Introduction

Many Danish consumers face a familiar sales pitch: bundle your insurance and save. Insurers like Tryg, Topdanmark, and Codan actively promote samlerabat (multi-policy discounts) with promises of convenience and lower premiums. But here's what most people don't realize: those bundled "deals" aren't always the cheapest option. A 2025 test by Forbrugerrådet Tænk found a staggering 5,700 kr gap between the cheapest and most expensive bundled packages for the same coverage—and four of the six cheapest companies didn't offer bundling discounts at all.

The choice between bundled and separate policies directly affects what you pay, what you're covered for, and how easily you can switch when life changes. With Danish households spending an average of 15,900 kr annually on insurance (4.4% of total consumption), even small adjustments can put thousands of kroner back in your pocket:

- Annual premium — bundled pricing isn't always lower than shopping separately

- Coverage quality — packages can include gaps or overlap you won't notice until you claim

- Flexibility — locking into one insurer can cost you when your needs shift

Below, you'll find a clear framework for comparing both approaches—including the hidden factors, like loyalty surcharges and duplicate coverages, that most Danes never think to check.

Key Takeaways

- Bundling offers discounts of 5–25%, but the actual savings depend on the insurer's base rates and your policy mix

- Separate policies let you cherry-pick the best provider for each coverage type, often beating bundled prices

- Hidden costs of bundling include silent premium increases, duplicate protections, and cross-policy rate hikes after claims

- The right choice depends on your risk profile and how closely you track what you're actually paying each renewal

- Compare both options every year at renewal — not just when you first sign up

Bundled vs. Separate Insurance: Quick Comparison

Here's how the two approaches compare across the factors that matter most to your wallet and peace of mind.

| Factor | Bundled | Separate |

|---|---|---|

| Premium Savings | Multi-policy discount typically 5–25% off combined premiums. Tryg offers up to 20%, Topdanmark up to 12%, Codan up to 15%. | No bundling discount, but access to best-in-class rates per coverage type. Tænk's 2025 test found the cheapest overall provider offered no samlerabat. |

| Coverage Flexibility | Standardized packages that may not fit unique needs. Harder to customize one policy without affecting the rest. | Full flexibility to tailor each policy independently — choose limits, endorsements, and providers that match your risk profile. |

| Admin Simplicity | Single renewal date, one bill, one claims contact. Simpler to manage. | Multiple renewal dates and contacts. More active management, but more control. |

| Claims Impact | A claim on one policy may affect renewal pricing across all bundled policies with the same insurer. | A claim typically only affects that specific policy's premium — others stay unaffected. |

| Long-Term Cost Risk | Loyalty can breed complacency. Insurers raise rates at renewal knowing bundled customers rarely switch — Tænk documented increases of up to 37% for some customers. | Easier to switch one policy at a time without disrupting all coverage, making annual price shopping practical. |

What is Bundled Insurance?

Bundled insurance means purchasing two or more policies—most commonly home and auto, but also renters, life, boat, motorcycle, or umbrella—from the same insurer under one account, usually in exchange for a multi-policy discount.

The discount mechanism works through direct premium reduction: insurers lower your combined cost as an incentive for customer consolidation. The discount appears as a percentage off one or both policies, not as a separate line item. In Denmark, major insurers offer varying tiers:

| Insurer | Maximum Discount | Tier Structure | Required Base Policy |

|---|---|---|---|

| Tryg | 20% | 10% (3 policies), 15% (4), 20% (5+) | Indboforsikring |

| Topdanmark | 12% | 8% (2 types), 12% (3 types) | Indboforsikring |

| If Skadeforsikring | 15% | Level 1: 10%, Level 2: 15%, Level 3: 15% + advisory | Kasko, indbo, or hus |

| Codan | 15% | 10% (2 categories), 15% (3+) | Varies by category |

Beyond the discount, bundling comes with several practical advantages:

- Single deductible when one event damages multiple insured assets — for instance, when a storm damages both your car and home at once

- Unified renewal dates across all policies, reducing administrative overhead

- Loyalty rewards that compound as you add more policies to your account

- Priority claims handling offered by some insurers to multi-policy customers

The most commonly bundled policies in Denmark include indboforsikring (contents/renters), bilforsikring (auto), husforsikring (home), and ulykkesforsikring (accident). These four form the standard household benchmark used by Tænk's testing framework when evaluating Danish insurers.

