This article explains how Danish insurers evaluate home condition, which inspection findings matter most for your premium, and concrete steps to turn inspection results into real savings. You'll learn what repairs deliver the greatest insurance impact and how to use documented improvements as leverage when comparing providers.

Key Takeaways

- Danish home insurance has risen 45% faster than the EU average since the mid-1990s—condition-based discounts are now worth pursuing

- Roof age, electrical systems, and plumbing drive your premium—these are the areas insurers weight most heavily in risk calculations

- A tilstandsrapport (condition report) surfaces maintenance issues you can fix before they raise your renewal rate

- Documented repairs to high-risk systems give you concrete leverage to negotiate lower rates

- Loyal customers pay 7–8% more than new customers at identical risk; combining inspections with a market comparison reclaims that gap

How Insurers Use Your Home's Condition to Set Your Premium

Insurance companies fundamentally price the probability of a claim. A poorly maintained home is statistically more likely to generate expensive claims—water damage, fire, structural failure—so insurers charge more to offset that risk.

Danish insurers gather information about your home's condition through several channels:

- Self-reported data from policy applications and renewals

- Property records and satellite imagery to assess roof age and visible condition

- Mandatory inspections for older homes or high-value properties

- Tilstandsrapporter (condition reports) submitted by homeowners or required for ejerskifteforsikring (change-of-ownership insurance)

A formal home inspection provides documented, credible evidence that you can present to insurers. Two identical-looking homes on the same street can have dramatically different premiums based on what's happening with their roofs, wiring, plumbing, and heating systems. Insurers weight these systems heavily because they correlate directly with the most common and costly claims.

That home-level risk sits inside a market where premiums are already climbing fast. Danish house and home insurance prices have risen 45% more than the EU average since the mid-1990s, according to the Danish Competition and Consumer Authority (KFST). Market concentration—with the top five carriers controlling roughly 80% of revenue—drives strong profitability and automatic premium indexation tied to wage indices, not necessarily actual risk.

Climate costs are pushing premiums further. Climate-related damage exceeded DKK 3 billion in 2023 alone, with fire and water damage together accounting for approximately two-thirds of all building and contents payouts.

What Drives Your Premium

Insurers use condition-based underwriting to price your risk accurately. The European Insurance and Occupational Pensions Authority (EIOPA) promotes "impact underwriting" that links property-level mitigation to lower risk-based premiums. Features like storm-resistant roof tiles, upgraded electrical panels, and floodproof installations can reduce your premium—but only if documented and disclosed.

What Home Inspections Reveal That Directly Affects Your Rate

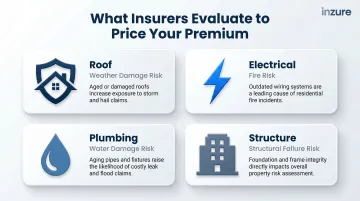

Understanding what inspectors evaluate helps you prioritize upgrades and repairs that deliver the biggest insurance impact. Here are the systems Danish insurers care about most.

The Roof

Your roof is the first line of defense against weather damage—the leading source of home insurance claims in Denmark. Inspectors assess:

- Age and remaining lifespan of roofing materials

- Condition: cracked tiles, worn felt, damaged flashing

- Material type: whether materials meet current building standards

- Signs of improper repair or deferred maintenance

Denmark experienced its wettest year since 1874 in 2023, with storm surges and cloudbursts generating thousands of claims. The October 2023 storm surge alone produced approximately 2,186 claims and DKK 1.1 billion in damage. A new or recently replaced roof with quality materials can noticeably reduce your premium; an aging or damaged roof can trigger surcharges or coverage restrictions.

Coverage implications: If your tilstandsrapport flags a known roof defect, damage arising from that defect may be excluded as not "sudden and unforeseen" until you complete repairs. Danish home insurance covers sudden events, not gradual deterioration from lack of maintenance.

