Introduction

Danish consumers face a stark reality: insurance prices have surged by over 91% since 2000, significantly outpacing the 56% increase in the general consumer price index. Yet the problem isn't inflation alone — it's structural pricing inequality. A 2025 report by the Danish Competition and Consumer Authority (KFST) reveals that loyal customers pay a loyalty penalty of 7-8 percentage points higher margins on home and contents insurance compared to new customers, with some Danish insurers applying penalties reaching 30-35 percentage points.

Overpaying is the norm, not the exception. Only 28% of active Danish consumers compare prices across providers, despite a 14.5% annual switching rate. Most people pay too much not because they're high-risk, but because they never actively manage their policies or question what they're actually paying for.

This guide covers nine practical, evidence-backed strategies for reducing insurance costs across policy types, organised by where costs can realistically be cut.

Key Takeaways

- Loyal customers pay 7-8% higher premiums than new customers—this is deliberate industry pricing, not accidental

- Tests show spreads of over 5,000 DKK per year between cheapest and most expensive providers for identical coverage

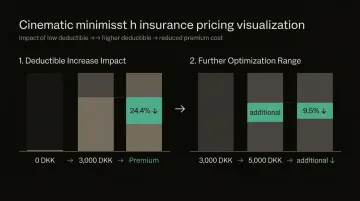

- Raising deductibles from 0 DKK to 3,000 DKK reduces premiums by an average of 24.4%

- Bundling discounts reach 20%, yet comparison tests show it's rarely the cheapest overall option

- Annual policy audits surface duplicate coverage and gaps most consumers never discover

How Insurance Costs Typically Build Up

Insurance costs rarely spike dramatically. Instead, they accumulate through small annual increases, coverage drift, and auto-renewals that go unquestioned. Many Danish consumers notice overpayment only when they finally compare quotes—which 72% never do.

Cost build-up compounds fast. A 5-8% annual price increase on a policy already above market rate doubles the gap within a few years — with no change in your risk profile.

One documented case shows a customer's annual premium rising from 4,800 DKK in Year 1 to 7,200 DKK by Year 10 — a 50% increase driven entirely by loyalty penalties, not increased risk.

These costs stay hidden until someone audits the full policy portfolio — which most consumers never do. The usual culprits:

- Duplicate coverage across multiple policies you've accumulated over time

- Unnecessary add-ons bundled in at renewal without explanation

- Loyalty penalties that push long-term customers above the market rate

Left unchecked, these gaps cost Danish households hundreds — sometimes thousands — of kroner every year.

Key Cost Drivers for Insurance Premiums

Risk Profile and Coverage Decisions

Primary factors that determine premium pricing include:

- Claims history - Fewer claims over time reduces home and personal insurance premiums

- Property characteristics - Security systems, age, location affect home insurance

- Coverage scope and limits - Higher limits and lower deductibles increase cost

- Location-based actuarial data - Postal code significantly impacts pricing

Each of these factors is adjustable. Improving home security, filing fewer small claims, or recalibrating your coverage limits can meaningfully reduce what you pay year over year.

Structural Market Drivers

Beyond individual choices, structural forces in the Danish insurance market push premiums higher — often without consumers noticing:

Loyalty tax: Insurers reward new customers with discounts while gradually raising rates for existing ones. Research confirms customers with 10+ years of tenure face margins 7-8 percentage points higher than brand-new customers for identical coverage.

Consumer inertia: Most households never switch or renegotiate. With only 28% of active consumers comparing prices, insurers face little pressure to price competitively for existing customers.

Market transparency gaps: Consumers who cannot easily see what competitors charge for the same coverage cannot pressure their insurer to adjust pricing. Inzure was built specifically for this problem — upload your policy documents and see the real market price for your coverage in 60 seconds, without the hours of manual comparison most consumers abandon halfway through.

Nine Ways to Lower Your Insurance Costs

The nine strategies below fall into three categories: decisions made at purchase or renewal, how policies are managed over time, and external factors that affect your risk profile. The most effective cost reduction combines strategies from all three categories.

Strategies That Reduce Costs by Changing Your Decisions

These decisions—made before or at renewal—directly shape your premium and have the highest immediate impact on cost.

Strategy 1: Shop Around and Compare Quotes

Premiums for identical coverage vary significantly between insurers because each company calculates risk differently. Forbrugerrådet Tænk tests show spreads of over 5,000 DKK annually between cheapest and most expensive providers for identical coverage profiles.

