This isn't an accident. It's a structural feature of how the insurance industry operates — and it's precisely why insurance savings calculators exist.

This guide explains how savings calculators work, what factors they measure, how to navigate the deductible-premium tradeoff, and which hidden costs drain your budget. You'll also learn how to act on your results effectively, whether that means negotiating with your current provider or making an informed switch.

Key Takeaways

- Insurance savings calculators estimate potential savings by analyzing your coverage, deductible, and provider against market rates

- The 2,000–3,000 kr deductible range delivers the strongest premium reduction (24.4% on average) without excessive financial risk

- Loyalty penalties, auto-indexation, and duplicate coverage quietly drain thousands from Danish households each year

- Bundling discounts of 10–20% sound appealing, but separate policies from different insurers often cost less overall

- Inzure analyzes your existing policies in 60 seconds, benchmarking premiums and flagging gaps automatically

What Is an Insurance Savings Calculator?

An insurance savings calculator takes inputs about your current policy — premium, deductible, coverage types, provider — and estimates how much you could save by changing one or more variables. This might mean switching providers, adjusting your deductible, or removing redundant coverage you didn't know existed.

Quote comparison tools vs. savings calculators:

Most comparison tools show what a new policy costs. A savings calculator goes further by accounting for your current policy's terms, coverage gaps, loyalty pricing, and claim history. This produces a more complete picture of your actual savings potential.

Inzure reads your actual policy documents and benchmarks your premiums against real market rates across Danish insurers including Tryg, Alka, Topdanmark, Codan, GF, Alm. Brand, and If — completing the full analysis in approximately 60 seconds, compared to the 10+ hours manual research typically requires.

How they work:

- Upload your policy documents (PDF or photo)

- AI extracts key details: coverage scope, premiums, exclusions, deductibles

- The system benchmarks against current market data

- You receive a report showing gaps, overlaps, and potential savings

Instead of wondering whether you're overpaying, you see exactly where your premiums sit relative to competitive market rates.

What Factors Does an Insurance Savings Calculator Measure?

Premium vs. Coverage Quality

Calculators don't just compare prices — they evaluate whether your premium reflects the coverage you're actually receiving. A policy with a low base price but major exclusions may cost more in the long run than a higher premium with comprehensive protection.

For example, a cheap home contents policy might exclude bicycle theft for high-value bikes, require add-ons for accidental damage, or cap liability coverage below recommended levels. You won't discover these gaps until you file a claim.

Deductible Level

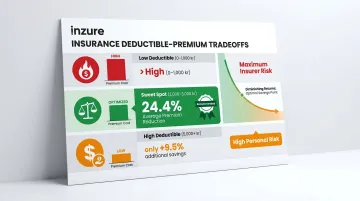

Your deductible directly affects your premium. Savings calculators model the break-even point — how many claim-free years it takes for a higher deductible to pay off versus a lower one.

Research from Forbrugerradet Tænk analyzing 14 Danish insurers shows that moving from 0 kr to 3,000 kr selvrisiko reduces home contents premiums by 24.4% on average. Going from 3,000 kr to 5,000 kr yields only an additional 9.5% reduction — the marginal benefit diminishes significantly above 3,000 kr.

Loyalty Pricing

The Danish Competition and Consumer Authority (Konkurrencerådet) documented this phenomenon in April 2025. The pattern is widespread across the market:

- Long-term customers pay on average 1,108 kr/year more than new customers for equivalent coverage

- Some insurers extract 30-35 percentage points higher margins from loyal customers

- The top 5 Danish insurers control ~80% of total revenue, limiting competitive pressure

- Danish insurance prices have risen 45% more than the EU average for house and home coverage since the mid-1990s

Duplicate and Overlapping Coverage

Approximately one-third of Danes are over-insured, particularly in travel insurance. Common overlap sources include:

- Credit card travel insurance (unknowingly included)

- Travel agency policies sold to already-covered travelers

- Union membership benefits

- Pension scheme bundled coverage

- Triple-covered baggage via airline liability, home contents, and separate travel policy

Calculators flag these redundancies by cross-referencing your active policies.

Understanding the Deductible-Premium Tradeoff

A deductible is the amount you pay out-of-pocket before insurance coverage begins. A higher deductible lowers your monthly or annual premium but increases your financial exposure when a claim occurs. Getting this balance right is what separates smart insurance decisions from expensive ones.

