Introduction

If you own a home in a wildfire-prone region, you've likely watched your insurance premiums climb year after year. Many homeowners are now asking a critical question: Is creating defensible space around my property actually worth the investment when it comes to their insurance bill?

The short answer is yes — defensible space can reduce insurance costs. The specifics depend on your insurer, your location, and how well you document your efforts. This guide covers how defensible space affects your premiums, what insurers look for during inspections, and how to document your work to qualify for every available discount.

TLDR:

- Defensible space can lower premiums by 5–20% through wildfire mitigation discounts in high-risk states

- Insurers conduct risk-score assessments and on-site inspections to determine discount eligibility

- Many high-risk jurisdictions mandate minimum clearance distances — check your local requirements before assuming you're compliant

- Documentation (photos, receipts, third-party inspections) is essential to qualify for discounts

- In extreme-risk areas, defensible space may determine whether standard insurers will cover your home at all

What Is Defensible Space and Why Do Insurers Care?

Defensible space is the managed buffer zone around your home designed to slow or stop wildfire spread. It serves two critical functions: protecting the structure from direct flames, radiant heat, and ember ignition, and providing a safe area for firefighters to defend the property.

The Insurer's Risk Calculation

From an underwriting standpoint, a home with no defensible space in a wildfire-prone region represents a near-certain total loss if fire strikes. A home with proper clearance has a significantly lower probability of complete destruction—and this translates directly into lower premiums, better coverage options, or simply the ability to get insured at all.

Insurance eligibility and pricing are increasingly tied to wildfire risk scores, which factor in:

- Proximity to fire stations

- Vegetation density around the property

- Local fire history and ignition patterns

- Whether the property meets defensible space standards

Homes that fail these assessments face limited coverage options or outright policy non-renewal.

Legal Requirements Are Driving Insurance Decisions

Many states have made defensible space legally required within a certain radius of homes in high-risk zones. In California, Public Resources Code Section 4291 mandates 100 feet of defensible space around structures in wildfire-prone areas. Recent updates through Assembly Bill 3074 created an even stricter "ember-resistant zone" within the first 5 feet of the structure.

Insurers now check for compliance during underwriting inspections. Properties that don't meet legal requirements face two outcomes: outright coverage denial or significant premium surcharges. Meeting the legal minimum isn't just about avoiding fines — it's a baseline requirement for staying insurable.

Does Defensible Space Actually Reduce Insurance Costs?

Yes—documented defensible space can lower premiums, unlock mitigation discounts, and in some markets, determine whether a standard insurer will cover your home at all. But the effect is not automatic and varies widely by carrier.

How the Discount Mechanism Works

Insurers in high-wildfire states have begun offering structured wildfire mitigation discounts for homeowners who take verified steps to reduce risk. The discount mechanism works differently depending on the carrier:

- Some insurers apply the discount to your entire homeowner's premium

- Others apply it only to the wildfire risk component of your policy

- The same defensible space upgrade can yield a 5% discount from one insurer and a 15% discount from another

This variability makes comparison shopping essential. What you're paying with one carrier may not reflect the full value of your mitigation work.

Stacking Discounts Through Home Hardening

Defensible space delivers its biggest financial impact when paired with physical home upgrades. Adding ember-resistant vents, fire-rated roofing, and non-combustible siding alongside cleared zones can unlock certifications like the Insurance Institute for Business & Home Safety (IBHS) Wildfire Prepared Home designation.

Properties that achieve these certifications typically qualify for:

- 10-20% premium reductions from participating insurers

- Priority consideration during coverage reviews

- Better access to standard market policies instead of last-resort programs

That said, even a full certification package won't override every underwriting barrier—which is where realistic expectations matter.

Realistic Limits: What Defensible Space Can't Do

Defensible space alone won't automatically get a high-risk property into the standard insurance market if other risk factors remain:

- High fire history in your immediate area

- Remote location with limited fire department access

- Extreme topography (steep slopes, narrow access roads)

- Dense surrounding vegetation beyond your property line

The goal is a stronger negotiating position with insurers—lower premiums, better coverage terms, or both. What it won't do is wipe out an underwriter's concerns about location or fire history.

