Introduction

Most Danish households pay more for insurance than they should — often without knowing it. Insurers routinely raise premiums at renewal with minimal explanation, and most people never compare what they're actually paying against what the market offers. The gap between what you pay and what you could pay is frequently larger than expected.

Insurance costs rarely jump all at once. They creep up through automatic renewals, loyalty penalties, and insurer-driven price adjustments that go unquestioned. By the time most people notice, they're overpaying — and often carrying coverage gaps at the same time.

This article covers five practical strategies to lower your insurance premiums without cutting the coverage you actually need. Applied together, these methods can reduce what you pay by 20–46% per year — a range Inzure has documented across thousands of Danish consumer policies.

Key Takeaways

- Auto-renewals quietly raise your premiums each year — most Danish households overpay without ever noticing

- Raising your deductible by a modest amount can cut your annual premium by 10–20% with limited financial risk

- Bundling home, accident, and liability coverage under one carrier almost always costs less than separate policies

- Duplicate coverages are common: many people pay twice for the same protection across multiple policies

- Switching carriers — or simply threatening to — is often enough to unlock better rates on existing coverage

How Business Insurance Costs Accumulate Over Time

How Insurance Costs Accumulate Over Time

Business insurance costs rarely appear as a sudden shock. They build incrementally across renewal cycles, policy add-ons, and insurer adjustments that policyholders rarely review in detail.

The pattern typically looks like this:

- Year one: A competitive quote gets you in the door

- Year two: Renewal comes in 3–5% higher

- Year three: A new coverage endorsement gets added

- Year four: Premiums adjust upward to reflect updated asset or household values

- Year five: You're paying 20–30% more — without ever consciously choosing to expand coverage

The loyalty penalty is well-documented. The UK Financial Conduct Authority found that loyal home insurance customers paid approximately 83% more than new customers for identical coverage after five years. Similar patterns exist across European consumer insurance markets: insurers reserve their sharpest pricing for new customers, not loyal ones.

Most cost accumulation remains invisible by design:

- Policies auto-renew without requiring active confirmation

- Policy language is deliberately complex and difficult to parse

- Few policyholders benchmark their premiums against actual market rates

- Brokers may prioritize ease of renewal over cost optimization

Passive renewal is the default for most people — and insurers count on it.

Key Factors That Drive Up Business Insurance Premiums

⚠️ Section requires full rewrite. All content in this section covers US commercial/B2B insurance (general liability, workers' comp, commercial property) with USD pricing and US-market sources (Insureon, Marsh, CIAB). Inzure's scope is exclusively Danish B2C personal insurance (home, travel, accident, liability). Business/Commercial Insurance is explicitly listed as out-of-scope. A surgical fix is not possible — the factual content, sources, currency, and audience framing all need to be replaced. See revision_summary for recommended rewrite direction.

5 Ways to Lower Your Business Insurance Premiums

Premium reduction requires identifying where excess cost originates. Blunt coverage cuts create new financial risks, while targeted adjustments based on actual cost drivers generate sustainable savings.

Way 1: Raise Your Deductible Strategically

Increasing your deductible — the amount you pay out-of-pocket before insurance activates — directly reduces premiums because it decreases the insurer's exposure.

Moving from a $500 to $1,000 deductible saves 10-20% on most business insurance policies, including general liability, BOPs, commercial property, and errors & omissions coverage. Jumping from $1,000 to $2,500 delivers even greater savings.

Before raising your deductible, weigh these factors:

- Only raise deductibles to levels you can cover from operating cash or reserves

- Evaluate whether filing small claims is worthwhile — if repair costs barely exceed your deductible, paying out-of-pocket preserves your claims history

- Higher deductibles work best for businesses with predictable cash flow and low claims frequency

- Document your decision at renewal to ensure the change is properly applied

About two-thirds of small businesses choose to pay deductibles on general liability policies, with average deductibles between $500-$1,000. For professional liability, deductibles typically range from $500 to $10,000 depending on risk profile.

When this strategy fails: If your business operates on thin margins with limited cash reserves, a $5,000 deductible that saves $800 annually creates more risk than value.

Way 2: Bundle Your Business Coverages Into a Single Policy

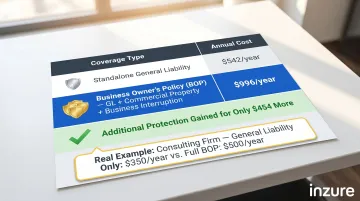

Business Owner's Policies (BOPs) consolidate multiple coverage types — property insurance, business interruption, and general liability — into a single package that costs less than purchasing each policy separately.

