Introduction

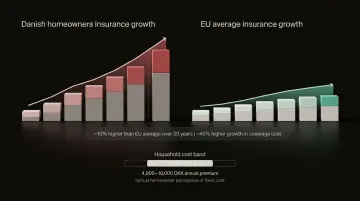

Danish homeowners insurance premiums have risen nearly 10% more than the EU average over the past three decades, with house and contents coverage increasing almost 45% more than comparable European markets. Many homeowners treat their annual premium—typically between 4.000–10.000 DKK—as a fixed household expense determined entirely by location and property age.

The reality is different. A significant portion of your premium is shaped by decisions you can control.

Roof condition, electrical systems, water protection devices, and security installations all factor into your insurer's risk assessment. Targeted improvements in these areas can meaningfully reduce what you pay, but only if you understand which upgrades matter and ensure your insurer actually credits them.

This article breaks down how premiums are calculated, what drives the cost, and which home improvements give you the most direct leverage over your annual bill.

Key Takeaways

- Loyal customers often pay 7% more than new customers for identical coverage due to compounding annual renewal increases

- Insurers price based on claim probability, so improvements reducing fire, water, theft, or storm risk lower your premium

- Water leak detectors, roof replacement, electrical upgrades, and monitored security systems deliver the highest savings

- Documenting improvements and reporting them to your insurer is essential—discounts are rarely applied automatically

- Some renovations (pools, extensions) raise premiums by increasing replacement value—check the impact before committing

How Home Insurance Premium Costs Build Up Over Time

Home insurance costs rarely appear as one large visible expense. Instead, they accumulate through small annual increases at renewal—often framed as market adjustments or claims inflation—so most homeowners never connect the total cost to specific, changeable features of their home.

A 2025 report by the Danish Competition and Consumer Authority reveals the scale of this problem. Customers with 10+ years of tenure pay an average margin of 27%, compared to 20% for new customers—a 7 percentage point difference that translates to 445 DKK in annual overpayment. The gap exists because insurers automatically index existing customers' premiums using wage growth rates that historically exceed inflation, while new customers receive competitive introductory pricing.

This pricing gap doesn't emerge from nowhere — it's driven by specific risk thresholds that trigger upward reassessments at renewal:

- A roof aging past 30 years flagged as a structural liability

- Outdated wiring identified during an inspection

- A claims history that shifts your risk profile upward

Your premium reflects your home's risk profile at each renewal point, not a fixed baseline. The gap between what you currently pay and the market rate for your actual risk level is often invisible without an independent comparison. Loyal customers who never review their policy are statistically the most likely to be overpaying.

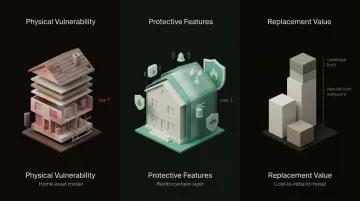

Key Cost Drivers for Home Insurance Premiums

Insurers price based on the probability and potential severity of a claim. The structural condition and protective systems of your home are among the most influential variables in the pricing model—more so than many homeowners realize.

Main driver categories include:

- Physical vulnerability — Roof condition, building materials, age of electrical and plumbing systems

- Protective features — Alarms, suppression systems, weather reinforcements, leak detection

- Replacement value — The cost to rebuild your home relative to your coverage limit

Fire damage is the most expensive claim category in Denmark, with an average compensation of 87,000 DKK per claim. In 2022 alone, nearly 41,000 fire claims totalled 3.5 billion DKK.

Water damage is equally common. Danish insurers received over 22,000 cloudburst claims in 2023—the highest number since 2011.

These figures show where insurers concentrate their risk exposure—and where targeted home improvements can have the most impact on your premium. The exact savings depend on your geography (storm exposure, crime rates), home age, and your insurer's risk model. Start with the largest risk driver in your home first.

Cost-Reduction Strategies for Home Insurance Through Smart Improvements

Effective cost reduction depends on targeting the right risk category—structural vulnerability, active protection, or policy management—rather than making random upgrades and hoping for a discount.

Strategies That Reduce Costs by Changing Decisions About Your Home's Structure

These improvements modify the physical fabric of your home, reducing the insurer's expected claim severity and producing lasting premium reductions.