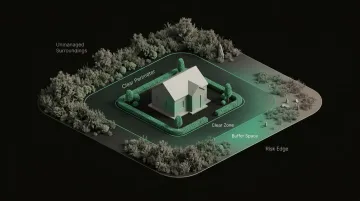

The Three Zones of Defensible Space: What Insurers Look For

When an insurer sends an inspector to your property, they're scoring it against a three-zone framework developed by the NFPA — and each zone has direct bearing on your coverage eligibility and premium. Most state fire agencies use the same structure, so understanding it tells you exactly what inspectors are looking for before they arrive.

Zone 0—The Immediate Zone (0-5 feet from the structure)

Zone 0 is where ember intrusion begins — and where most home ignitions during wildfires actually start. All combustible materials must be removed from the immediate perimeter:

- Replace wood mulch with gravel, pavers, or rock

- Clear all dead leaves, pine needles, and plant debris

- Remove stored firewood (relocate to Zone 2)

- Install gutter guards to prevent debris accumulation

- Clear roof valleys and ridges of all organic matter

- Ensure attic vents have fine metal mesh screens (1/8-inch maximum) to block embers

California's Assembly Bill 3074 made this zone legally mandatory — homeowners must remove any material embers can ignite within 5 feet of the structure. Inspectors treat non-compliance here as an automatic risk flag, regardless of how well the outer zones are maintained.

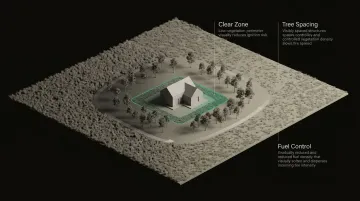

Zone 1—The Intermediate Zone (5-30 feet)

This zone focuses on reducing fuel load and breaking vegetation connectivity:

- Clear all dead plants, dry grasses, and fallen branches

- Space trees so canopy crowns are at least 10 feet from the structure and 18 feet apart from each other

- Remove ladder fuels (low branches that allow fire to climb into the canopy) up to at least 6 feet from the ground

- Trim shrubs to maximum 18-inch height

- Create horizontal and vertical spacing to prevent continuous fuel paths

Zone 1 compliance is often what separates a standard premium from a discounted one — insurers can visually assess tree spacing and fuel load from the street or aerial imagery.

Zone 2 — Beyond 30 Feet: Slowing Fire Before It Arrives

The outer zone won't stop a wildfire, but it reduces the intensity and speed of flames reaching your home — giving firefighters a better chance and giving insurers evidence of managed risk:

- Trim native grasses to 4 inches or lower

- Space trees with at least 12 feet between crowns for those within 30-60 feet of the home

- Space trees with at least 6 feet between crowns for those 60-100 feet from the structure

- Keep outbuildings, fuel tanks, and propane storage clear of flammable vegetation

- Remove dead trees and large accumulations of fallen timber

How to Document Your Defensible Space and Claim Insurance Discounts

Documentation is where most homeowners lose money. Insurers need verifiable proof before applying discounts—verbal confirmation isn't enough.

Build a Strong Documentation File

The strongest file includes:

- Before-and-after photos showing cleared zones from multiple angles

- Dated video walkthroughs of your property perimeter

- Seasonal maintenance logs tracking ongoing clearing work

- Receipts or contractor invoices for materials and services

- Measurements showing compliance with zone spacing requirements

Photos should clearly show the structure, the cleared zones, and distant reference points to demonstrate scale.

The Value of Third-Party Inspections

A third-party inspection report from a certified wildfire mitigation specialist or local fire department gives underwriters more confidence than self-reported documentation. Many insurers will expedite discount approval when you submit an objective assessment.

Check with your local fire department—some agencies offer free defensible space inspections and will provide written confirmation of compliance.

