Introduction

Many Danish homeowners invest in a security system for safety reasons but don't realise it can also reduce what they pay for home insurance — yet most never see a single krone in savings because they don't take the right steps afterward.

Those right steps start with understanding how premiums actually work. Home insurance costs can feel like something you can't do much about — but the security measures at your home are one of the few factors you can actively control. Installing an alarm system won't mean lower premiums on its own. Danish insurers have specific requirements, and unless you know what they are, a new alarm system can sit unused as a discount lever.

Below, you'll find what actually determines whether you get a discount, how much you can realistically expect, and how to check whether your current insurer is giving you a fair price in the first place.

Key Takeaways

- Installing a security system can lower home insurance premiums — but only if it meets your insurer's specific requirements

- Discounts typically range from 10–20%, depending on professional monitoring and device types

- Having a system alone is not enough — you must inform your insurer and request the discount directly

- Security discounts can stack with other home improvements, though loyal customers frequently overpay regardless

- A discounted premium is not always the cheapest option — compare the market before renewing

Why Home Insurance Costs More Without a Security System

Insurers price home insurance based on risk — the likelihood that a claim will be filed. Homes without security systems are statistically more attractive targets for burglary and slower to detect hazards like fires or water leaks, which increases the insurer's expected payout. Research shows that homes with no security are seven times more likely to be burglarised than homes with basic security measures in place.

This elevated risk profile builds over time. Without any protective signal, your home sits in a higher risk tier, meaning every premium renewal locks in a higher base rate.

If a theft claim is eventually filed, premiums often increase sharply in subsequent years. Data from Danish insurance forums suggests that filing just two claims within three years can double your annual premium, rising from around 6,807 kr to 13,952 kr, creating a costly cycle that's difficult to escape.

That cycle is where the real cost gap emerges. Many homeowners pay what they're quoted without realising that a modest investment in security could shift them into a lower-risk category and reduce what they owe each year. With 30,825 residential burglaries reported in Denmark in 2025, insurers view unprotected homes as measurably riskier assets and price them accordingly.

What Determines How Much You Save on Home Insurance

The discount you receive for installing a security system is not a flat amount. Danish insurers typically offer between 10% and 20% off your home contents insurance (indboforsikring), but the actual saving depends heavily on several interacting factors.

Monitoring Type: Professional vs. Self-Monitored

Professionally monitored systems — where a 24/7 manned control centre (bemandet vagtcentral) can respond even when you're unreachable — consistently earn higher discounts than self-monitored or DIY setups. Danish insurers require connection to a police-approved alarm centre to qualify for any meaningful discount.

Why insurers reward professional monitoring:

- Guaranteed emergency response regardless of homeowner availability

- Immediate verification and police dispatch

- Lower false alarm rates due to professional filtering

- Reduced total loss from faster incident response

Self-monitored systems that only send SMS or video notifications to you and neighbours do not qualify for discounts with most Danish insurers.

System Comprehensiveness: Single-Device vs. Multi-Layered Protection

Insurers reward systems that cover multiple risk categories, not just burglary. A setup that includes several of these elements signals broader risk reduction:

- Monitored burglar alarms

- Smoke and fire detectors

- Carbon monoxide detectors

- Water leak sensors

- Video surveillance integrated with monitoring

Discounts can also stack. If Forsikring offers 10% for an approved alarm plus an additional 10% for approved window locks — customers who install both protective measures can reach a combined 20% discount.

Insurer-Specific Requirements: Certification Matters

Which system you install matters less than whether your insurer recognises it. Danish insurers typically require:

- AIA-approved installation by a registered installer

- EN 50131 certification (European alarm standard)

- Connection to a Rigspolitiet-approved control centre

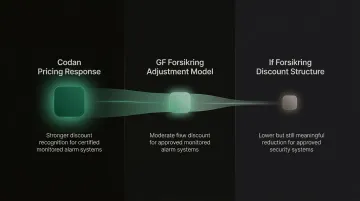

The same security system may earn a 15% discount with one insurer and nothing with another. For example:

| Insurer | Security System Discount |

|---------|--------------------------|

| Codan | 20% for G4S alarm |

| GF Forsikring | 15% for monitored alarm |

| If Forsikring | 10% for approved alarm |

Home and Policy Baseline: The Starting Point Matters

A 10% discount on a high premium saves more than the same 10% on a low one. The absolute savings depend on what you're already paying.

Homeowners already on inflated premiums — a common situation for long-standing customers who have never switched — have the most to gain. A 2025 report by Konkurrence- og Forbrugerstyrelsen confirmed that loyal customers with 10+ years of seniority pay an average of 240 kr more annually than new customers with identical risk profiles.

That gap matters. A 15% security discount on an overpriced baseline may still leave you paying more than a competitor charges with no discount at all — which makes checking your current market price as important as installing the alarm itself.

How to Maximise Your Home Insurance Savings with a Security System

Security discounts do not apply automatically. Getting them requires choosing the right system, telling your insurer about it, and then checking whether your overall premium is actually competitive.

Choosing the Right Security System for Maximum Discount

The first decision that affects your discount is made before installation: selecting a system your insurer will actually recognise.

Verify before you buy:

Contact your insurer and ask specifically whether a system or provider qualifies before committing. Request details about:

- Approved installer requirements

- Required certification standards

- Minimum device types needed

- Whether the monitoring company is recognised

Monitored vs. unmonitored systems:

Professionally monitored systems earn higher discounts because they guarantee a response even when you cannot act. Unmonitored or purely app-based systems earn little or no discount with most Danish insurers.

