Introduction

Across Europe's coastlines, home insurance premiums have surged sharply in recent years as insurers price in rising storm and flood risk. In Denmark, coastal and waterfront properties regularly face combined annual costs — covering building insurance, water damage riders, and storm deductibles — that can run 40–70% higher than comparable inland homes. For many households, that gap runs into tens of thousands of kroner per year.

The cost gap isn't simply a reflection of genuine risk.

The decisions you make — which coverage you carry, what deductibles you accept, and whether you ever compare your policy against the market — determine how much of that cost is genuinely necessary. This guide breaks down the specific factors driving coastal premiums higher and covers practical strategies for bringing them down without leaving yourself underprotected.

Key Takeaways

- Coastal home insurance typically spans multiple policies: building coverage, flood insurance, and storm/stormflod add-ons

- Key cost drivers: distance to water, roof condition, flood zone, and thin insurer competition

- Reduce costs through smarter coverage choices, active policy management, and storm-damage hardening

- Comparing quotes helps — but knowing what's actually driving your premium is what produces real savings

- Most coastal homeowners overpay simply because no one has reviewed their policy since they first signed it

How Coastal Home Insurance Costs Typically Build Up

Coastal insurance costs rarely arrive as a single visible number. They accumulate across:

- Main dwelling policy covering structure, contents, and liability

- Separate flood insurance (standard homeowners policies exclude flooding)

- Wind or hurricane deductible calculated as a percentage of your home's insured value (commonly 2–5%), not a flat dollar amount

For example, a homeowner with a 2,500,000 kr. insured coastal dwelling and a 2% wind deductible faces a 50,000 kr. out-of-pocket cost before wind-damage coverage activates — on top of their annual premiums.

Cost build-up is unpredictable. Premiums can stay flat for years, then spike sharply after:

- A major storm season that drains insurer reserves

- Carrier re-underwriting based on updated risk models

- An insurer exiting your coastal market entirely, leaving fewer competitors and higher prices

When carriers withdraw from a coastal market or revise their risk models, the remaining insurers face less competitive pressure — and prices reflect that. Danish coastal homeowners along exposed stretches of Jutland or Funen have seen this pattern directly: fewer competing carriers means renewal quotes that climb steeply, with little warning before the invoice arrives.

Key Cost Drivers for Coastal Home Insurance

Geographic Proximity and Flood Zone Classification

The single most powerful driver is your distance to the coastline and your property's flood risk designation. Insurers assess:

- Distance to open water or tidal areas

- Elevation above sea level

- Official flood zone classification (high-risk vs. low-risk zones)

Flood risk pricing is increasingly property-specific rather than zone-wide. Properties in high-risk coastal zones typically face higher base rates, mandatory separate flood coverage requirements, and annual premium increases until rates reflect the full assessed risk. Even modest improvements in a property's measured elevation or risk classification can translate into meaningful premium reductions.

Roof Age and Construction Features

Your roof is a major underwriting variable — and often the one that surprises homeowners most. An aging or non-impact-rated roof on a coastal property significantly increases insurer exposure to storm and wind damage. Many insurers will:

- Surcharge premiums for roofs over 10–15 years old

- Restrict coverage options for older or unrated roofs

- Decline to cover the property without replacement

Certified storm-resistant features — impact-resistant roofing, reinforced connections between roof and walls, and storm shutters — directly reduce your risk profile and, in many markets, earn documented premium discounts that insurers are required to apply.

Insurer Market Dynamics

When private carriers exit high-risk coastal markets — or sharply restrict what they'll cover — competitive pressure drops and premiums rise for everyone who remains. Homeowners in exposed coastal zones often find their options narrowing to state-backed or pooled insurer programs, which typically carry higher costs and more limited coverage than private alternatives.

This dynamic means the market you're shopping in matters as much as your individual property characteristics. Fewer competing carriers means less incentive for any single insurer to offer you a sharper price.

What's Actually Driving Your Specific Premium

Coastal policies are complex and often layered across multiple coverage types, which means most homeowners can't pinpoint which specific factors are inflating their bill. Geographic risk, roof age, and market conditions all interact — and insurers aren't required to explain the weighting.

Auditing your own policy documents — or having them analyzed systematically — is the only reliable way to identify which cost drivers are actually embedded in your premium, rather than guessing.

Cost-Reduction Strategies for Coastal Home Insurance

The most effective strategies differ depending on whether your costs are driven by upfront coverage choices, how the policy is managed over time, or the physical and regulatory environment surrounding your property. The highest-impact savings usually come from addressing all three dimensions.

Strategies That Reduce Costs by Changing Your Coverage Decisions

Get Rebuild Cost Right (Not Market Value)

Many coastal homeowners over-insure for some things while being dangerously underinsured for others. The critical decision: insure for rebuild cost (replacement cost value), not market value. Rebuilding after a storm can cost far more than the property's sale price. Getting this number wrong in either direction creates problems:

- Too high: You pay premiums on coverage you'll never use

- Too low: You're underinsured when disaster strikes

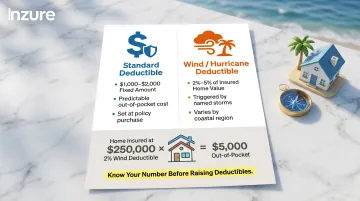

Understand Your Wind Deductible

Raising a standard deductible can lower premiums, but coastal homeowners must also understand their wind or hurricane deductible—typically calculated as a percentage of insured dwelling value (often 2–5%). According to the Insurance Information Institute, doubling a standard deductible can reduce premiums by 10–25% — though exact savings vary by market and insurer.

Know what your percentage deductible means in dollar terms. A 2% deductible on a home insured for 250,000 in dwelling coverage equals a 5,000 out-of-pocket cost before insurance covers wind damage. This helps you decide how much cash reserve you need before raising deductibles further.

