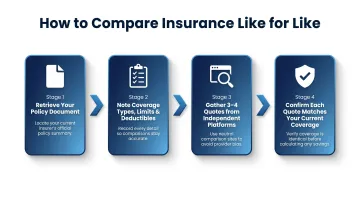

Step 1: Get the Real Market Price for Your Coverage

Start by retrieving your policy's declarations page or full document — it lists your coverage types, limits, deductibles, and active discounts. Without those specifics, any comparison is guesswork.

That's exactly what makes the next step faster than it sounds. Inzure reads and analyzes these documents automatically — even photos of policy pages work. The AI extracts your exact coverage details, including the fine print, and benchmarks them against current market rates across Danish insurers in 60 seconds.

Step 2: Compare Like for Like

Compare quotes with identical coverage types, limits, and deductibles — not just the headline premium. A cheaper quote with lower limits or a higher deductible is not a saving; it's reduced protection.

When gathering quotes:

- Get at least three to four from different insurers

- Use independent platforms — not insurer-tied comparison sites — for broader market visibility

- Confirm each quote matches your current coverage before treating it as a saving

Inzure's platform automatically flags when a competing quote involves lower coverage or a higher deductible, so the comparison stays honest.

Step 3: Negotiate Before You Switch

Contact your current insurer before switching and explicitly state you have received lower quotes for identical coverage. Many insurers will match or beat a competitor's price to retain you — but they will not offer this proactively.

If the insurer offers a real reduction, ask for it to be applied immediately, not only at next renewal. **According to KFST research, 80% of customers who negotiated received a lower rate** — a figure worth keeping in mind before you assume switching is the only option.

Step 4: Build a Review Habit

Set an annual calendar reminder 4–6 weeks before each renewal date. This gives enough time to gather quotes and negotiate without time pressure. The loyalty tax compounds over time — the longer you go without reviewing, the larger the gap grows.

Inzure offers continuous market monitoring after your initial analysis. You're notified only when something actionable appears:

- A switch that produces a meaningful price saving

- A coverage upgrade available at the same premium

- An unjustified increase from your current insurer

The monitoring is free. The 20% commission applies only if a recommended switch actually results in savings.

When Staying Is the Right Call

Switching is not always optimal. Stay if:

- You have recent or open claims

- You insure a unique high-risk property

- You are mid-policy-period facing cancellation fees

- You have a bundled multi-policy discount that would disappear

Even if the conclusion is to stay, knowing the market price gives you negotiating power.

Frequently Asked Questions

What is the insurance loyalty tax?

The insurance loyalty tax is the pricing gap where long-term customers pay more than new customers for identical coverage. It's driven by insurer pricing algorithms and gradual premium increases, not by any change in the customer's actual risk profile.

Is staying with the same car insurer worth it, or do loyal customers pay more?

In most cases, loyal insurance customers pay more. KFST found that 10-year customers pay DKK 425 more per year than new customers for the same coverage—a pattern seen across multiple insurance categories. Whether staying is worth it depends on whether your insurer's loyalty discount genuinely offsets base rate increases. A direct market comparison is the only reliable way to know.

How do insurance companies justify charging loyal customers more?

Insurers typically cite three reasons: funding new-customer discounts through acquisition cost recovery, risk profile changes, and loyalty discounts already applied. Consumer advocates note these explanations don't hold up—the loyalty gap persists even when risk profiles haven't changed, and loyalty discounts are often applied on top of inflated base rates.

How do I know if I'm paying a loyalty tax on my insurance?

If your premium rises annually without changes to your claims history or risk profile, and you haven't compared quotes in the past 12–24 months, you're likely affected. Inzure's policy analysis tool can benchmark your current premium against real-time market rates to show exactly how large the gap is.

How often should I review my insurance premiums to avoid the loyalty tax?

Review annually, ideally 4–6 weeks before each renewal. Even if you stay with the same insurer, comparing market rates strengthens your negotiating position and often leads to a lower rate. KFST confirmed that 80% of customers who negotiated received a lower premium.