Introduction

Danish homeowners are systematically overpaying for insurance. Research from the Danish Competition and Consumer Authority (KFST) reveals that loyal customers with 20+ years of tenure pay up to 402 DKK more annually than new customers for identical coverage—a premium penalty of 22 percentage points just for staying with the same insurer.

Overpayment rarely happens all at once. It builds through specific decisions, unchecked habits, and policy drift that compound over time. Most of it is preventable — yet homeowners keep renewing without questioning whether their coverage still makes sense or whether their premium reflects market rates.

This article covers 12 practical strategies to reduce homeowners insurance costs — from decisions you make when buying coverage, to habits that keep your premium in check year after year.

Key Takeaways

- Insurance costs grow quietly through annual renewals, policy drift, and discounts most homeowners never claim

- The biggest cost drivers are low deductibles, wrong coverage amounts, poor credit scores, and skipping the comparison market

- Lowering costs takes three moves: smarter buying decisions, active policy upkeep, and reducing home risk

- Insurers reward low-risk behaviors with discounts most homeowners never claim

- Inzure analyses your existing policy and shows what Danish carriers actually charge for equivalent coverage — in 60 seconds

How Homeowners Insurance Costs Build Up Over Time

Homeowners insurance premiums rarely spike overnight. They compound through annual renewal increases, coverage adjustments, and new risk ratings that policyholders rarely scrutinize. Danish insurance prices have increased nearly 10% more than the EU average from 1996 to 2023, with contents insurance rising 45% more than the EU average over the same period.

Many costs stay hidden until renewal. Three patterns show up repeatedly:

- Coverage that no longer matches actual rebuild costs

- Scheduled endorsements on items no longer worth their original value

- Claims history that raises base rates without notice

Insurers nudge premiums up in small increments — 2% one year, 3% the next — counting on customers to accept the increases rather than shop around.

That inertia is exactly what insurers count on — and it costs loyal customers the most. KFST data confirms that long-term customers pay higher margins than new customers. For house insurance, the gap is 6 percentage points (DKK 456 per year) between new customers and those with 20+ years of tenure. Staying put, in other words, is often the most expensive choice you can make.

Key Cost Drivers for Homeowners Insurance

Primary Structural Factors

Homeowners insurance premiums are determined by:

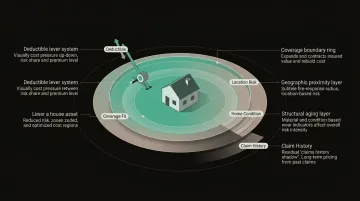

- Deductible size: Higher deductibles reduce annual premiums significantly

- Dwelling coverage limits: Should match rebuild cost, not market value

- Location and fire service proximity: Distance to fire stations affects risk ratings

- Older homes and certain construction materials increase premiums

- Previous claims raise your rates for multiple years afterward

Secondary Behavioral Factors

In Denmark, credit scores function as risk proxies. Insurers use the RKI credit default register, and homeowners registered in RKI often face higher premiums or outright coverage denials. Policy bundling decisions also matter: consolidating multiple policies with one insurer typically unlocks percentage discounts.

Risk-mitigation upgrades can also bring your premiums down. Security systems, updated electrical, plumbing, and HVAC, and storm-hardening measures all reduce what insurers consider risky about your home. These qualify you for specific discounts — but you usually have to ask for them explicitly.

Critical distinction: Cost is driven by both static factors (location, structure, age) and dynamic factors (credit, claims behavior, coverage reviews). Focusing on the dynamic factors is where most homeowners find the fastest savings.

Cost-Reduction Strategies for Homeowners Insurance

Most homeowners overpay in one of three areas: the decisions they make at purchase, how they manage their policy over time, or the risk profile of their home. The 12 strategies below address each.

Decision-Based Savings

These strategies tend to deliver the largest one-time savings — and they take effect before or at the point of purchase or renewal.

Strategy 1 — Shop Around and Compare Quotes

Premiums for identical coverage differ significantly between insurers. UK Financial Conduct Authority data shows that a typical home insurance customer with 5+ years of tenure pays £108 more than a new customer for buildings insurance—purely due to loyalty inertia.

In Denmark, approximately 14–15% of insurance policies switch providers each year — yet most homeowners stay with their current insurer while quietly paying inflated premiums. Independent comparison tools fix this. Inzure's AI-driven platform analyzes uploaded policy documents in 60 seconds, compares your coverage against actual market pricing, and shows where you're overpaying — with no obligation to switch.

Action: Upload your current policy as a PDF or photo to an independent comparison platform. Identify whether your premium reflects current market rates or loyalty-penalty pricing.

Strategy 2 — Raise Your Deductible Deliberately

Moving from a lower deductible to a higher one reduces annual premiums noticeably. Research by Forbrugerrådet Tænk found that raising a deductible from 0 DKK to 3,000 DKK reduces premiums by an average of 24.4%. Raising it further from 3,000 DKK to 5,000 DKK yields an additional 9.5% reduction.