Device types most likely to qualify:

- Monitored burglar alarms

- Fire and smoke alarms (connected to monitoring)

- Water leak sensors (monitored)

- Video surveillance integrated with monitoring service

A system covering several of these simultaneously tends to earn a higher discount than any single device alone.

Some homeowners invest in smart home gadgets that are not insurance-recognised — technology that adds convenience but earns no premium reduction. Check the insurer's approved device or provider list before purchasing.

Informing Your Insurer — and Verifying the Discount Actually Appears

After installation, contact your insurer, describe the specific system and devices installed, and request a premium review. Discounts do not apply automatically — you need to ask.

Information to have ready:

- Brand and model of the system

- Whether it is professionally monitored (and by which company)

- Monitoring company's details and approval status

- Specific devices installed (alarms, detectors, cameras)

- Installation declaration (installationserklæring) from your AIA-registered installer

How to frame the request:

"I have installed an AIA-approved burglar alarm system with professional monitoring through [company name]. The system includes [list devices]. I would like to request a review of my home insurance premium to apply any available security discount."

Once the insurer confirms a discount, check your renewed premium carefully. Many consumers assume it was handled and never follow up.

Even after receiving a security discount, your insurer's discounted rate may still be higher than what a competitor charges without any discount. That is where comparing against real market rates matters. Inzure analyses your current policy in 60 seconds to show whether you are paying a fair price — not just a reduced price on an already expensive policy.

Stacking Your Savings: Other Factors That Lower Your Premium

Security systems are one of several home characteristics that affect insurance pricing. Other factors that often reduce premiums include:

- Physical security improvements: Deadbolt locks, window locks, reinforced doors

- Fire safety upgrades: Modern smoke detectors, fire extinguishers

- Home maintenance: New roof, updated electrical and plumbing systems

- Location factors: Proximity to fire services, low-crime neighbourhood

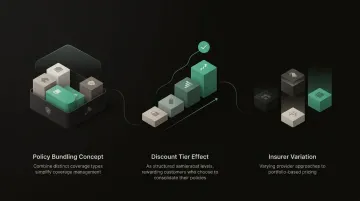

Bundling multiple improvements:

Homeowners who combine protective improvements — a security system, upgraded locks, new roof, monitored smoke and water detectors — can stack discounts and achieve a larger total reduction than any single factor alone.

Bundling policies (samlerabat):

Many insurers offer additional discounts when you combine multiple insurance policies:

| Insurer | Bundling Discount |

|---|---|

| Topdanmark + Norlys | Up to 15% |

| GF Forsikring | 10% for 3+ policies |

| If Forsikring | Up to 15% |

Stacking discounts is most effective when the base premium is competitive. Loyal customers who have stayed with the same insurer for years are far more likely to be paying above-market rates — meaning their stacked discounts may still leave them overpaying compared to switching or renegotiating.

Conclusion

A security system can lower home insurance costs, but the savings are not automatic. They depend on choosing a system your insurer recognises, notifying your insurer promptly, and verifying the discount has been applied correctly. Getting the discount applied is step one — keeping your overall premium competitive is what comes next.

That next step is ongoing. Once a discount is applied, it's worth checking periodically whether your overall premium still reflects what the market actually charges — because a 10% discount on an overpriced policy can still mean you're overpaying.

That's where Inzure's independent AI-powered analysis is useful. Upload your policy in 60 seconds and see what Danish insurers are actually charging for equivalent coverage — so you can judge whether your current deal holds up, discounts included.

Frequently Asked Questions

How much will a security system lower my homeowners insurance?

Discounts typically range from 10–20% depending on the insurer and the type of system installed, with professionally monitored systems earning higher reductions. The actual savings depend on your current premium: a 15% discount on 8.000 kr. saves more than 15% on 4.000 kr.

What are 5 ways to reduce homeowners insurance costs?

The five most impactful methods:

- Install a professionally monitored security system

- Improve the home's physical condition (new roof, upgraded locks)

- Bundle multiple policies with one insurer

- Increase your deductible (selvrisiko)

- Compare rates across insurers to ensure your base price is competitive, not just discounted

What security system do burglars hate?

Research shows burglars most strongly avoid homes with visible alarm systems and professional monitoring, as these create both a deterrent and a guaranteed emergency response. Combining window/door locks with external lights provides protection 20 times greater than having no security. Loud audible alarms combined with exterior cameras and signage are the most effective deterrents.

Does a DIY security system qualify for a home insurance discount?

It depends on the insurer. Some recognise self-installed systems if they include professional monitoring through an approved control centre, while others require certified installation by an AIA-registered installer. Always verify with your insurer before purchasing, and be prepared to provide an installation declaration to qualify for the discount.

Do I need professional monitoring to get a discount on home insurance?

Most Danish insurers require or strongly prefer professionally monitored systems connected to a 24/7 manned control centre for any significant discount. Self-monitored systems that only send notifications to your phone may qualify for a smaller reduction or none at all, depending on the provider.

How do I claim a security system discount on my home insurance?

You must contact your insurer after installation, provide details about the system (brand, devices, monitoring service), and explicitly request a premium review. Bring your installation declaration from your AIA-registered installer as proof. The discount is rarely applied automatically, so confirm it appears on your next renewal notice.