The numbers make the case:

| Coverage Type | Average Annual Cost |

|---|---|

| Standalone General Liability | $542 |

| BOP (GL + Commercial Property + Business Interruption) | $996 |

| Added property/BI protection for incremental cost | $454 |

For consulting businesses specifically, standalone GL costs $350/year while a BOP with added property coverage costs just $500/year — adding meaningful protection for only $150 annually.

BOPs are available to businesses that meet these criteria:

- Typically available for businesses with fewer than 100 employees

- Annual revenue generally under $5 million

- Low-to-moderate risk operations (office-based, retail, service businesses)

- Standard coverage needs without highly specialized risks

What BOPs don't cover: Workers' compensation, professional liability (E&O), commercial auto, health insurance, or disability coverage must be purchased separately.

Larger businesses or those with complex risk profiles may need a Commercial Package Policy (CPP) instead. CPPs cost more than BOPs but can include property, GL, inland marine, crime coverage, and equipment breakdown protection tailored to specific operational needs.

Bundling also reduces administrative complexity, eliminates potential coverage gaps between separate policies, and simplifies renewals.

Way 3: Build and Enforce a Workplace Safety Program

A documented, actively enforced safety program signals lower risk to insurers, which directly reduces workers' compensation and general liability premiums.

OSHA research cites a Cal/OSHA study showing a 9.4% drop in injury claims and 26% average savings on workers' compensation costs in the four years following a workplace safety inspection, compared to similar uninspected workplaces. Inspected firms saved an estimated $355,000 in injury claims and compensation over that period.

Informal safety culture doesn't qualify — insurers respond to documentation and demonstrable enforcement. OSHA's seven core elements provide the framework:

- Management leadership — commitment, resources, and accountability from ownership

- Worker participation — engaging employees in hazard identification

- Hazard identification and assessment — proactive identification before incidents occur

- Hazard prevention and control — implementing controls and protective measures

- Education and training — ensuring all workers understand safe procedures

- Program evaluation and improvement — monitoring outcomes and adjusting

- Communication and coordination — coordinating safety across contractors and shared worksites

Workers' compensation insurers use experience rating systems that directly tie your safety record to pricing. Like a safe-driving discount for auto insurance, employers with good safety records save on premiums. Poor loss experience triggers debit modification factors that increase costs.

To act on this immediately:

- Request a formal risk control consultation from your insurer — many offer these at no charge

- Ask specifically about premium reduction programs tied to safety improvements

- Document all training sessions, incident reports, and safety audits

- Review your experience modification rate annually and challenge it if inaccurate

OSHA data also shows a direct link between safety and survival: businesses that failed within two years had an average injury rate of 9.71, while those surviving more than five years averaged 3.89 in their first year.

Way 4: Audit Your Coverage for Gaps and Overlaps

Over time, businesses accumulate redundant coverages — either because policies were added without removing outdated ones, or because coverage from one policy duplicates what another provides. These overlaps inflate premiums without adding protection.

Willis Towers Watson research identifies cyber, crime, and professional indemnity policies as primary overlap areas. Social engineering losses, for example, may trigger both crime and cyber policies simultaneously — redundant coverage that raises costs without adding benefit.

Genuine gaps carry the opposite risk. The Hiscox report found:

- 25% of businesses lack professional liability when required

- Only 49% carry property insurance

- 35% lack cyber insurance despite 75% having heightened cyber exposure

- 22% lack general liability protection despite operating in environments where it's necessary

Two concrete examples:

- Overlap: A manufacturer paying for equipment breakdown coverage under both a commercial property policy and a separate inland marine policy

- Gap: A consulting firm storing client data in the cloud with no cyber liability coverage — exposed to breach notification costs, forensic investigation, and regulatory fines

Audit your coverage at these trigger points:

- At every renewal cycle (annually minimum)

- After significant business changes: new hires, new locations, new service offerings

- Following revenue increases or decreases of 20% or more

- When adding new asset categories (vehicles, equipment, real estate)

- After regulatory changes in your industry

Request declarations pages for all active policies and review them side-by-side. Look specifically for:

- Duplicate per-occurrence limits across policies

- Overlapping coverage triggers (e.g., both a BOP and standalone GL)

- Outdated coverage for assets no longer owned

- Exclusions that create gaps when multiple policies are involved

- Coverage limits that no longer match current asset values or revenue

WTW recommends qualitative scenario testing: "How would your current insurance policies respond to your key risk scenarios?" Use comprehensive claims data to understand how insurance has responded to similar situations in your industry.

