In 2018, the UK Financial Conduct Authority uncovered 6 million loyal motor insurance customers paying ca. 10,4 milliarder DKK more than they would have for equivalent risk. More recently, Dutch regulators found nearly half of insurers penalizing loyal car insurance customers by ca. 1.119 DKK annually — not for driving badly, but simply for staying put.

This isn't about market forces or rising risk. It's price optimization — a data-driven practice where insurers identify customers unlikely to shop around and quietly raise their premiums year after year. The longer you stay, the more you pay.

This guide unpacks how price optimization works against you and what concrete strategies you can use to reverse it.

Key Takeaways

- Insurance costs rise not just from risk — insurers use price optimization to charge loyal customers more based on their likelihood to stay

- Key cost drivers include coverage level, policy overlaps, loyalty tenure, and skipping regular market comparisons

- Regularly comparing policies delivers the highest impact — documented savings reach thousands of kroner per year for those who switch

- You can also reduce premiums by adjusting deductibles, eliminating unnecessary coverage, and actively claiming available discounts

- Insurance optimization is ongoing: automated monitoring platforms remove the manual effort and prevent future overpayment

What Is Auto Insurance Price Optimization — And Why It Costs You More

Price optimization is a data-driven insurer practice that uses behavioral and consumer data — purchase patterns, lifestyle signals, how long you've stayed with a provider — to identify customers unlikely to shop around. Insurers then raise premiums based on this price tolerance, not actuarial risk.

It's Not Risk-Based Pricing

Unlike rate changes driven by accidents or driving violations, price optimization penalizes loyalty and inertia. Two drivers with identical risk profiles can pay materially different premiums simply because one compares rates annually and the other doesn't.

The National Association of Insurance Commissioners (NAIC) defines it as "the supplementation of traditional actuarial loss cost models to include quantitative customer demand models for use in determining customer prices." A 2013 survey cited in the white paper found 45% of large insurance companies used some form of price optimization.

How the Mechanism Works

Insurers purchase or compile consumer data and run it through internal scoring models that assign a "price elasticity index" — a score estimating how sensitive each customer is to price increases. They then set premiums based on this tolerance rather than purely on risk.

Connecticut regulators describe it as "an insurer's use of sophisticated data mining tools and modeling techniques during the ratemaking process to vary rates based on factors other than a person's risk of loss. The goal is to charge an insured person the highest amount he or she will tolerate before shopping for alternative coverage."

The "Loyalty Discount" Masking Effect

Insurers sometimes apply small loyalty discounts while simultaneously raising base rates — so the net premium goes up even as you feel rewarded. A common example: a 10% discount applied after a 25% rate increase. You see "loyal customer discount" on your renewal notice, but your total cost is still 15% higher than last year.

The Regulatory Landscape

That loyalty trap is exactly what regulators have moved to stop. Price optimization has been banned or restricted across multiple jurisdictions because it prices based on consumer behavior rather than actuarial risk — a distinction regulators increasingly view as discriminatory.

- United States: Twelve states plus Washington D.C. have banned the practice, including California, Florida, Maryland, Ohio, and Pennsylvania. Colorado became the 15th jurisdiction to act in 2015.

- European Union: EIOPA's 2023 supervisory statement targets "price walking" — repeated renewal increases unrelated to risk. This practice is incompatible with the Insurance Distribution Directive (IDD), which requires insurers to act in customers' best interests.

- Denmark: Danish insurers are bound by IDD fair-treatment obligations as EU members. The Danish Insurance Contracts Act also allows policies to be cancelled with 30 days' notice — meaning you're never locked into an unfair renewal.

How Auto Insurance Costs Build Up Over Time

Insurance overpayment rarely arrives as one obvious spike. It builds gradually — small annual premium increases that go unchallenged because most people assume the hike reflects genuine risk changes or broader market conditions.

The Compounding Effect

Each renewal year adds a small increment. Without comparison shopping, you can drift significantly above market rate over a 3-5 year period without noticing.

The pattern is well-documented across European markets. UK data from 2024 found that 47% of policyholders renewed automatically without comparing prices — collectively paying ca. 4,87 milliarder DKK more than necessary that year. The same passive renewal behavior drives overpayment in the Danish market.

In the Netherlands, the Authority for the Financial Markets found that loyal customers staying 9+ years generated profit margins over 10 percentage points higher than new customers with identical risk profiles. Insurers aren't rewarding loyalty — they're pricing on it.