Electrical and Plumbing Systems

Faulty electrical systems are a leading cause of residential fires, making outdated wiring a significant risk factor for insurers. Inspectors look for:

- Outdated wiring types (aluminum, knob-and-tube)

- Panel age, capacity, and grounding issues

- Non-compliant or illegal installations

Approximately one in three fires in Denmark are caused by electricity, according to Sikkerhedsstyrelsen (the Danish Safety Technology Authority). Roughly 1,000 fires per year stem from electrical installations or appliances, with electricity contributing to 10–15% of fire fatalities.

In 2022, electrical faults were the most frequent known cause among large fires exceeding DKK 1 million, with 92 such cases recorded.

On the plumbing side, inspectors check:

- Pipe material (older materials prone to corrosion or leaks)

- Signs of leaks, water damage, or moisture intrusion

- Water heater age and condition

Outdated plumbing materials are tied to water damage claims—another top payout category for Danish insurers. Some carriers, such as Alka, offer premium discounts if you install an approved water security system to mitigate hidden pipe damage.

Insurability note: Damage due to illegal or non-compliant electrical installations is typically excluded from coverage until corrected. This makes inspection-driven remediation both a safety and financial priority.

Structural Integrity and Safety Features

Inspectors evaluate:

- Foundation condition and signs of settling or cracking

- Structural soundness of load-bearing walls and supports

- Presence and function of safety features: smoke detectors, carbon monoxide detectors, fire suppression systems

Structural deficiencies — foundation cracks, compromised load-bearing walls — can result in higher premiums or outright denial of coverage. Addressing them before renewal puts you in a stronger negotiating position. Homes with documented safety features, on the other hand, often qualify for targeted discounts: Alka, for instance, grants reductions for fireproofing thatched roofs and installing approved water security systems.

These carrier-level incentives reflect a broader regulatory shift. EIOPA's work on impact underwriting identifies premium benefits for property-level risk reduction — storm-resistant roof connections, impact-resistant windows, floodproof doors. Not every Danish insurer publishes a formal discount schedule for these upgrades, but the pattern is consistent: bring documented proof of improvements to your renewal conversation, and you have concrete grounds to negotiate.

What to Do After a Home Inspection to Actually Lower Your Premium

A home inspection report is only valuable if you act on it strategically. Follow these steps to translate findings into real premium savings.

Step 1: Review the Inspection Report Strategically

Not all findings carry equal weight with insurers. Prioritize repairs that directly affect the systems insurers care about most:

- Roof integrity and weatherproofing

- Electrical panel capacity and wiring compliance

- Plumbing material and leak risk

- Structural soundness and safety features

Cosmetic issues like peeling paint or outdated fixtures will not move the needle on your premium. Systemic safety issues—faulty wiring, roof damage, water intrusion—will.

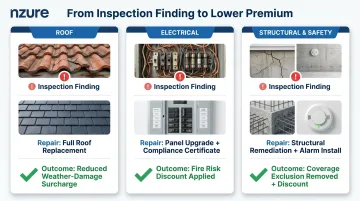

Step 2: Make Targeted Repairs and Document Everything

Fixing a flagged issue is only half the job. You need to keep receipts, contractor invoices, and before-and-after photographs. This documentation substantiates that the risk has been reduced when you present it to insurers.

For example:

- If you replace an outdated electrical panel, obtain a compliance certificate from a certified electrician

- If you reroof, save invoices specifying materials and installation date

- If you install an approved water security system, retain proof of purchase and installation

Step 3: Request a Re-Evaluation After Repairs

Many homeowners don't realize they can proactively contact their insurer with updated documentation and request a premium review—you don't have to wait until renewal. Danish insurers consider installed, approved risk-mitigation devices when setting terms, and Bolius advises discussing noted defects with your insurer and correcting them to restore full coverage.