Important caveat: This strategy only makes financial sense if you maintain savings to cover the higher out-of-pocket amount. If a claim occurs, you'll pay the deductible before insurance coverage begins. Don't raise your deductible beyond what you can afford in an emergency.

Strategy 3 — Insure the Rebuild Cost, Not the Purchase Price

The land under your home holds no insurable risk. Your policy should cover the cost to reconstruct the structure using current labor and materials—not the market value that includes land. Both under-insuring and over-insuring represent cost errors.

Topdanmark warned in 2022 that over 50% of Danish businesses risk underinsurance due to soaring inflation and material costs. The construction cost index for residential buildings in Denmark rose 2.6% year-over-year in Q4 2024, meaning rebuild costs increase independently of property values.

Action: Request a rebuild cost estimate from a certified appraiser or your insurer. Adjust your dwelling coverage to match this figure, not your home's purchase price or market value.

Strategy 4 — Factor Insurance Costs Into the Home-Buying Decision

Proximity to fire services, roof type, construction materials, and existing claims history all affect premiums before your first policy is written. A hip roof versus a gabled roof, or a home near a fire hydrant versus one distant from a fire station, can translate into hundreds of kroner in annual premium differences.

Thatch roofs in Denmark carry significantly higher premiums due to fire risk. However, documenting that your thatch roof is fireproofed (brandsikret) reduces both the insurance premium and the statutory distance requirement to neighboring properties from 10 meters to 5 meters.

Action: When evaluating properties, request insurance quotes before finalizing the purchase. Factor annual premium differences into your total ownership cost calculation.

Strategy 5 — Avoid High-Risk Property Additions

Pools, trampolines, and similar "attractive nuisances" increase liability exposure and raise premiums. Insurers may require safety nets, fences, or locked gates to maintain liability coverage, or they may exclude injuries entirely from coverage.

Action: Check with your insurer before adding pools, trampolines, or similar features. Understand the premium impact and liability requirements rather than discovering restrictions at renewal.

Policy Management Savings

Once your policy is in place, how you manage it year-to-year determines whether you stay appropriately covered — or gradually overpay.

Strategy 6 — Review Your Policy and Possessions Annually

Coverage limits drift out of alignment over time:

- High-value items depreciate, reducing their replacement value

- Renovations change rebuild costs

- Scheduled endorsements outlive their purpose

- Family circumstances change (new dependents, adult children moving out)

Conduct an annual audit:

- Verify dwelling coverage still matches current rebuild cost

- Remove endorsements for items no longer worth insuring

- Adjust personal property limits to reflect current possessions

- Update beneficiaries and coverage for household changes

Inzure customers have discovered critical gaps during annual reviews—one customer found her newborn was unnecessarily listed and charged for two years, while another realized family members were missing from multiple policies entirely.

Strategy 7 — Maintain and Improve Your Credit Score

In many markets, insurers use credit-based insurance scores to set premiums. Danish insurers rely on the RKI credit default register—homeowners registered in RKI face higher premiums for mandatory insurances and potential coverage denials for optional coverages.

Correcting credit report errors or reducing card utilization can reduce premiums without changing your home or policy at all.

Action: Request your credit report annually. Dispute any errors. Pay down high credit card balances to improve your utilization ratio.

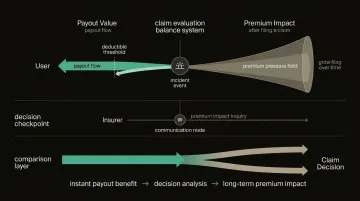

Strategy 8 — Be Strategic About Filing Small Claims

Filing a claim below three times your deductible often costs more in long-term premium increases than it recovers in claim payments. Premiums can rise after a single claim and remain elevated for multiple years.

Before filing any claim:

- Calculate the claim amount minus your deductible

- Call your insurer and ask how filing would affect your premium

- Request a specific percentage increase and duration

- Compare the claim payout to the multi-year premium increase

- Only file if the payout significantly exceeds the long-term cost

Action: Treat your insurance for major losses, not minor inconveniences. Pay small repairs out of pocket to preserve your claims-free status and discount eligibility.

Strategy 9 — Monitor Loyalty Discounts but Verify Competitiveness

Many insurers offer modest loyalty discounts after 3-5 years. However, KFST research shows these discounts are often outpaced by annual rate creep. Long-term customers pay higher margins despite receiving "loyalty benefits."

Your insurer may advertise a loyalty discount while simultaneously charging you more than a new customer would pay for the exact same coverage. The discount doesn't offset the rate creep — it just softens the optics.

Action: Compare market rates annually even as a long-term customer. Don't assume loyalty equals best price—verify it independently.

Home Context and Discount Savings

Some savings come not from your policy decisions, but from the conditions around your home — its risk profile, how your policies are structured, and which discounts you're eligible to claim.

