Insurance premiums don't become expensive overnight. They grow through passive renewal habits, structural industry pricing practices, and decisions consumers don't realize they're making. The average Danish household now spends nearly 16,000 kr annually on non-life insurance, up from 3.1% of total household consumption in 1995 to 4.4% in 2022. This guide shows you how to stop overpaying — not by cutting coverage, but by paying the right price for the protection you actually need.

Key Takeaways

- Premiums build gradually through auto-renewals and loyalty penalties, not sudden spikes

- Key cost drivers: deductible levels, coverage scope, risk profile, and years of loyalty without renegotiating

- The biggest savings typically come from comparing market rates at renewal and auditing your coverage for gaps or overlap

- Raising your deductible strategically can also reduce premiums — if you have the cash buffer to absorb a higher out-of-pocket cost

- Simply canceling coverage creates risk — the goal is the right coverage at a fair price

- AI-powered policy analysis can reveal savings that manual price checks routinely miss

How Insurance Premiums Typically Build Up Over Time

Insurance costs rarely spike suddenly. They accumulate through a series of small, nearly invisible increases that compound over years.

Annual renewal increases are the primary driver. Since the mid-1990s, Danish non-life insurance prices have risen 10% more than the EU average — house and contents insurance alone has increased 45% more than the EU average over the same period.

The Danish Competition Council identified an industry-wide practice of automatically increasing premiums in line with private-sector wage development — often 3-5% per year — without specific prior notification to policyholders.

Most consumers accept the renewal quote without comparing it to current market rates — never seeing the gap between what they pay and what a new customer would pay for identical coverage. Forbrugerradet Taenk's August 2025 testing found that total prices for bundled home, contents, and accident insurance rose by up to 37% between 2023 and 2025 for certain customer profiles.

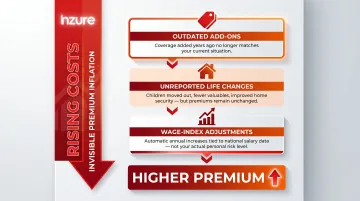

The Invisible Nature of Cost Creep

Three specific mechanisms quietly push premiums higher without triggering any notification:

- Add-ons from policies 5+ years ago that no longer match your situation

- Life changes never reported — children moving out, fewer valuables, better home security

- Automatic wage-index adjustments that raise your premium based on salary data, not your actual risk

The Danish Competition Council characterizes automatic annual increases as a form of "tacit price coordination" that weakens competition. Without external benchmarking, there's no practical way to tell whether your annual increase reflects genuine risk changes — or simply a loyalty penalty built into the system.

Key Cost Drivers for Insurance Premiums

Deductible Structure

Your deductible is one of the most direct levers affecting premium cost. The lower your deductible, the higher the insurer's exposure, and the higher your premium. According to the Insurance Information Institute, increasing a homeowner's deductible from DKK 500 to DKK 1,000 can reduce premiums by roughly 10-25%, depending on the insurer.

Most consumers never revisit the deductible they chose at sign-up — even when their finances have improved and a higher out-of-pocket threshold would cost them less each year.

Coverage Scope and Policy Limits

Comprehensive coverage on an older, depreciated asset may cost more than the asset is worth in potential claims. Common inefficiencies include:

- Overlapping liability coverage across home and family plans

- Duplicate travel insurance provided by credit cards or the public health card for EU travel

- Outdated sum-insured values that no longer reflect actual belongings

Forbrugerradet Taenk advises reviewing coverage whenever major life changes occur — children moving out, purchasing fewer valuables, improved home security — to avoid paying for protection you no longer need.

Risk Profile Factors

Your driving record, claims history, and property characteristics compound over time. Key factors insurers weight heavily include:

- Claims history: A single claim can affect premiums for 3-7 years in most European markets

- Property characteristics: Security upgrades (alarms, locks) can lower your risk score

- Credit and payment history: Relevant in some Danish carrier assessments

Identical risk profiles routinely receive quotes that differ by hundreds of kroner across carriers — which is exactly why comparing matters.

The Loyalty Tax

The Danish Competition Council's 2025 analysis confirmed that 10-year customers pay 7-8 percentage points more than new customers with the same risk profile. Staying loyal doesn't earn a discount — it earns a higher margin for the insurer.

The Council's findings go further: customers aged 65+, those with education only to 9th grade, and those with low financial literacy pay disproportionately higher margins. The loyalty penalty isn't just a market inefficiency — it falls hardest on those least equipped to push back.