Key patterns that drive cumulative overpayment:

- Automatic renewals accepted without checking the current market rate

- Loyalty pricing — longer tenure often means higher margins extracted from you

- Small annual increases that individually seem minor but compound significantly over 3-5 years

- Assumed risk-based pricing — most customers presume increases are justified when they often aren't

The Hidden Nature of These Costs

Unlike a one-time expense, ongoing premium overpayment stays invisible until you compare market rates directly. Once you do, the gap is usually concrete: Inzure users have identified savings ranging from 2,800 kr to 48,000 kr per year — money paid year after year to the same insurer for no additional benefit.

Key Factors That Drive Your Auto Insurance Premium

Auto insurance premiums are shaped by two groups of factors: risk-based (driving record, age, vehicle type, location, annual mileage) and behavioral (loyalty tenure, payment method, whether you've recently shopped).

Most drivers focus on the first group — the behavioral factors are where insurers quietly gain the upper hand.

Standard Risk-Based Factors in Denmark

- Car model and value: Higher-value vehicles and models with expensive parts cost more to insure

- Driver age: Young drivers under 25 pay 50-100% more; premiums decrease from age 25 to around 55

- Postcode/location: Urban areas like Copenhagen typically have higher rates due to theft and accident frequency

- Estimated annual mileage: Lower mileage often qualifies for reduced premiums

- Claims history (bonus-malus step): Denmark's no-claims bonus system offers up to 65-70% discounts at the highest step

- Chosen deductible (selvrisiko): Higher deductibles reduce premiums

Inertia as a Cost Driver

Staying with the same insurer for years without comparing rates is increasingly treated by insurers as a signal that you will tolerate higher prices. The longer you stay without shopping around, the more you pay for that loyalty.

The NAIC white paper cites a Deloitte survey finding that 58% of auto insurance consumers rarely or never shop for coverage. Only 18% shop every year. Insurers price with that knowledge built in.

Coverage Mismatches

Pricing inefficiency isn't always about paying too much — sometimes it's paying for the wrong things. Two common mismatches:

- Over-coverage: Paying for protections you don't need, such as duplicate benefits already covered elsewhere

- Under-coverage: Gaps in protection you assume you have but don't — often only discovered at claims time

Both are hard to catch without comparing your actual situation against what your policy states.

Cost-Reduction Strategies: Taking Back Control of Your Premium

The most effective strategies vary depending on which dimension of cost you want to address — the decisions made at policy selection, the habits maintained during the policy term, or the broader context in which coverage sits.

Strategies That Reduce Costs by Changing Decisions

Compare rates at every renewal, not just when something changes

Shopping around at each renewal period — ideally 4-6 weeks before the policy renews — is the single highest-impact action. It signals to insurers you are price-sensitive and exposes you to competitive offers.

Danish car insurance prices can vary by 30-50% between providers for equivalent coverage. In the UK, the FCA's pricing reforms delivered ca. 13,9 milliarder DKK in consumer savings over a 10-year horizon in the motor market by effectively banning renewal premiums higher than new-customer prices.

Adjust your deductible deliberately

Raising your deductible shifts more out-of-pocket risk to you in exchange for a lower premium. This can be a sound trade-off if you have an emergency fund.

The Insurance Information Institute states that increasing your deductible from 1.400 DKK to 3.500 DKK reduces collision and comprehensive costs by 15-30%. Going to a 7.000 DKK deductible can save 40% or more.

In Denmark, the standard selvrisiko is 3,884 kr, adjustable from approximately 2,500 kr to 10,000 kr. Raising it lowers your annual premium proportionally.

Right-size your coverage to your actual vehicle value

Maintaining comprehensive and collision coverage on an older or lower-value vehicle may result in premium costs that approach or exceed the vehicle's insurable value.

If your car is worth 30,000 kr and full kasko costs 8,000 kr annually, you're paying more than 25% of the vehicle's value each year — liability-only coverage is often the smarter financial call.

Choose your next vehicle with insurance cost in mind

Vehicle make, model, repair cost, safety rating, and theft likelihood all factor into premium calculations. Reviewing insurance cost estimates before purchasing a vehicle can cut your long-term insurance bill meaningfully.

Some models cost twice as much to insure as others in the same price range due to parts availability, theft rates, or safety features.

Strategies That Reduce Costs by Improving How You Manage Coverage

Protect and improve your credit profile

In most markets, insurers use a credit-based insurance score as part of their risk model, with the rationale that financial responsibility correlates with lower claim rates. While credit-based insurance scoring is less prevalent in Europe than in the United States, maintaining or improving credit has a direct premium impact over time where it is used.

Under GDPR Article 22, if an insurer uses automated credit-based scoring, they must provide the right to human intervention and to contest the decision.

Maintain a clean driving record

Avoiding violations, at-fault accidents, and claims keeps you in the lowest risk tier and prevents surcharges.

