Introduction

Flooding is financially catastrophic: FEMA estimates that just one inch of floodwater causes roughly 175.000 DKK in damage to a home, yet the average flood insurance premium hovers around ca. 6.545 DKK annually. For homeowners in high-risk zones with federally backed mortgages, flood insurance isn't optional — and premiums can feel both unavoidable and unchangeable.

Most policyholders accept whatever rate they're quoted without realizing several powerful levers exist to reduce costs. Under FEMA's Risk Rating 2.0 system, premiums increase annually — currently capped at 18% per year — until they reach the property's full actuarial risk rate. For many homeowners, that means a median jump from ca. 4.823 DKK to ca. 9.016 DKK.

That trajectory won't reverse on its own. This guide breaks down where flood insurance costs come from, what keeps pushing them higher, and the concrete strategies you can use to reduce premiums without reducing coverage.

Key Takeaways

- Flood insurance costs stem from property-level risk factors, coverage decisions, and program-level pricing—not all of which are fixed

- Physical mitigation upgrades like elevated utilities, flood vents, and structural elevation reduce how insurers rate your property's risk

- Raise your deductible, obtain an Elevation Certificate, and compare state-backed vs. private flood insurers — these decisions at purchase or renewal carry the highest savings potential

- Your community's participation in FEMA's Community Rating System can reduce premiums by 5–45%, yet most homeowners never verify their community's rating status

- Review your flood policy every year — one-time shopping misses rate changes, new mitigation credits, and coverage gaps that compound over time

How Flood Insurance Costs Typically Build Up

Flood insurance expenses don't appear as a single visible line item that stays constant. Premiums typically start at a base rate, then increase annually — sometimes compounding year after year. As insurers recalibrate risk models, properties gradually move toward their full risk-adjusted rate — which can far exceed what a policyholder currently pays.

Many flood policies carry annual increase limits for primary residences, with secondary properties and high-risk homes facing steeper hikes. These caps prevent immediate sticker shock. What they don't prevent is steady, compounding growth until you reach the insurer's full risk rate.

Even within those annual caps, the baseline rate itself can be inflated — and that's a separate problem entirely. Costs become harder to manage when homeowners don't realize their property is being rated on outdated assumptions. Three common culprits include:

- Outdated flood maps that no longer reflect your property's actual risk zone

- Unrecorded mitigation improvements your insurer hasn't accounted for in your rating

- Incorrect elevation data that places your property at higher risk than it is

Insurers default to the information on file. If that information is wrong, you pay for it.

Key Cost Drivers for Flood Insurance

Flood insurance pricing depends on several primary factors:

Fixed Property Characteristics:

- Property location and flood zone designation

- Distance to water sources (coasts, rivers, lakes)

- Elevation of the structure relative to your insurer's flood level benchmarks

- Foundation type (slab, crawlspace, basement, elevated)

- Building replacement cost value

Policyholder Decisions:

- How much building and contents coverage is purchased

- What deductible level is selected

- Whether key documentation (like an Elevation Certificate) has been submitted

The flood insurance market itself shapes costs just as much as the property details above. Public flood insurance schemes and private insurers use different pricing methods, set different coverage limits, and respond differently when you've made flood mitigation improvements. Most people don't realize they can choose between the two — or that this choice can dramatically impact annual costs.

Cost-Reduction Strategies for Flood Insurance

Flood insurance cost reduction isn't about finding one magic fix—it depends on which cost drivers are most relevant to your property. Different strategies deliver different results depending on whether the issue is property risk, policy decisions, or ongoing management.

Strategies That Reduce Costs by Changing Decisions

These approaches deliver the most impact at the point of purchase or renewal—before a policy is locked in for the year.

Compare NFIP and Private Flood Insurance

The NFIP is not your only option. Private flood insurers have grown more competitive and can offer lower premiums for many property types. A Milliman feasibility study found that 77% of Florida single-family homes could pay less with private policies than with NFIP coverage—often saving 20-40% annually.

Key differences include:

- Coverage limits: NFIP caps building coverage at 1.750.000 DKK and contents at 700.000 DKK, while private insurers often offer 14 millioner DKK+ building and 7 millioner DKK+ contents coverage

- Waiting periods: NFIP requires 30 days; private carriers range from 0-14 days

- Loss of use coverage: NFIP excludes this; private policies frequently include it

- Pricing models: NFIP uses federal Risk Rating 2.0; private insurers use proprietary catastrophe modeling

The catch: 14% of Florida homes in the same study would pay over twice as much in the private market. Private insurers tend to avoid severe repetitive loss properties, leaving the NFIP as the insurer of last resort for the highest-risk homes.

Since July 1, 2019, federal regulations require lenders to accept private flood insurance policies that meet the statutory definition under the Biggert-Waters Act, making it easier to satisfy mortgage requirements with private coverage.

Opt for a Higher Deductible Strategically

Increasing your flood insurance deductible lowers annual premiums—sometimes by 40% or more. The South Carolina Department of Insurance notes that raising the deductible to the 70.000 DKK maximum can reduce premiums by up to 40%.