Use Cases of Bundled Insurance

Bundling works best for consumers with straightforward, standard risk profiles:

- Families with a regular home and one or two vehicles

- Renters combining auto and contents insurance

- Homeowners adding umbrella coverage on top of existing home and auto

Bundling is most advantageous when all your needs fall within one insurer's standard product range. If you require niche coverage — such as sommerhus (holiday home) insurance, campingvogn (caravan) policies, or fritidsbåd (leisure boat) coverage — specialist providers often outperform generalist bundlers on both price and terms.

What is Separate Insurance?

Separate (unbundled) insurance means purchasing each policy type independently from whichever provider offers the best combination of price, coverage, and service for that specific risk—rather than consolidating under one insurer.

The core financial logic: if Provider A offers the best home rate and Provider B offers the best travel rate, the combined cost of two separate best-in-class policies may be lower than a bundled discount on mediocre-rate policies from a single insurer.

Example: Suppose Company X offers bundled home + accident insurance for 8,000 kr with a 15% discount (9,412 kr before discount). Company Y offers home insurance alone for 4,200 kr, and Company Z offers accident insurance alone for 3,500 kr. The separate approach costs 7,700 kr total—300 kr less than the "discounted" bundle, plus potentially better coverage from each specialist.

Coverage quality matters just as much as price. Separate policies let you choose the right limits and coverage options for each risk without compromise—particularly important for consumers with above-average needs, such as an older home, valuable belongings, or a risk history that requires tailored coverage.

Use Cases of Separate Insurance

Separate policies benefit consumers with complex or high-value situations:

- Owning property in a flood-prone area requiring a specialist insurer

- Insuring a bicycle or high-value item needing specialist coverage

- Having a risk history that makes one category expensive regardless of bundling

Separate insurance also suits consumers who actively price-shop at every renewal—those willing to compare quotes annually can consistently find competitive rates without committing to a single provider.

Bundled vs. Separate: Which Saves You More on Premiums?

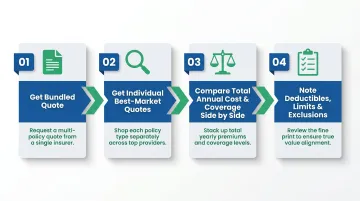

Determining which is cheaper requires doing the actual math—not assuming bundling wins. The correct comparison method:

- Get a bundled quote from one insurer with full policy details

- Get individual best-in-market quotes for each policy type

- Compare total annual cost AND coverage levels side by side

- Note deductibles, limits, and exclusions—not just premium

Comparing premiums alone without reviewing coverage levels is a common mistake that can leave you underinsured.

The Loyalty Tax Problem

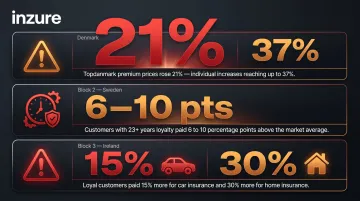

Insurers count on bundled customers being less likely to switch, which allows them to raise premiums gradually at renewal while still technically offering a "multi-policy discount." Tænk states directly: "Det er dyrt at være loyal kunde i forsikringsselskaber" (It is expensive to be a loyal customer with insurance companies).

Real-world data confirms this:

- Tænk's 2025 test documented Topdanmark prices up over 21%, with individual consumers facing increases up to 37%

- Swedish data shows that customers staying 23+ years received premium increases 6–10 percentage points higher than average

- In Ireland, loyal customers paid approximately 15% more for car insurance and 30% more for home insurance compared to new customers

Over 3–5 years, the initial bundling savings can be fully eroded by incremental rate increases that you never questioned.