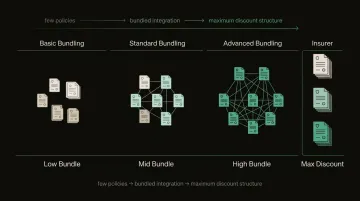

Strategy 10 — Bundle Home and Auto (and Other) Policies

Bundling multiple policies with the same insurer typically unlocks percentage discounts on both. Danish insurers offer bundling discounts (samlerabat) ranging from 10-20% depending on the number of policies combined.

Representative bundling discounts:

| Insurer | Maximum Discount | Requirements |

|---|---|---|

| Tryg | Up to 20% | 5 eligible policies including contents |

| If Forsikring | Up to 15% | 3 policies (Level 3 in If Fordelsprogram) |

| Topdanmark | Up to 12% | 3 selected policies including contents |

| Codan | 10-15% | 2-3 core policies (Kernekunde) |

Important caveat: Bundling discounts don't always apply evenly across all policies, and consumer tests indicate that combining standalone policies from companies without bundling discounts can sometimes result in lower overall costs.

Action: Calculate your bundled total and compare it against separate quotes from standalone specialists. Verify that bundling actually delivers savings rather than assuming it's always cheapest.

Strategy 11 — Harden Your Home Against Risk and Improve Security

Upgrades that reduce the insurer's modeled risk qualify for specific discounts:

Security systems: Codan offers a 20% discount on contents insurance for installing a G4S alarm system.

Water leak alarms: Tryg offers a 40% discount on pipe/cable coverage for installing an approved water leak detection system.

Storm-mitigation upgrades: Impact-resistant roofing, storm shutters, and structural reinforcements reduce risk in areas prone to severe weather.

System upgrades: Updated electrical, plumbing, and HVAC systems demonstrate lower risk and qualify for discounts.

Action: Choose upgrades that serve a practical purpose and qualify for a premium discount. Request verification requirements before installation—insurers may require inspection or certification to apply the discount.

Strategy 12 — Seek Out All Applicable Discounts

Insurers offer numerous discounts that most homeowners never claim:

- Retiree/senior discounts — Codan offers a 10% discount to members of Ældre Sagen (age 50+), recognizing that retirees spend more time at home, reducing burglary risk and enabling faster fire response

- No-claims discounts — Multi-year claims-free history qualifies for reduced premiums

- Smoke-free household discounts — Lower fire risk in non-smoking homes

- Paperless billing discounts — Administrative cost savings passed to customers

- Group or employer-affiliated discounts — Alka offers 10% discounts via trade unions and association memberships

Critical point: These discounts aren't always advertised and you must specifically ask for them.

Action: Call your insurer and ask explicitly which discounts you qualify for. Provide documentation (union membership, age verification, security system certification) to claim every eligible discount.

Conclusion

Reducing homeowners insurance costs starts with understanding what you're actually paying for. Most overpayment isn't the result of bad luck — it's the result of policies that haven't been reviewed, compared, or questioned since they were first signed.

Effective cost reduction is ongoing. Premiums change at every renewal, market rates shift, and a policy that was competitive two years ago may no longer be. Homeowners who pay less treat their insurance as something to actively manage, not passively accept.

For Danish households, platforms like Inzure automate that monitoring. Upload your policy, get a full analysis in 60 seconds, and compare actual market rates — not just whatever your current insurer quotes at renewal.

Frequently Asked Questions

How can I lower my homeowners insurance premiums?

Start by comparing quotes from multiple insurers, then raise your deductible deliberately — this alone can cut premiums by 24% or more. Bundle multiple policies with the same insurer for a multi-policy discount, and review your coverage annually to drop unnecessary endorsements or outdated scheduled items.

Can I adjust my homeowners insurance coverage to lower my premiums?

Yes, coverage limits, deductibles, and scheduled endorsements can all be adjusted to reduce premiums. However, reducing dwelling coverage below the true rebuild cost creates underinsurance risk that outweighs any premium savings. Always maintain adequate coverage for the actual cost to rebuild your home.

Do I want actual cash value or replacement cost coverage?

Replacement cost coverage pays to rebuild at current prices; actual cash value deducts depreciation, leaving you to cover the gap. Choose replacement cost for dwelling coverage — the higher premium is worth the protection against major losses.

What is the 80% rule in homeowners insurance?

Denmark uses a proportional underinsurance clause instead of a strict 80% rule. If your sum insured falls below the property's replacement value, claims are reduced proportionally — insured for 1 million DKK on a 2 million DKK home, a 200,000 DKK claim pays out only 100,000 DKK.

Do seniors get a discount on home insurance?

Many Danish insurers offer discounts to homeowners aged 50-55+ who are retired. The discount recognizes that retirees spend more time at home, reducing burglary risk and enabling faster response to fires or maintenance issues. Availability and discount size vary by insurer—ask explicitly to claim this benefit.

How much does homeowners insurance cost for a 4,000,000 DKK house?

In Denmark, house insurance typically ranges from 4,000-10,000 DKK annually, while contents insurance averages 1,500-3,000 DKK annually. Actual cost varies significantly by location, construction type, coverage selected, and claims history. Remember: insure based on rebuild cost, not purchase price or market value.