The Core Mechanic

If choosing a higher deductible saves you 800 kr/year in premiums, but the deductible is 1,500 kr higher, it takes nearly two claim-free years to break even. If you file a claim in year one, you've lost money.

Example calculation:

- Policy A: 2,500 kr/year premium, 1,000 kr deductible

- Policy B: 1,700 kr/year premium, 3,000 kr deductible

- Annual savings: 800 kr

- Additional out-of-pocket risk: 2,000 kr

- Break-even: 2.5 claim-free years

The 2,000-3,000 kr Sweet Spot

According to Forbrugerradet Tænk's analysis, the 2,000-3,000 kr selvrisiko range offers the best risk-reward tradeoff for most Danish families. It delivers substantial premium reductions without requiring emergency funds beyond what most households should maintain anyway.

Financial experts like Vanguard recommend maintaining emergency savings of at least the equivalent of 14,000 kr or 2-4 weeks of expenses, factoring in insurance deductibles. If your emergency fund comfortably clears that threshold, a higher deductible becomes a realistic option.

When Higher Deductibles (5,000+ kr) Make Sense

A 5,000 kr or higher deductible shifts significant financial risk onto you. It pays off only under specific conditions:

- Maintain emergency savings large enough to cover the deductible without hardship

- Own newer assets (home, possessions) with lower claim probability

- File claims rarely and want to minimize ongoing premium costs

Without sufficient emergency funds, a high deductible can force you into debt if a claim occurs.

How Deductibles Apply

In Danish property insurance, deductibles apply per claim event, not annually. If multiple items are damaged in a single incident, you pay only one deductible. Filing frequent small claims risks premium increases or policy cancellation, so set your deductible at the highest amount you could cover immediately from savings — no more.

Hidden Reasons You're Overpaying on Insurance

The Loyalty Penalty

Insurance companies offer their best prices to new customers, not loyal ones. Auto-renewal locks you into prices that rise each year — often well above inflation or claims history.

The Konkurrencerådet's April 2025 investigation found that a 10-year customer contributes 7-8 percentage points more to insurer earnings than a new customer. Vulnerable groups — customers aged 65+, those with limited education, and low financial literacy — are disproportionately affected.

This practice is so widespread that Danish insurers use annual index adjustments tied to wage development as a standard contract term, requiring no individual customer notification. Premiums index upward, but the sum insured (coverage amount) often is not indexed correspondingly. You progressively pay more for proportionally less coverage.

Duplicate Coverage Across Policies

Many people pay for the same coverage multiple times:

- Roadside assistance from your auto policy often duplicates what your credit card already covers

- Travel insurance can appear on your credit card, through union membership, via your pension scheme, and as a separate purchase — all at once

- Bicycle theft is frequently covered under both a standalone bicycle policy and your home contents insurance

- Legal aid bundled into home contents is often purchased again as a standalone policy

These overlaps are rarely obvious because they're buried in different policy documents.

Outdated Coverage Levels

Life changes aren't automatically reflected in your insurance:

- Home renovations increase property value, but your sum insured stays the same

- You pay off your car loan but maintain the same coverage level

- Children leave home, reducing liability exposure

- You replace expensive items with cheaper alternatives but maintain high coverage limits

Each of these gaps means you're either underinsured or overpaying — sometimes both.

Overlooked Discounts

Danish insurers offer bundling discounts (samlerabat) of 10-20%, but Forbrugerradet Tænk warns this is "rarely the cheapest solution." Buying individual policies from different companies can be cheaper.

Common unclaimed discounts:

- Safety device installations, such as approved smoke alarms and locks

- Union or professional association membership — IDA Forsikring, for example, offers members 15% off

- Claims-free history

- Paying annually rather than monthly

There's another catch with bundling: a Finanstilsynet study found that a claim on one product (car insurance) can trigger a price increase on another (home insurance) — a penalty most customers never see coming.