Roof Replacement or Upgrade

The roof is the single most weighted structural factor in most home insurance pricing models. Rather than offering upfront premium discounts, Danish insurers apply strict age-based depreciation to older roofs during claims. For example, Alm. Brand depreciates roofing felt by 20% after 15 years, 50% after 20 years, and 80% after 30 years.

Replacing an ageing roof with modern, weather-resistant materials resets this depreciation schedule and lowers both the insurer's projected claim cost and the likelihood of a major payout. While US insurers offer 10-20% direct premium reductions for Class 4 impact-resistant roofs, Danish homeowners benefit by avoiding severe claim deductions rather than receiving upfront discounts.

Weather-Resistant Windows and Storm Protection

Reinforcing openings through impact-resistant glazing, storm shutters, or reinforced garage doors directly reduces wind and storm damage risk. Between January 2023 and June 2025, over 131,000 weather-related claims were reported to Danish insurers—meaning 3 out of 100 adult Danes experienced property damage.

In regions with high storm exposure, this category of improvement can unlock meaningful discounts and should be documented with an inspection report. In hurricane-prone US states, installing impact-rated windows or approved shutters can reduce wind premiums by 10-30%.

Upgrading Electrical Wiring and Plumbing

Outdated systems are among the most common reasons insurers apply risk surcharges or decline coverage. According to the Danish Emergency Management Agency, 19% of residential fires are caused by electrical faults or failures. For plumbing, Danish insurers heavily depreciate old pipes—Alm. Brand pays 100% for repairs up to 30 years old, but only 25% for pipes over 50 years old.

Modernising these systems removes significant flags from the underwriting assessment and can unlock both lower premiums and access to more competitive insurers. In the US, underwriting guidelines explicitly exclude homes with any of the following from standard coverage:

- Knob-and-tube wiring

- Aluminium wiring

- Polybutylene plumbing

Strategies That Reduce Costs by Changing How Your Home Is Protected

Active deterrence and detection systems reduce the probability of a claim occurring in the first place. Unlike structural upgrades, these discounts can often be applied to an existing policy mid-term—no need to wait for renewal.

Monitored Security Systems

The size of the discount correlates directly with system capability. A basic local alarm provides a small reduction, while a central-station-monitored system that alerts police and fire departments delivers meaningfully larger savings.

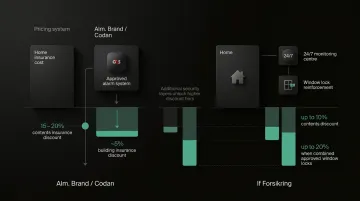

Danish discount tiers:

- Alm. Brand/Codan: 15-20% discount on contents insurance and 5% on building insurance for approved G4S alarm systems

- If Forsikring: Up to 10% discount on contents insurance for approved alarms connected to a 24/7 control centre, up to 20% when combined with approved window locks

To qualify, alarms must typically be F&P-approved (Forsikring & Pension) and connected to an approved control centre with a maximum response time of 20-35 minutes depending on security level.

Smart Home Protection Devices

Leak detection sensors, smart smoke detectors, pipe freeze sensors, and connected carbon monoxide alarms reduce the frequency and severity of water and fire claims. Danish insurers are aggressively subsidising water leak detection:

- Tryg: 40% discount on pipe coverage for approved water security alarms (e.g., Grohe Sense)

- If Forsikring: 10-25% discount on pipe and extended water damage coverage for CE-approved water shut-off systems

- Alka: 20% discount on pipe damage coverage for Grohe Sense Guard installation

- Topdanmark/Alm. Brand: Distributing LeakBot sensors to 160,000 customers to prevent water claims

Approximately 17% of Danish households have home security systems and 15% have energy management systems—higher than the European average of 10%.

Sprinkler and Fire Suppression Systems

Interior sprinkler systems significantly reduce expected damage from fire events. According to the US National Fire Protection Association, average property loss per fire is 55% lower in homes with sprinklers compared to homes without automatic extinguishing systems.