Cost-Reduction Strategies for Insurance Premiums

Not every savings opportunity works the same way — or at the same time. These seven strategies are grouped by when you can act on them, so you know exactly where to focus first.

The three phases are:

- Before your policy is structured — decisions about deductibles, bundling, and coverage scope that affect your starting premium

- While your policy is active — adjustments you can make mid-term, such as removing duplicate coverage or updating your risk profile

- In relation to the broader market — comparing your current deal against what other carriers actually charge for the same coverage

Strategies That Reduce Costs by Changing Decisions

Strategy 1 — Increase Your Deductible Deliberately

Raising your deductible shifts a portion of financial risk from the insurer to you in exchange for lower recurring premiums.

How it works: Research the premium difference between your current deductible and higher options. For example, moving from a low deductible (500 kr) to a mid-range one (1,500 kr) can reduce your annual premium by 10-25% — potentially 800-2,000 kr per year for a typical contents policy.

When this makes sense: Only increase your deductible if you can comfortably cover the higher out-of-pocket cost in the event of a claim. Consider your emergency fund, typical claim sizes in your policy category, and your personal risk tolerance.

Implementation: Contact your current insurer to request a quote with a higher deductible, then compare that quote against market rates for equivalent coverage with the new deductible level.

Strategy 2 — Right-Size Your Coverage by Auditing What You Actually Need

Many policyholders carry coverage they no longer need:

- Comprehensive/collision on depreciated vehicles where the coverage costs more than potential payouts

- Personal accident coverage duplicated across work-provided policies and personal policies

- Coverage limits set years ago and never reviewed despite life changes

What to audit:

- Contents insurance sum-insured — does it still match your actual belongings value?

- Liability limits — are they appropriate for your current wealth and risk exposure?

- Family member coverage — are children who moved out still listed?

- Travel insurance — do you already have coverage through credit cards or employer benefits?

Dropping or adjusting unnecessary coverage can reduce premiums without creating real-world protection gaps.

Strategy 3 — Make Smarter Policy and Payment Decisions Upfront

Insurers lock in several cost factors at policy initiation, not at renewal:

Pay annually instead of monthly: Tryg and FDM Forsikring both charge a 3% surcharge on the annual premium for monthly payment. For a 10,000 kr annual policy, that's 300 kr extra simply for spreading payments across 12 months. Monthly payment also incurs higher collection fees: Tryg charges 38.50 kr per invoice for physical payment vs. 9.50 kr for direct debit.

Opt into paperless billing and autopay discounts: Many insurers offer small but meaningful discounts (typically 2-5%) for electronic billing and automatic payment enrollment.

Choose lower-risk vehicle models: When purchasing a new car, consider insurance risk ratings. Insurers price based on theft rates, repair costs, and safety features. Choosing a model with lower insurance ratings can save hundreds to thousands of kroner annually.

Strategies That Reduce Costs by Changing How Your Insurance Is Managed

Strategy 4 — Protect and Actively Manage Your Risk Profile

A clean claims history directly reduces premiums over a 3-5 year window.

Three habits protect your risk profile over time:

- Avoid small claims — Pay minor damages out of pocket when costs are close to your deductible. A single claim can raise your premium for 3+ years, wiping out whatever you recovered.

- Document your home security setup — Smoke detectors, burglar alarms, and security systems can qualify you for discounts with many Danish insurers. Keep records and ask your insurer directly.

- Review your policy annually — Risk profiles shift. A home renovation, a new security system, or fewer years without claims all create grounds to renegotiate.

Strategy 5 — Stack Available Discounts and Bundle Strategically

Managing your risk profile keeps your base rate low. The next step is making sure you're actively claiming every discount you're entitled to — most policyholders aren't.

Common discounts Danish policyholders overlook:

- Multi-policy bundling (home + contents under one insurer)

- Low-mileage discounts on vehicle coverage

- Loyalty discounts that require active enrollment — they're rarely applied automatically

- Home security discounts for documented alarm systems

Forbrugerrådet Tænk's August 2025 testing puts this in sharp relief: 4 of the 6 cheapest insurers offered 0% bundling discount — their low prices came from competitive base rates, not promotional deals. In 8 out of 15 cases, the same insurer ranked among the cheapest for one policy type and among the most expensive for another.

What this means practically: the total combined premium is what matters, not the discount percentage. Bundling only saves money if the combined price beats buying separately from different insurers. Always compare the final number.