How it works:

- NFIP allows separate deductibles for building and contents, each up to 70.000 DKK

- Higher deductibles mean you assume more out-of-pocket risk during a flood event

- The insurer reduces your premium because they're covering less of the initial loss

Break-even considerations:

| Baseline Premium | Annual Savings (40%) | Years to Break Even (at 63.000 DKK increase) |

|---|---|---|

| 7.000 DKK | 2.800 DKK | 22.5 years |

| 10.500 DKK | 4.200 DKK | 15.0 years |

| 17.500 DKK | 7.000 DKK | 9.0 years |

This strategy is only appropriate for homeowners with adequate financial reserves to cover the 70.000 DKK out-of-pocket exposure. Some mortgage lenders may not permit deductibles this high.

Provide an Elevation Certificate

An Elevation Certificate (EC) is a licensed surveyor's document showing your property's elevation relative to the BFE. Under Risk Rating 2.0, ECs are no longer mandatory, but can still be submitted voluntarily to lower premiums.

How it works: FEMA uses default elevation assumptions (often conservative) unless you provide better data. If your EC shows your First Floor Height is higher than FEMA's estimate, the rating engine will use your data and return a lower premium. Providing an EC will never increase your premium—FEMA compares the data and uses whichever yields the lowest rate.

Costs and returns:

- Typical surveyor fees: 3.500-14.000 DKK

- Potential discount: Properties elevated 3 feet above grade can receive 22.1% discounts compared to properties at 0 feet

When to invest: ECs are most valuable for homes on crawlspaces or elevated foundations where the lowest floor is visibly higher than adjacent ground. If your property meets this description, the upfront surveyor cost can pay for itself within 1-3 years.

Calibrate Coverage Amounts Accurately

Over-insuring is a common way homeowners overpay without realizing it. Purchasing more building coverage than the actual replacement cost, or contents coverage exceeding the value of your possessions, inflates premiums unnecessarily.

Key considerations:

- NFIP building coverage is capped at 1.750.000 DKK (private insurers offer higher limits)

- Contents coverage is a separate decision and should match actual risk exposure

- Contents coverage pays out at Actual Cash Value (depreciated), not replacement cost

- Loss of use and temporary living expenses are not covered by NFIP

Review your coverage amounts annually. If your building's replacement cost is 1.260.000 DKK, purchasing 1.750.000 DKK in coverage means you're paying for 490.000 DKK in protection you don't need.

Strategies That Reduce Costs by Changing How Coverage Is Managed

These approaches focus on reducing cost through visibility and control while the policy is active—not just at purchase.

Review Your Policy Annually Instead of Auto-Renewing

Loyalty to a single insurer or passively accepting a renewal quote is one of the most common ways flood insurance costs creep upward. Market conditions, private insurer offerings, and community CRS status can all change year-to-year, making annual comparison a high-value habit.

Why this matters:

- Private insurers enter and exit markets, creating new opportunities

- Your community's CRS rating may improve, unlocking automatic discounts

- Risk Rating 2.0 adjustments may make alternative coverage more competitive

US homeowners can compare options by contacting agents directly or using carrier websites. Set a calendar reminder 60 days before renewal to evaluate alternatives before your current policy locks in.

Document and Report All Mitigation Improvements to Your Insurer

Physical improvements to your property—elevated utilities, installed flood vents, structural changes—can qualify for lower rates, but only if they are documented and formally submitted.

Critical documentation includes:

- Contractor receipts and invoices

- Photos of completed work (before and after)

- Building permits and final inspections

- Engineer certifications for structural changes

Keep records of all mitigation work in a dedicated file. At renewal, submit this documentation to your insurer along with a formal request for a premium adjustment. Insurers cannot adjust your rate based on improvements they don't know about.

Verify Your Community's CRS Participation and Discount Status

If your community participates in FEMA's Community Rating System, NFIP policyholders receive automatic discounts of 5-45% depending on the community's classification. Over 1,500 communities participate nationwide, covering roughly 76% of the entire NFIP policyholder base.

How to check:

- Visit FEMA's Community Status Book online

- Call your insurance agent and ask for your community's CRS class

- Contact your municipal floodplain manager

Under Risk Rating 2.0, CRS discounts apply uniformly to all eligible policies in the community, regardless of whether the structure is inside or outside the Special Flood Hazard Area. Many homeowners don't know to check this, meaning they may be missing discounts that should already be applied—or could be if community officials take action.

Strategies That Reduce Costs by Changing the Context Around the Property

These approaches acknowledge that sometimes the premium is high because of the surrounding risk environment—and that environment can be influenced, both at the individual property level and through community action.