While US insurers offer 5-13% premium discounts for NFPA 13D sprinkler systems, major Danish retail carriers do not publicly publish standard percentage discounts for private residential sprinklers. However, installation costs combined with reduced out-of-pocket loss exposure create a measurable long-term financial case.

Strategies That Reduce Costs by Changing the Context Around Your Policy

The surrounding conditions determine whether improvements translate into actual savings. In many cases, the home improvement is only half the equation—the real cost driver is whether the insurer is documenting and actively crediting the improvement.

Document Every Improvement and Report It to Your Insurer Proactively

Insurers do not automatically reduce premiums when homeowners make improvements. Discounts must be requested and supported with documentation—receipts, permits, inspection reports, before-and-after photos. Waiting until renewal is common but unnecessary, as policy adjustments can typically be made mid-term.

Many homeowners who have made qualifying improvements are still paying the pre-improvement rate because their insurer never reassessed. Proactive reporting ensures you receive the savings you've earned immediately, rather than continuing to subsidise the insurer's margin.

Time Improvements Strategically and Be Alert to Improvements That Raise Rather Than Lower Premiums

Additions that increase your home's replacement value—pools, extensions, or high-end kitchen and bathroom remodels—will typically raise premiums because they increase both dwelling coverage needs and liability exposure. Understanding this distinction before investing helps you prioritise cost-reducing over cost-increasing renovations.

Danish policy terms explicitly state that failing to report these upgrades can void coverage or reduce payouts. Report both improvements and additions proactively; the insurer needs the full picture either way.

Verify That Your Insurer Actually Applied the Discount You Are Entitled To

Using an independent platform like Inzure to analyse your current policy against market benchmarks can reveal whether you are receiving the lower rates your home improvements have earned—or whether you are still paying the pre-improvement price.

Inzure's AI-powered analysis reads your policy documents, compares your coverage and pricing against other Danish carriers, and identifies gaps, overlaps, and pricing errors. The 60-second analysis is free, and you only pay 20% of annual savings if Inzure finds a better deal and you choose to switch.

Conclusion

Home improvements reduce insurance costs when they target the specific risk factors inflating your premium — not when they're the most expensive upgrades. Structural vulnerability, absent protection systems, and undocumented upgrades are the three most common sources of avoidable cost.

The right improvement depends entirely on your situation. A homeowner with a 20-year-old roof has a different priority than one with outdated wiring or no security system. What matters across all cases is the same: act on the improvement, document it, and then confirm your insurer has actually reduced your premium.

That last step is where many homeowners lose out. If you're unsure whether your current policy reflects your home's real risk profile, tools like Inzure can analyze your existing coverage and show you what the market actually charges for a home like yours — in about 60 seconds.

Frequently Asked Questions

What home improvements can lower homeowners insurance?

The highest-impact categories are: roof replacement, monitored security systems, electrical and plumbing upgrades, weather-resistant reinforcements, and water leak detection. The actual reduction depends on your home's risk profile and your insurer's discount structure.

Do home improvements automatically lower your insurance premium?

No. Improvements do not automatically trigger premium reductions. You must report changes to your insurer, provide documentation (receipts, permits, inspection reports), and request a reassessment. Many qualifying improvements go uncredited because the insurer was never informed.

How much can a new roof lower homeowners insurance?

In Denmark, a new roof does not typically trigger a direct premium discount. It does, however, reset the depreciation schedule — protecting you from steep claim deductions (up to 80%) that apply to older roofs during a damage event.

Does a security system reduce home insurance costs?

Yes. Monitored security systems reduce premiums, and the discount tier depends on system capability. Local alarms yield smaller reductions (5-10%), while central-station systems with fire and police dispatch monitoring yield the largest discounts (15-20% on contents insurance in Denmark).

Which home improvements raise insurance costs instead of lowering them?

Improvements that increase replacement value or liability exposure—pools, home extensions, large detached structures, and high-end kitchen or bathroom remodels—typically require coverage increases, which raise premiums. Danish insurers explicitly require notification of these changes, and failure to report can void coverage.

Do home extensions or renovations raise my insurance premium?

Yes — any addition that increases your home's rebuild value must be reported to your insurer. Extensions, finished basements, or major remodels raise the required coverage limit, which increases your premium. Failing to update your policy can leave you underinsured after a claim.