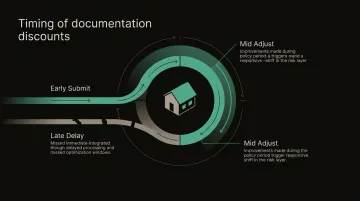

Timing Matters: Submit Documentation Proactively

Submit your documentation 60-90 days before your policy renewal, not when you receive your renewal bill. Insurers need processing time, and late submissions often mean the discount won't appear until the following year.

Mid-term work doesn't have to wait until renewal. If you complete defensible space improvements during an active policy period, contact your insurer immediately to request a premium adjustment — some carriers will apply the discount retroactively.

What Happens If You Don't Have Defensible Space?

Skip defensible space, and your insurance options narrow fast. Common consequences include:

- Higher premiums reflecting increased risk

- Exclusions for wildfire-related damages

- Higher wildfire-specific deductibles (often 5-10% of dwelling coverage)

- Reduced coverage limits on dwelling or contents

- Policy non-renewal forcing you into the last-resort market

The Non-Renewal Crisis in High-Risk Zones

The non-renewal problem has accelerated sharply. Thousands of policies in California, Oregon, and Colorado have been non-renewed as insurers exit high-risk markets. Without standard coverage, homeowners are forced into last-resort programs like the California FAIR Plan.

FAIR Plans provide only basic fire coverage without liability or water damage protection, often at higher cost than standard policies. Homeowners must then layer a Difference in Conditions (DIC) policy on top to fill coverage gaps, driving total costs well above what a standard policy would have cost.

A standard policy might cost $2,500 annually, while a FAIR Plan plus DIC policy for equivalent coverage can exceed $4,500 — nearly double the premium for less protection.

Other Ways to Reduce Home Insurance Costs

Defensible space is just one strategy. These complementary approaches stack with mitigation discounts:

Policy and Coverage Adjustments

- Raise your deductible if your emergency fund allows (can reduce premiums 15-25%)

- Install monitored smoke and security systems (5-15% discount)

- Improve your credit score where insurers are permitted to use it in pricing

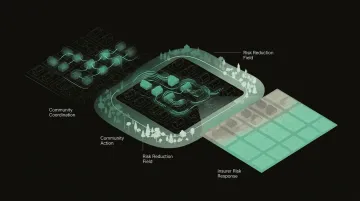

Community-Level Programs

Join a recognized community wildfire safety program like Firewise USA. When an entire neighborhood participates in coordinated brush clearing and home hardening, insurers treat the collective risk more favorably and may offer additional community-level discounts.

Verify You're Getting the Discount You've Earned

Many homeowners complete defensible space improvements and never see their premium drop — not because the insurer won't discount, but because no one asked. After documented improvements, contact your insurer directly and request a policy review. If they can't adjust your rate to reflect reduced risk, comparing quotes from other carriers is a reasonable next step.

Frequently Asked Questions

Does defensible space affect insurance?

Yes, defensible space directly affects both insurance eligibility and premium pricing. Insurers view properties with maintained buffer zones as lower-risk, which can result in 5–20% discounts and better access to standard coverage in wildfire-prone areas.

How can I reduce the cost of my home insurance?

Several steps can lower your premium:

- Create and document defensible space around the property

- Invest in home hardening (fire-rated roof, ember-resistant vents)

- Bundle policies, raise your deductible, and compare carriers to ensure you're getting full credit for risk-reduction efforts

What is the 30-30-30 rule for fires?

The 30-30-30 rule refers to weather conditions that dramatically increase wildfire risk: 30% relative humidity or below, temperatures of 30°C (86°F) or above, and wind speeds of 30 km/h or higher. Under these conditions, fire spreads rapidly and defensible space becomes especially critical.

What is the 80% rule in property insurance?

The 80% rule requires homeowners to insure their property for at least 80% of its full replacement cost to receive full claims payouts. Falling below this threshold means the insurer will only cover a proportional share of any loss, even partial ones.

Is defensible space legally required?

In many high-risk states, yes. California requires 100 feet of clearance in certain zones, with a strict 0–5 foot ember-resistant zone. Meeting or exceeding these standards typically triggers insurer inspections and makes properties eligible for mitigation discounts.