Unnecessary Add-Ons and Riders

Danish home contents policies include common optional extras (tilvalg) that policyholders accepted at sign-up and forgot about:

Frequently redundant add-ons:

- Accidental damage (pludselig skade) — often overlaps with manufacturer warranties

- Electronics damage — sometimes already included under accidental damage coverage

- Extended bicycle coverage — unnecessary if your bike's value is low

- Identity theft protection — base policies frequently cover this partially through legal aid

- Travel and cancellation insurance — high duplication risk with credit cards and union benefits

- High-value items cover — only relevant if you own jewelry or luxury goods

Reviewing and removing unused riders generates meaningful savings without reducing actual protection.

How to Act on Your Insurance Savings Calculator Results

Interpreting Your Savings Estimate

Not all savings are equal. A calculator might show 3,000 kr/year potential savings from switching providers — but switching involves time, possible coverage gaps during transition, and the risk of losing claim history benefits with your current insurer.

Critical questions to ask:

- Does the cheaper policy have the same coverage breadth?

- Are there exclusions or higher deductibles that explain the lower price?

- Will switching affect my ability to file a current claim?

- What's the cancellation timeline and transition process?

Don't chase the largest number without understanding what you're gaining or losing.

Use Results as Negotiating Leverage

That caution doesn't mean staying put. Armed with market data and competitor quotes, many Danish policyholders negotiate directly with their current insurer for meaningful rate reductions — without switching at all.

The cancellation department tactic:

Contact your insurer's opsigelsesafdeling (cancellation department), not standard customer service. This team has authority to offer significant price reductions that front-line agents cannot.

Consumer-reported results from Danish households:

- Showing competitor quote: ~2,000 kr/year savings (Tryg, retained customer)

- Initiating switch, retention call: ~4,000 kr/year savings (Alm. Brand cancellation dept offer)

- Full switch: ~5,000 kr/year savings (Topdanmark to GF Forsikring)

How to approach the conversation:

- Use Forsikringsguiden.dk to obtain 2-3 written quotes

- Call your insurer and state you're considering switching

- Present the competitor quotes with specific pricing

- Ask for a rate reduction to match or beat the market rate

- If the front-line agent says no discounts are possible, explicitly request to speak with the cancellation department

Run a Full Policy Review, Not Just a Quote Comparison

The most powerful use of an insurance savings calculator is combined with a full policy audit — examining what you're covered for, what's missing, and what's redundant.

Inzure is built specifically for this. Upload your existing policies (PDF or photo) and receive an independent AI analysis in approximately 60 seconds that:

- Benchmarks your premiums against the full Danish market

- Identifies coverage gaps (missing bicycle theft, insufficient liability limits, absent legal aid)

- Flags duplicate coverage across multiple policies

- Quantifies loyalty surcharges vs. new customer rates

- Models different deductible scenarios

The analysis is free with no obligation to switch. When you do act on a better deal, Inzure handles the transition and charges 20% of your annual savings — and if the switch delivers better coverage at the same price, the service costs nothing.

Most Danish households have never had a clear picture of what their policies actually cover or what they should cost. This is what changes that.

Frequently Asked Questions

Will my premium go up if I lower my deductible?

Yes, lowering your deductible generally increases your premium because the insurer takes on more financial risk per claim. The exact change varies by insurer, policy type, and how significant the deductible adjustment is.

Is it better to have a 1,000 kr or 2,000 kr deductible?

A 2,000 kr deductible is better if you have savings to cover the higher out-of-pocket cost and want lower premiums. A 1,000 kr deductible is safer if you have limited emergency funds or higher likelihood of claims. The right choice depends on your financial cushion and risk tolerance.

Is a 5,000 kr deductible high?

Yes, 5,000 kr is a high deductible for most standard Danish insurance types, meaning you absorb significant upfront risk in exchange for lower premiums. It works best if you have solid emergency savings and rarely file claims.

How much can I realistically save by comparing insurance providers?

Savings vary widely depending on policy type, current insurer, and how long you've been a customer. The Konkurrencerådet found that 10+ year loyal customers pay on average 1,108 kr/year more than new customers for equivalent coverage. Consumer-reported savings from switching or negotiating range from 1,000 to 5,000 kr/year, with the highest gains achieved by long-term customers.

How often should I review my insurance policies?

Review your policies at least once a year, ideally before renewal, and after any major life event — such as a move, marriage, new vehicle, or home renovation. Coverage needs and market pricing both change regularly, and annual reviews ensure you're not paying for outdated or unnecessary coverage.