Step 4: Use Inspection Findings as Leverage When Comparing Providers

Different insurers weight the same risk factors differently. A well-maintained home with documented upgrades can qualify for dramatically different rates across providers — so shopping your policy after completing repairs is worth the effort.

An independent comparison tool like Inzure can accelerate this process. Upload your existing policy as a PDF or photo, and the platform benchmarks your coverage and pricing against current market rates across Danish insurers — including Tryg, Topdanmark, Alka, Codan, GF, Alm. Brand, If, and Lærerstandens Brandforsikring — in about 60 seconds. The analysis flags:

- Coverage gaps and overlaps

- Unjustified price increases

- Whether your documented improvements are actually lowering your premium

The analysis is free. Inzure charges a 20% commission on savings only if you switch to a better deal.

Step 5: Ask Specifically About Discounts

Insurers often do not volunteer available discounts for:

- New or upgraded roofs

- Updated electrical panels or rewiring

- Monitored alarm or fire suppression systems

- Claim-free histories

Your inspection report gives you the specific language and evidence needed to ask the right questions. For instance, if you've installed an Alka-approved water security system, explicitly request the corresponding discount on hidden pipe coverage.

Why Existing Homeowners Benefit Just as Much as Buyers

Many homeowners associate inspections exclusively with the home-buying process. In reality, periodic inspections are one of the most overlooked tools for managing insurance costs over time.

Homes Age—And So Do Their Risk Profiles

What passed inspection five years ago may be showing wear today. Roofs deteriorate, electrical panels age, and plumbing materials corrode. An inspection helps you identify maintenance issues before they become insurance liabilities—or before your insurer's own inspection catches them at renewal and triggers a premium increase.

The Loyalty Penalty

Loyal customers with 10+ years of seniority pay on average 7–8 percentage points more than new customers with the same risk, amounting to roughly 1.108 kr. per year across car, house, and home insurance combined, according to KFST. The same analysis found that most consumers do not solicit new quotes or switch within two years, and approximately 80% who negotiate obtain lower prices.

Proactive inspections give you documented proof of your home's condition—exactly the kind of leverage you need to renegotiate with your current insurer or make a compelling case when switching to one that prices well-maintained homes fairly. That documented evidence is what turns a negotiation from a guess into a conversation backed by facts.

Practical Inspection Cadence

Videncentret Bolius recommends practical maintenance checks that double as periodic condition assessments. As a general guide:

- Every 3–5 years for general condition reviews

- After major weather events (storms, heavy rain, flooding)

- Before policy renewal if your home is aging or you suspect deferred maintenance

- After significant renovations to document improvements

Each inspection creates a paper trail. Over time, that trail becomes your strongest argument for lower premiums—whether you stay with your current insurer or move to one that rewards maintenance.

Frequently Asked Questions

What is the biggest red flag in a home inspection?

Major structural issues, significant roof damage, outdated or hazardous electrical systems (such as knob-and-tube wiring), and evidence of water intrusion are the most serious red flags. These signal elevated risk to insurers and are expensive to repair.

Can a home inspection guarantee lower insurance premiums?

A home inspection itself doesn't guarantee lower premiums, but the repairs it prompts can. A clean report with documented improvements gives you concrete leverage to negotiate or shop for better rates.

What types of home improvements lower insurance costs the most?

Roof replacement or upgrade, modernizing electrical panels, updating plumbing, adding storm-resistant features, and installing monitored security or fire suppression systems tend to have the greatest impact. These directly reduce the likelihood and severity of common claims.

How often should homeowners get an inspection to maintain lower insurance rates?

Most homeowners benefit from an inspection every 3–5 years, after major weather events, after significant renovations, and before policy renewal if the home is aging.

Should I fix issues found in an inspection before switching insurance providers?

Fixing major issues first removes risk factors that drive up quotes or trigger coverage exclusions. That said, comparing multiple providers simultaneously still makes sense — some insurers are more lenient than others, even with known issues.