Strategies That Reduce Costs by Changing the Context Around Your Insurance

Strategy 6 — Shop the Market Actively, Especially at Renewal

Premiums vary dramatically across insurers for identical coverage. Taenk's 2025 testing found a 5,700 kr difference (nearly 40%) between the cheapest and most expensive insurer for equivalent bundled coverage. In extreme cases, the most expensive charged more than double the cheapest.

In 2024, 1,507,033 private insurance policies were transferred between companies in Denmark — a record. Roughly 15% of insurance customers switch annually, compared to only 4% for banking. Yet 85% still stay with their insurer each year, many quietly paying the loyalty penalty.

Case study: A customer loyal to Tryg for 20 years saw his house insurance rise from 4,116 kr to 6,180 kr — a 50% increase. He switched providers and saved 8,000 kr per year.

At renewal, follow these four steps:

- Gather at least 3 quotes before deciding

- Compare equivalent coverage terms, not just price

- Check insurer financial stability and claims reputation

- Confirm the new policy start date before canceling the old one to avoid gaps

Forbrugerradet Taenk recommends switching every 3-5 years to avoid overpaying.

Strategy 7 — Detect Loyalty Penalties and Duplicate Coverage Using Independent Analysis

This is the most overlooked strategy — you cannot spot overcharges or duplicate coverage without benchmarking your policy against what's actually on the market.

The gap most consumers miss: After 10 years with the same insurer, you're likely paying approximately 2,400 kr more per year compared to a new customer for identical coverage — but you have no way of knowing this unless you benchmark your policy.

Independent analysis typically surfaces four things most consumers never check:

- Loyalty surcharges quantified to the exact krone amount

- Duplicate coverage — travel insurance through credit cards, liability overlap across policies

- Coverage gaps — missing legal aid, unregistered family members

- Unjustified price increases that exceed market norms

Inzure's analysis platform handles this in 60 seconds — upload your policy documents and receive a detailed report showing loyalty penalties, overlapping coverage, and the real market price for equivalent protection.

Early users have uncovered savings ranging from 2,800 kr to 48,000 kr per year. Once you have the report, the decision is yours: renegotiate, switch, or stay — with full visibility into what your current terms actually cost you.

Conclusion

Most overpayment is invisible until you go looking for it. The cost sits inside your policy structure, your risk profile, or a market you've never benchmarked yourself against — and it stays there as long as you leave it alone.

The most effective approach is continuous, not one-time: review your policy annually, benchmark against the market at every renewal, and use independent tools that work for you, not for the insurer. Platforms like Inzure analyze your existing policies against the Danish market in 60 seconds — identifying gaps, overlaps, and pricing you can actually challenge.

With record switching activity (1.5 million policies in 2024) and regulatory scrutiny increasing (Denmark's first market investigation into insurance pricing), the Danish insurance market is becoming more transparent. Take advantage of this momentum by acting on the seven strategies above.

Frequently Asked Questions

What is insurance premium reduction?

Insurance premium reduction refers to lowering the recurring cost of a policy through adjustments to deductibles, coverage scope, risk profile, or switching to a more competitively priced insurer. It's distinct from canceling coverage — the goal is paying the right price for adequate protection.

What is the best way to reduce your insurance premium?

The single most impactful action for most consumers is actively comparing market rates at renewal rather than auto-renewing, combined with auditing existing coverage for overlaps or unnecessary add-ons. Danish consumer watchdog Taenk's testing shows price gaps up to 5,700 kr (40%) between insurers for identical coverage.

Can I negotiate a lower insurance premium?

Premiums aren't directly negotiable like contract prices, but you can influence them effectively. Present competing quotes, request a loyalty review, ask which discounts you qualify for, and demonstrate an improved risk profile — such as a clean claims history or new security systems.

How do past claims affect my insurance premium?

A claims history raises premiums, but the impact varies between insurers — some weigh past claims less heavily than others. Focus on rebuilding a clean record over 3-5 years and compare across multiple insurers to find the best rate for your situation.

What's the best way to switch insurance providers?

Gather quotes with equivalent coverage terms, confirm the new policy's start date before canceling the old one, and check the new insurer's ratings. Under Danish law, you have a 14-day cooling-off period to withdraw from a newly signed policy.

Is 300 kr a month for insurance bad?

Whether a premium is reasonable depends on the market, coverage level, and your risk profile. The more important question is whether the price reflects the real market rate for your situation, which you can only determine by comparing current quotes from at least 3 insurers.