Shopping must involve like-for-like comparison of coverage limits, deductibles, and exclusions—not just headline price. Many insurers advertise steep discounts but maintain higher baseline prices, making comparison essential.

Example pricing variation:

- Lærerstandens Brandforsikring: 14,242 DKK (cheapest)

- Alka: 16,434 DKK

- Codan: 19,937 DKK (most expensive, despite bundling discount)

The 5,695 DKK difference between cheapest and most expensive represents 40% higher cost for identical protection.

Strategy 2: Bundle Multiple Policies with One Provider

Approximately 7 out of 10 major Danish insurers offer bundling discounts (samlerabat):

- Tryg: Up to 20% for 5 qualifying policies

- Codan: Up to 15% for 3 qualifying policies

- Topdanmark: Up to 12% for multiple policies

Forbrugerrådet Tænk explicitly warns that bundling is rarely the cheapest option. Tests reveal it's often cheaper to buy policies individually from different providers, as a company offering cheap contents insurance might simultaneously overcharge for travel coverage. Always compare bundled quotes against separate quotes before committing.

Strategy 3: Raise Your Deductible Strategically

Increasing your deductible (selvrisiko)—the amount paid out of pocket before insurance pays—reduces your premium. Forbrugerrådet Tænk analysis of 14 insurers reveals a clear sweet spot:

| Deductible Increase | Average Premium Reduction |

|---|---|

| 0 DKK → 3,000 DKK | 24.4% decrease |

| 3,000 DKK → 5,000 DKK | 9.5% additional decrease |

The most significant savings come from moving away from a 0 DKK deductible to a moderate level (2,000-3,000 DKK), after which marginal savings diminish rapidly.

Only raise deductibles if you have savings to cover the higher out-of-pocket cost in case of a claim. Setting a 5,000 DKK deductible when you cannot afford a 5,000 DKK expense leaves you exposed to out-of-pocket costs you can't cover.

Strategy 4: Adjust or Remove Coverage That No Longer Fits

Many households carry coverage that exceeds actual need:

- Comprehensive collision on older vehicles - When a car's value drops below 30,000-40,000 DKK, comprehensive coverage may cost more than potential claim payouts

- Coverage limits far above asset value - Insuring contents for 1,000,000 DKK when actual belongings are worth 400,000 DKK wastes money

- Add-ons duplicated elsewhere - Forbrugerrådet Tænk advises against purchasing individual electronics warranties when your contents insurance already includes electronics coverage

Audit your policies annually to identify and trim excess coverage without creating dangerous gaps.

Strategies That Reduce Costs by Changing How Insurance Is Managed

These approaches reduce cost through better visibility and control during active coverage. They often go unaddressed because they require ongoing attention, not a one-time decision.

Strategy 5: Review Your Full Policy Portfolio Annually and Eliminate Duplicates

Overlapping coverage is more common than most people expect:

- Travel insurance included in premium credit cards (such as Mastercard Gold or Platinum) that duplicates standalone annual travel policies

- Roadside assistance in both home and auto policies

- Electronics coverage duplicated across multiple policies

Conducting a full audit at each renewal cycle surfaces both redundancies and gaps. Most consumers never complete this audit because it traditionally requires 10+ hours of manual document review.

Inzure's AI-powered analysis eliminates that barrier — scanning policies across all Danish insurers in 60 seconds, automatically identifying duplicates, coverage gaps, and whether your current premium reflects actual market rates. One customer discovered she had been without home contents insurance for 10 years while simultaneously carrying redundant coverage elsewhere.

Strategy 6: Avoid Filing Small Claims to Protect Your Premium Record

Frequent small claims signal higher risk to insurers, leading to premium increases or loss of no-claims discounts (skadesfri rabat) that can far exceed the value of the claim itself.

Before filing a claim, calculate whether the repair cost exceeds your deductible by a meaningful margin. If a repair costs 3,500 DKK and your deductible is 3,000 DKK, filing for a 500 DKK net benefit may trigger premium increases of 1,000-2,000 DKK annually for 3-5 years.

Always file claims for significant losses, liability incidents, or situations where documentation protects your legal position.

Strategy 7: Monitor and Improve Your Credit Score

In some European insurance markets, credit history is used as a risk proxy. However, in Denmark and the broader EU, the use of automated credit scoring to price insurance is heavily restricted by GDPR Article 22, which grants data subjects the right not to be subject to decisions based solely on automated processing.