Bundle Strategically

Bundling home, auto, and flood policies with the same insurer (or insurer group) can unlock meaningful multi-policy discounts. This works best when a single insurer covers coastal properties, so ask specifically about bundling options when getting quotes from coastal specialists.

Trim Add-On Coverages

Review and trim add-ons that may no longer match your actual situation:

- Loss-of-use limits that exceed your needs

- Scheduled personal property riders for items you no longer own

- Duplicate liability coverage that overlaps with an umbrella policy

Strategies That Reduce Costs by Changing How the Policy Is Managed

Review Annually Before Renewal

Coastal insurers regularly re-underwrite policies at renewal—meaning premiums can be adjusted based on updated risk models, claims data, or market conditions without you noticing until the bill arrives. 47% of U.S. homeowners reported a premium increase in the prior year, the highest level in over a decade.

Reviewing your policy every year before renewal (not just paying automatically) is one of the highest-leverage habits coastal homeowners can build. Ongoing market monitoring can catch these silent increases and alert you before you overpay another year.

Shop Specialist Coastal Insurers Every 2–3 Years

Different insurers weight coastal risk factors differently. A carrier that was the most competitive option three years ago may no longer be. Shop actively across specialist coastal insurers every two to three years rather than relying on the same carrier for loyalty.

Research what type of specialist coastal or regional insurers operate in your area—they often understand local risk better and price more competitively than national carriers.

Protect Your Claims-Free Discount

Filing small claims (for amounts close to your deductible) can trigger premium increases or non-renewal in high-risk coastal markets where insurers already operate on thin margins. Reserve insurance for major losses and self-fund smaller repairs to protect your claims-free discount and your ability to renew coverage.

These policy management habits compound over time. The structural improvements below take that further by directly changing how insurers assess your property's risk.

Strategies That Reduce Costs by Changing the Context Around the Property

Invest in Home Hardening

Home hardening is the most direct way for coastal homeowners to influence their own risk profile and qualify for mitigation discounts. Key upgrades include:

- Impact-resistant roofing

- Storm shutters or impact-rated windows

- Hurricane straps to anchor roof structure

- Reinforced garage doors

Many coastal markets — and some government programs — offer inspection schemes or grant assistance for approved storm-resistance improvements. Ask your insurer for a list of eligible upgrades and the corresponding discount schedule before starting any renovation work. Structural improvements typically qualify for mitigation discounts, though the exact amounts vary by property and carrier.

Consider Proximity to Fire Services

Proximity to fire stations and the quality of local water supply infrastructure affects premiums even in coastal areas — independent of storm risk. Communities that invest in fire infrastructure over time can see corresponding premium reductions for all homeowners in the area. It's worth understanding how your local fire protection rating influences your specific policy pricing.

Know Your Last-Resort Coverage Options

When private insurers exit a coastal market, most jurisdictions maintain a residual market or insurer of last resort — a state-backed or government-mandated scheme that steps in when private coverage is unavailable. These programs typically carry higher costs and more limited coverage than private alternatives.

If you find yourself in this position, two steps matter most:

- Understand what the residual scheme covers and where the gaps are

- Seek a supplemental private policy to cover perils the residual scheme excludes

Checking periodically whether private market options have returned — and comparing them against your current residual coverage — can reveal significant savings once competitive insurers re-enter your area.

Conclusion

The goal isn't simply to pay less — it's to pay the right amount for the right coverage. Coastal homeowners who cut costs carelessly often discover the gap when a storm claim comes back short. Effective cost reduction means identifying which specific cost drivers are at work in your policy, then applying the right strategy to each.

This is not a one-time task. The coastal insurance market shifts as storms occur, carriers enter and exit, and flood risk zone assessments are updated. Homeowners who review and compare their policy annually will consistently pay less — and keep their coverage aligned with their actual risk.

Frequently Asked Questions

How to negotiate a lower home insurance rate?

Start by getting competing quotes from specialist coastal insurers and use them as leverage with your current carrier. Point to specific home improvements—new roof, storm shutters, hurricane straps—or a clean claims history to request a discount or rate review. Insurers often match or beat competitor offers when presented with documented evidence.

What not to say to a homeowners insurance adjuster?

Avoid speculating about causes of damage, admitting fault, or underestimating losses on the spot. Document everything thoroughly with photos and receipts, and let the written evidence speak rather than making verbal statements that could be used to limit your payout. Ask for itemized explanations of settlement offers.

How does your home's location affect the cost of insurance?

Location determines risk exposure across several dimensions: distance to the coast, flood zone classification, local crime rates, and proximity to fire services. Coastal proximity is one of the most significant single factors — insurers assess distance to water and property elevation to calculate premiums on an individual basis.

Do I need separate flood insurance for a coastal home?

Yes — standard homeowners insurance does not cover flood damage. Coastal homeowners should consider a separate flood policy through a government-backed program or private insurer, since even properties outside official high-risk flood zones can experience storm surge during major storms.

What is a wind or hurricane deductible and how is it different from a standard deductible?

A wind or hurricane deductible is percentage-based — commonly 2–5% of the home's insured value — and applies specifically to wind-related claims in coastal areas. Unlike a flat-dollar standard deductible, the amount you pay out of pocket scales with your home's insured value. On a home insured for 500,000 with a 2% deductible, that's 10,000 before coverage kicks in.

Can home improvements really lower my coastal insurance premium?

Yes — structural upgrades tied to storm resistance can qualify for meaningful mitigation discounts in many coastal markets. Impact-rated roofing, hurricane straps, and storm shutters are commonly recognized improvements under wind mitigation discount programs. Ask your insurer for a schedule of eligible upgrades and corresponding discounts before starting any renovation work.