Introduction

Danish insurance customers who stay loyal to their provider pay 7-8% more on average than new customers, according to a 2025 report from Denmark's Competition and Consumer Authority. For ASU policyholders, the loyalty penalty is only part of the story.

In September 2025, Finanstilsynet ordered major insurers to fix their loss-making sickness and accident portfolios, warning that price increases haven't kept pace with rising claims costs. Market-wide premium hikes are now structural — not temporary.

Most ASU policies cost between 150-400 kr monthly. Over a 10-year term, a 25% overpayment on a 300 kr policy compounds to 90,000 kr in wasted premiums. The overpayment isn't inherent to the product — it comes from decisions made at purchase and the absence of ongoing review.

TL;DR

- ASU costs accumulate through unchallenged auto-renewals and wage-indexed premium hikes

- Deferred period, benefit amount, occupation class, and duplicate employer coverage drive the largest cost variations

- Savings require smarter choices at purchase, active monitoring, and eliminating coverage overlaps

- Most overpayment persists because insurers profit from complexity and customer passivity

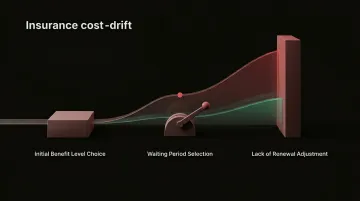

How ASU Insurance Costs Build Up Over Time

ASU insurance costs don't arrive as a single bill. They accumulate gradually through monthly premiums that auto-renew with incremental price increases.

In Denmark, most insurers apply annual wage-indexation to premiums without separate notification. The Danish Competition Authority found this indexation acts as tacit price coordination because increases are embedded in standard contract terms rather than flagged explicitly.

Cost build-up is driven by three compounding decisions:

- Benefit level chosen at inception — once locked in, most people never recalibrate even when income or expenses change

- Deferred period set at purchase — selecting a 30-day wait instead of 90 days can double the premium for coverage you may not need

- Absence of renegotiation — the original purchase decision continues to cost you disproportionately year after year

These three decisions compound quietly — but there's a second cost layer that's even easier to miss: coverage overlap. Many Danes hold ASU through a mortgage arrangement, employer benefit package, or separate income protection policy. Since insurers won't allow double-payment for the same loss, you're paying multiple premiums for coverage that can only pay out once.

Key Cost Drivers for ASU Insurance

Deferred Period

Your waiting period before benefits begin is the single most direct lever on your premium — and most people set it too short. A 30-day deferral costs noticeably more than 60 or 90 days, yet many choose it by default without checking whether their savings or employer sick pay already covers that gap.

If your employer provides eight weeks of full sick pay and you hold two months of expenses in savings, paying extra for 30-day cover is redundant.

Benefit Level

Most policies set benefit level at 50–65% of gross monthly income, and cost scales proportionally. The common mistake is calibrating to income rather than actual essential outgoings — mortgage, utilities, food.

If your essential monthly costs are 12.000 kr but 65% of your gross income is 18.000 kr, you're paying to insure 6.000 kr of discretionary spending that doesn't need protection.

Occupation Class

Insurers fix your occupation class at application — and policyholders rarely think to challenge it. Higher-risk roles attract higher premiums, but if your role has changed since you applied, your rate may not reflect that.

Moving from manual construction work to site supervision, for example, can shift your risk classification. If you haven't reviewed this since taking out the policy, you may be overpaying for a job you no longer do.

Age and Health Status

Age and health status at application affect underwriting terms — and on many policies, those terms are locked in from day one. Delaying purchase does increase lifetime costs, but buying at the right time with the wrong structure still inflates what you pay unnecessarily.

Timing matters. Structure matters more.

Policy Structure

Choosing between accident and sickness only, full ASU, or unemployment-only cover directly affects cost. Before defaulting to the broadest tier, consider whether you genuinely face unemployment risk:

- Public sector employees with strong job security may not need unemployment cover

- Those with substantial redundancy packages already have a financial buffer

- Self-employed individuals often need a different structure entirely

Paying for unemployment protection you're unlikely to trigger is one of the most common — and avoidable — sources of over-spend.

Cost-Reduction Strategies for ASU Insurance

ASU savings require matching the right strategy to the right cost driver. Cutting genuine sickness cover to save premiums creates financial risk. Addressing structural overspend—wrong deferred period, duplicate coverage, wrong benefit level—delivers savings without compromising protection.

Strategies That Reduce Costs by Changing Decisions

Start with the deferred period. Before selecting a 30-day waiting period, calculate how many weeks your employer's sick pay and personal savings could actually cover. Extending from 30 to 60 or 90 days can cut monthly premiums substantially while leaving genuine financial exposure unchanged for most employed workers.