Denmark's bonus-malus system offers substantial discounts:

- Step 0 (new driver): 0% discount

- Step 1 (1 claim-free year): approximately 15% discount

- Step 2 (2 years): approximately 30% discount

- Step 3 (3 years): approximately 40% discount

- Step 4 (4 years): approximately 50% discount

- Step 7-8 (maximum): approximately 65-70% discount

An at-fault claim drops you 2-3 steps. Maintaining your position at step 7-8 is the single largest premium lever for Danish drivers.

Audit your active discounts at every renewal

Many available discounts go unclaimed simply because policyholders don't ask. Common Danish auto insurance discounts include:

- Union or professional group memberships (IDA, Djøf, Akademikerne)

- Multi-policy bundling (home + auto)

- Higher deductible selection

- Annual payment instead of monthly installments

- Restricting the policy to named drivers

- Lower annual mileage declaration (under 15,000 km)

- No-claims history transfers between Danish insurers

Structural Moves That Cut Costs at the Policy Level

Beyond driving habits and coverage choices, how you structure your policies — and how actively you track market pricing — can have just as large an impact.

Bundle policies to access multi-policy discounts

Holding home, contents, or other personal insurance with the same provider typically unlocks multi-policy discounts that reduce your total premium cost across the board.

Explore usage-based or pay-per-mile insurance if you drive infrequently

Telematics-based insurance programs price coverage based on actual driving behavior and mileage rather than statistical averages, which can cut premiums substantially for low-mileage or consistently safe drivers.

Consumer Reports found median annual savings across all US telematics users were 840 DKK, with maximum discounts ranging from 15% to 40% depending on insurer. Policies with younger drivers saw median savings of 1.715 DKK.

The European insurance telematics market is projected to reach 17.6 million policies by 2028, with growing availability in Denmark.

Use an independent platform to monitor market rates continuously — not just once

The most durable way to avoid price optimization is to close the information gap. When insurers know you're not comparing, they have pricing power.

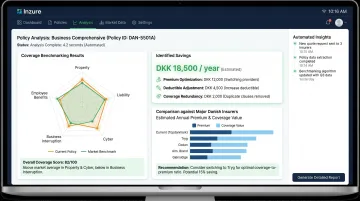

Inzure, an AI-powered independent platform, analyzes your existing policies across the Danish market and flags when you're paying above the going rate — converting one-time comparison shopping into ongoing protection.

The platform completes policy analysis in 60 seconds, benchmarking your coverage and pricing against major Danish insurers including Tryg, Topdanmark, Alka, Codan, and others. It's free to use; Inzure charges only 20% of savings if you choose to switch. Alerts fire only when something actionable comes up (a better-priced deal or an unwarranted increase), so you never have to remember to compare manually.

Conclusion

Auto insurance overpayment is rarely caused by unavoidable risk. More often, it comes down to three things: **not shopping around, not knowing what comparable coverage costs, and insurer pricing practices that rely on customer inaction**.

Reducing what you pay takes two things: a clear look at your current coverage, and a habit of comparing as your circumstances change. Continuous monitoring tools make that second part practical — turning what used to be hours of research into something that runs in the background.

Most people who switch after a proper comparison find savings they didn't expect. The gap between your current premium and the market rate is real — it just requires looking.

Frequently Asked Questions

What is price optimization in insurance?

Price optimization is an insurer practice of using behavioral and consumer data to identify customers who are unlikely to shop around, then charging them higher premiums based on price tolerance rather than actual risk. In short, staying loyal often costs you more — not less.

How can I reduce my insurance premiums?

Compare rates at every renewal, raise deductibles where your emergency fund can absorb the risk, and claim all available discounts — no-claims bonuses, multi-policy bundles, and loyalty alternatives offered by competing insurers. Running these steps together consistently delivers the largest reductions.

Is price optimization in insurance legal?

In Denmark and across the EU, EIOPA's 2023 supervisory statement prohibits "price walking" under the Insurance Distribution Directive — meaning insurers cannot systematically charge loyal customers more than new customers for identical coverage. Enforcement varies by carrier, which is why independent comparison remains the most reliable consumer protection.

How do I know if I'm being price optimized?

The clearest signal is a premium that keeps rising at renewal despite no change in your risk profile — no new claims, no violations, no change in vehicle or mileage. Comparing your current premium against market quotes for identical coverage is the most direct way to detect it.

How long does it take to find out if I'm overpaying on my insurance?

An AI-powered policy analysis typically returns results in under 60 seconds. You upload your current policy documents, and the platform identifies overpayments, coverage gaps, and market alternatives — no manual comparison spreadsheets required.

How often should I compare insurance rates?

Compare at every renewal — typically every 6 or 12 months — and after any significant life change: moving, adding a family member, or acquiring new assets. Automated monitoring handles this in the background, flagging better deals without you having to remember to check.