Duplicate Coverage Risk

Bundled packages can include overlapping protections that consumers pay for twice:

- Travel insurance already covered by credit cards or the Danish public health card (det gule sundhedskort)

- Liability coverage included in both indboforsikring and umbrella policies

- Legal aid (retshjælp) bundled into standard indbo when you have a separate legal protection policy

- Roadside assistance covered by both auto policy and FDM membership

These duplicates inflate the effective premium without adding real protection. Tænk recommends self-insuring for small risks you can afford out-of-pocket rather than layering redundant coverage.

When Bundling Genuinely Wins

Bundling delivers real savings when:

- The multi-policy discount percentage beats the total of best-individual-market rates

- The insurer's base rates are competitive (not inflated to offset the discount)

- A single-deductible clause applies, saving costs in multi-policy claim events

- Your risk profile is standard enough that one insurer can competitively cover all categories

None of these conditions can be confirmed without comparing both structures directly — which is where most consumers stop short.

Cutting the Comparison Time

Manually requesting quotes from multiple Danish insurers and cross-referencing coverage levels takes hours. Inzure's platform reads your existing policy documents (PDF or photo upload) and runs that comparison in 60 seconds — identifying overpayment, duplicate coverages, and whether bundling or splitting policies costs less. You get a structured report showing gaps and overlaps, with no obligation to switch.

Run a free policy analysis to see whether your current bundle is genuinely the cheapest option or if splitting policies could save you thousands.

Conclusion

Neither bundling nor separating policies wins universally. Bundling offers convenience and real savings for consumers with standard, straightforward needs—but it is not automatically the cheapest option, and the savings can erode over time without active monitoring. Separate policies demand more effort but reward consumers who invest time in annual comparison shopping with both better rates and better coverage fit.

The bigger risk is failing to reassess. Insurance needs change, insurer rates shift, and the bundled deal you signed three years ago may no longer reflect market reality. Yet only 20% of Danish consumers switched providers in the previous two years — most simply accept renewal increases without checking whether better options exist.

Treat your insurance portfolio as something to review annually, not set and forget. Tools like Inzure can run that check in 60 seconds — flagging price increases, coverage gaps, and better market rates across Danish carriers — so staying on top of it no longer requires hours of manual research.

Frequently Asked Questions

Is it always cheaper to bundle insurance policies?

No. Bundling offers discounts, but is not guaranteed to be cheaper. It depends on the insurer's base rates and your individual risk profile. Tænk's 2025 test found the cheapest provider offered no bundling discount at all, while companies with 15–25% discounts were still more expensive overall.

What types of insurance are typically bundled together in Denmark?

The most common combinations are indboforsikring (contents) and bilforsikring (auto), home and contents, and multi-policy packages including ulykkesforsikring (accident) or husforsikring (house). Tænk's standard test uses these four household policies as the benchmark bundle.

Can bundling insurance lead to coverage gaps?

Yes. Standardized bundle packages may not include the specific endorsements or limits you need—such as high-value jewelry coverage or elektronikdækning for electronics. Some bundles drop important protections to keep premiums low. Always compare coverage details alongside price before committing to a bundle.

When should I consider switching from a bundled to separate policies?

Consider switching when renewal premiums have risen significantly (check for loyalty surcharges), when you've acquired a high-value or specialist asset that needs tailored coverage, or when a competitor offers substantially better rates for one of your policy types on its own.

How do I accurately compare the true cost of bundled vs. separate insurance?

Quote both options at identical coverage levels—same deductibles, limits, and endorsements—and factor in long-term renewal trends, not just the first-year premium. Also check for duplicate coverages. Use Forsikringsguiden.dk or platforms like Inzure to benchmark across multiple providers at once.

Does making a claim affect all policies if they are bundled?

With bundled policies, a claim on one policy can influence the insurer's risk assessment at renewal, potentially raising premiums across your entire bundle. Separate policies generally contain any claims impact to that specific policy only.