Right-size the benefit level to essential outgoings only:

- List fixed monthly commitments: mortgage or rent, utilities, minimum food spend, loan repayments

- Insure that figure — not a percentage of gross salary

- The gap between actual essential costs and 65% of salary is often 4.000–6.000 kr

- Every unnecessary krone of benefit level increases the premium

Before paying for the unemployment component of ASU, assess whether you actually face meaningful redundancy risk. Contract type, employer stability, and sector all matter. Accident and sickness-only cover is often considerably cheaper if involuntary redundancy is unlikely.

A UK FCA study found wide price dispersion for income protection products, meaning customers with similar risk profiles pay vastly different prices depending on the insurer. Comparing the full market before committing or renewing costs nothing — the savings potential is significant.

Strategies That Reduce Costs by Changing How ASU Is Managed

Most policyholders only think about their ASU cover when they first buy it — and insurers count on that. Premiums for existing customers rise faster than quotes for new customers with identical profiles. The fix is straightforward: get a new-customer comparison at every renewal and use it as leverage to negotiate or switch. Research shows 85% of consumers who negotiated received a price reduction.

Beyond renewal, watch for changes that make your current policy partly redundant. If your employer introduces group income protection or extends sick pay terms, the coverage gap your ASU fills shrinks — and so should your benefit level.

Tools like Inzure's policy analysis flag duplicate coverage, pricing anomalies, and gaps across Danish insurers in about 60 seconds. Running a check before each renewal takes less time than the premium increase costs you.

Set a calendar reminder 60 days before your renewal date. Policies that auto-renew without a comparison check are the main way overpayment quietly compounds year on year.

Strategies That Reduce Costs by Changing the Context Around ASU

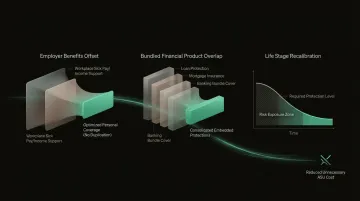

In many cases, the real cost driver is duplication — paying for ASU alongside other products that already cover the same risk. Three places this overlap typically hides:

- Employer benefits: Group income protection, extended sick pay, or employer mortgage schemes can significantly reduce or eliminate the coverage gap that personal ASU needs to fill. Quantify what your employer provides before calculating what to insure.

- Bundled financial products: ASU-type protections are frequently embedded in mortgage protection packages, loan add-ons, and current account benefits. Many households pay for the same underlying risk across two or three separate products.

- Changed life circumstances: A paid-down mortgage, financially independent children, or a larger emergency fund all reduce the financial exposure ASU needs to cover. Recalibrate benefit levels when obligations shrink — premiums follow.

Conclusion

Reducing ASU insurance costs starts with understanding where overspend originates—whether from a mismatched deferred period, an inflated benefit level, duplicate coverage, or unchallenged loyalty pricing—rather than cutting cover and accepting more risk.

Effective ASU cost reduction is a continuous process, not a one-time task. The most cost-efficient policyholders revisit their policy whenever life changes — a new job, a pay rise, a paid-off mortgage — and check the market annually rather than waiting for renewal letters to dictate the agenda.

The key levers covered in this guide:

- Deferred period: Extend it if you have savings or employer sick pay to cover the gap

- Benefit level: Align it with actual monthly commitments, not a round number

- Duplicate coverage: Check what your employer, mortgage lender, or existing policies already cover

- Loyalty pricing: Treat renewal as a trigger to compare, not a reason to auto-renew

Frequently Asked Questions

What does sickness and accident insurance cover?

Accident and sickness insurance pays a monthly benefit if you are unable to work due to illness or injury, typically replacing 50-65% of income. Pre-existing conditions are usually excluded, and most policies require medical underwriting at application.

What is the maximum benefit period under an accident, sickness, and unemployment policy?

Most ASU policies pay out for a maximum of 12 to 24 months per claim. This is much shorter than long-term income protection policies, which can pay out until retirement age.

What is the maximum payout for unemployment insurance?

Unemployment benefit under an ASU policy is typically capped at 50-65% of pre-claim monthly income for a maximum of 12 months. The exact limit depends on the policy terms and chosen benefit level.

What is the waiting period for ASU insurance and how does it affect my premiums?

Waiting (deferred) periods typically range from 30 to 90 days. Choosing a longer deferred period significantly reduces the monthly premium—making it a key lever for cost management without reducing the total amount you can claim.

Can I have both ASU insurance and income protection at the same time?

You can hold both policies at once, but insurers will not pay out on both for the same loss of income. Overlapping cover means paying two premiums for protection you can only claim once.

Is ASU insurance worth it if my employer already provides sick pay?

The key question is how large the gap is between your employer's sick pay and your essential outgoings. If savings can cover a short shortfall, a longer deferred period or accident-only cover is often sufficient — and noticeably cheaper.