Way 5: Compare the Market and Renegotiate Regularly

Most businesses never shop their insurance after the initial purchase, even though the market changes annually. Staying with one insurer without benchmarking means accepting whatever rate they choose to charge.

Current market conditions favor action: The CIAB Q4 2025 survey confirms the softest commercial insurance market since 2017, with premiums increasing just 0.2% on average. Global commercial rates declined 5% in Q1 2026, and property rates fell 9%. The survey notes "abundant capacity, enabled by a wave of carrier and MGA entrants to the market."

These conditions create unusually favorable leverage for renegotiation or switching.

A Nationwide survey found that 63% of small business owners and 81% of mid-market owners work with a single insurance agent — rarely seeking outside quotes. Compounding this, 74% of business owners misunderstand general liability coverage, making meaningful comparison difficult without expertise.

The Insurance Information Institute puts shopping around first on its cost-reduction list: "Prices vary from company to company, so it pays to shop around. Get the names of companies or brokers who specialize in your type of business."

How to do it effectively:

- Request quotes from at least three carriers or brokers 60-90 days before renewal

- Provide identical coverage specifications to enable apples-to-apples comparison

- Review not just premium but also coverage terms, exclusions, and deductibles

- Use competing quotes as leverage to renegotiate with your current carrier

- Document any service issues or claims handling problems that justify switching

Switch when:

- You're offered equivalent coverage at 15%+ lower premium

- A new carrier provides broader coverage at similar cost

- Your current insurer has demonstrated poor claims handling

- You've been with the same carrier 5+ years without shopping

Stay when:

- Your current carrier knows your business and claims history

- Switching would restart waiting periods for certain coverages

- The premium difference is minimal (under 10%) and relationship value is high

The current soft market window is the right time to act. Request competing quotes before your next renewal — the leverage available now may not exist in 12-18 months.

Conclusion

Reducing insurance premiums isn't about cutting coverage — it's about understanding where costs originate and addressing the specific decisions, behaviors, and market dynamics that inflate them.

The five strategies outlined here work best in combination. Each one reinforces the others:

- Auditing your policies first reveals gaps and duplicates — and tells you exactly how much deductible risk you can actually absorb

- Bundling home, travel, and accident coverage reduces total cost but needs periodic review to catch missing protections

- Adjusting deductibles generates immediate savings, but only if your audit confirms you have the reserves to cover them

- Shopping your improved risk profile across carriers — Tryg, Alka, Topdanmark, and others — captures savings your current insurer has no incentive to offer you

The highest-impact approach runs these steps in order: audit first, then restructure coverage, adjust deductibles based on what the audit reveals, and shop the optimized profile across the full Danish market.

Premium reduction isn't a one-time event. The most cost-effective households treat insurance as an ongoing financial decision — one that needs annual review, market comparison, and alignment with how your life has actually changed. Platforms like Inzure can run that analysis in 60 seconds, flagging gaps, overlaps, and price drift before they compound into years of overpaying.

Frequently Asked Questions

Frequently Asked Questions

How much does a $1,000,000 general liability insurance cost?

A $1 million general liability policy costs vary significantly by industry, location, and claims history — there's no single universal rate. Low-risk businesses (such as consultants) typically pay far less than contractors or trades with higher physical exposure. Always request quotes from multiple insurers before assuming the first offer is competitive.

How much should I pay for professional liability insurance?

Professional liability (E&O) costs depend heavily on your profession, annual revenue, claims history, and chosen policy limits. Consulting and advisory roles tend to sit at the lower end; hands-on technical or financial services pay more. Comparing quotes across carriers is the most reliable way to benchmark a fair rate.

What minimizes professional liability?

Documented contracts with clients, clear service scope definitions, and consistent error-handling procedures reduce both exposure and premium costs. Insurers price risk based on evidence — formalizing your processes gives underwriters concrete reasons to offer lower rates.

How often should I review my business insurance policy?

Review your policy at every renewal and after any significant change — new employees, expanded services, relocated premises, or major asset purchases. Annual market comparisons are worth doing even when nothing has changed; pricing shifts constantly between carriers.

Does raising my deductible always lower my business insurance premium?

Raising a deductible generally lowers premiums, but how much depends on the insurer's pricing model and coverage type. Request quotes at multiple deductible levels (such as $500, $1,000, $2,500, and $5,000) before committing to ensure the savings justify the increased out-of-pocket exposure.

Can bundling business insurance policies save money?

Yes — bundling multiple coverages under a single policy typically reduces total premium costs compared to buying each one separately. That said, businesses with complex or specialized needs may still require standalone policies for certain risks to ensure adequate protection.