Danish insurers instead rely on alternative risk proxies:

- Age (older policyholders generally receive lower premiums)

- Postal code

- Property size and characteristics

- Historical claims data

While credit scores don't directly impact Danish insurance pricing, maintaining financial stability ensures you can afford higher deductibles, which reduce premiums meaningfully.

Strategies That Reduce Costs by Changing the Context Around Insurance

These external and behavioural factors reduce the risk profile insurers use to price premiums. They require more time but create durable, compounding savings.

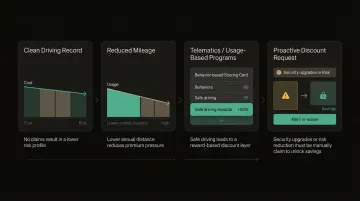

Strategy 8: Improve Your Risk Profile Through Behaviour and Property Upgrades

For home insurance: Installing security systems, smoke detectors, upgraded plumbing, or approved window locks reduces risk and earns discounts. The insurer If offers up to 10% discount for approved burglar alarms connected to a control centre, and up to 20% discount for homes with both alarms and approved window locks.

For auto insurance:

- Maintain a clean driving record

- Reduce annual mileage

- Enrol in telematics or usage-based programmes that reward safe driving

Proactively inform your insurer of any changes. Insurers do not automatically adjust your premium when you install security systems or reduce risk — you must request the discount.

Strategy 9: Seek Out Group Discounts, Loyalty Protections, and Structured Discount Programmes

Association-based insurance: Group insurance through employers, alumni associations, or professional organisations can offer meaningful reductions. Member-owned mutuals operate differently than traditional insurers. For example, LB Forsikring returned 135 million DKK to members in 2025 who had held contents policies for at least three continuous years.

No-claims discount protection: This paid add-on preserves your accumulated discount after a single claim. It's worth considering if your discount is substantial (40-60% after several years), as one at-fault claim without protection could eliminate years of savings.

Some insurers reward long-term customers with loyalty discounts, but these are far less common than loyalty penalties. Verify whether your insurer actually rewards or punishes tenure before assuming loyalty benefits exist.

Conclusion

The strategies in this guide target three distinct sources of overpayment: decisions made at purchase or renewal, gaps in ongoing policy management, and unchecked risk profiles. Addressing all three — not just the most obvious one — is what separates a meaningful reduction from a minor adjustment.

Cost reduction is not a one-time exercise. Premiums shift annually, market rates change, and personal circumstances evolve. The consumers who pay fair prices treat insurance as an active financial decision, not a passive subscription. Regular comparison shopping, annual policy audits, and strategic risk reduction create compounding savings that reach thousands of kroner annually — in some cases over 10.000 kr per year, based on real consumer outcomes. A platform like Inzure can surface these gaps in 60 seconds by analyzing your existing policies against current market rates, so the effort required is far lower than most people expect.

Frequently Asked Questions

How can you reduce the cost of insurance?

The most effective approaches combine shopping around for competitive quotes, bundling policies where genuinely cheaper, raising deductibles where financially safe, and auditing existing coverage annually to remove duplicates and unnecessary add-ons. Combined, these strategies can reduce premiums by 24–46% depending on your coverage profile.

How do I know if I'm paying too much for home insurance?

The clearest signal is that you haven't compared quotes in the past 12 months. Danish insurers regularly adjust pricing, and loyal customers often end up paying more than new ones. Running an independent comparison — or uploading your policy for AI analysis — typically reveals whether your current rate still reflects the market.

How often should I review my insurance policies?

Once a year, ideally before your renewal date. Annual reviews catch price increases, duplicate coverage across policies, and gaps that have opened up as your circumstances change — such as moving, acquiring new valuables, or changing family size.

How can I lower my liability insurance?

Liability premiums can be reduced by comparing quotes across insurers, improving the underlying risk profile (driving record, property security), and reviewing whether current liability limits are higher than legally or practically necessary for your asset exposure.

How to lower insurance rates for new drivers?

Complete an accredited driver's education or defensive driving course for a discount, be added to a parent's multi-vehicle policy where possible, choose a vehicle with lower insurance risk ratings, and enrol in telematics programmes that reward safe driving from the start.

Is it worth paying for no claims discount protection?

No-claims discount protection makes sense when your accumulated discount is substantial — typically 40–60% after several claim-free years — since one at-fault claim without protection can wipe out years of savings. Weigh the add-on cost against the size of the discount at risk and your realistic likelihood of making a claim.