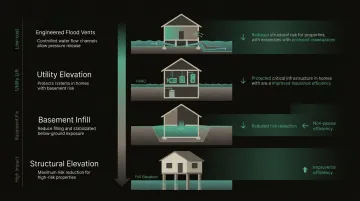

Invest in Physical Flood Mitigation Upgrades

Structural modifications reduce the physical risk your property poses to insurers, which directly translates to lower premiums:

High-impact mitigation measures:

| Mitigation Measure | Typical Cost | Premium Impact | Best Application |

|---|---|---|---|

| Engineered Flood Vents | 42.000-70.000 DKK | Moderate (removes enclosure penalty) | Homes with crawlspaces/enclosures |

| Elevating Utilities (HVAC, water heaters) | 42.000-70.000 DKK | Moderate (removes basement/subgrade penalty) | Homes with basement utilities |

| Basement Infill | 217.000-812.000 DKK | High (changes foundation rating) | High-risk homes with unused basements |

| Structural Elevation | 840.000-1.820.000 DKK | Extreme (e.g., 73.500 DKK down to 4.200 DKK) | Severe repetitive loss properties |

The RAND NYC case study: A 2017 RAND Corporation analysis found that elevating a structure 2 feet above the BFE could drop an average annual premium from 73.500 DKK to just 4.200 DKK. However, the upfront cost averaged 1.190.000 DKK, making this practical only for properties with severe repetitive losses or when grant funding is available.

Grant opportunities: FEMA's Hazard Mitigation Assistance programs, including Flood Mitigation Assistance (FMA) and Building Resilient Infrastructure and Communities (BRIC), can fund projects like installing flood openings or elevating buildings. These grants are administered through states and communities and can substantially offset homeowner costs.

Request a Flood Map Review if Your Zone Designation Appears Incorrect

FEMA's flood zone maps are periodically updated but can contain errors or lag behind infrastructure changes. Homeowners who believe their property has been incorrectly mapped into a higher-risk zone can request a Letter of Map Amendment (LOMA) or Letter of Map Revision (LOMR).

LOMA vs. LOMR:

- LOMA: Used when a structure is on naturally high ground (not elevated by fill) and should not be in a Special Flood Hazard Area

- LOMR-F: Used when a structure has been elevated by earthen fill to be at or above the BFE

The LOMA process:

- File the MT-EZ form with elevation data certified by a Licensed Land Surveyor

- No FEMA review fee for LOMA requests (LOMR-F costs 2.975-3.675 DKK)

- FEMA normally completes review within 60 days

- If approved, the LOMA officially removes the property from the SFHA, eliminating the federal flood insurance purchase requirement

Important caveat: Even if you receive a LOMA, maintaining flood coverage is highly recommended—over 25% of flood claims occur outside designated high-risk zones.

Encourage Community-Level Flood Resilience Investment

Individual homeowners can advocate for (and benefit from) their municipality enrolling in or improving its CRS rating. Communities that invest in open space preservation, floodplain management, and public education earn CRS credits that translate directly into policyholder discounts.

How to advocate:

- Attend local planning and zoning meetings

- Contact your municipal floodplain manager

- Request information about your community's current CRS status

- Encourage officials to pursue higher CRS classifications

A community moving from no CRS participation to even a basic Class 9 rating unlocks a 5% discount for all NFIP policyholders in the area. Moving from Class 9 to Class 8 increases the discount to 10%. These percentage discounts compound with individual mitigation efforts.

Conclusion

Flood insurance cost is not fixed—it shifts based on decisions made at purchase, how actively the policy is managed, and whether the property's physical risk profile has been addressed. Homeowners who treat flood insurance as a "set and forget" expense consistently overpay, particularly as insurers move premiums closer to actuarial full risk over time.

Take a layered approach to cost reduction:

Quick wins to start with:

- Check your current deductible level and calculate break-even points for increasing it

- Confirm any available insurer discounts are correctly applied to your policy

- Review your policy annually before auto-renewing, comparing multiple insurer options

Longer-term actions worth pursuing:

- Get a professional property risk assessment if your home sits in a lower-risk position than your current rating reflects

- Document all mitigation improvements and submit them to your insurer

- Pursue physical upgrades like elevated utilities or flood vents when financially feasible

Insurers won't flag that you're overpaying or that a better policy exists. That information only surfaces when you actively look for it. Even applying two or three of these strategies can meaningfully cut your annual premium while keeping your coverage intact.

Frequently Asked Questions

How to reduce the cost of flood insurance?

The highest-impact levers are:

- Physical mitigation: elevated utilities, flood vents, structural elevation

- Higher deductibles (up to 70.000 DKK can cut premiums by 40%)

- An Elevation Certificate to override FEMA's default risk assumptions

- Community CRS discount status (5–45% automatic savings)

- Annual comparison between NFIP and private insurer options

Why does my flood insurance keep going up every year?

FEMA's Risk Rating 2.0 shifted flood insurance from subsidized rates to full actuarial pricing. Federal law caps annual increases at 18% for most primary residences, so premiums climb incrementally each year until your property reaches its full risk-adjusted rate — a process that can take years to complete.

Does the federal government offer flood insurance?

Yes, the federal government offers flood insurance through FEMA's National Flood Insurance Program (NFIP), which is available through private insurance companies acting as intermediaries (Write Your Own insurers). However, private flood insurance is also an option, and since July 2019, federally regulated lenders must accept private policies that meet statutory requirements.

What is happening with the National Flood Insurance Program?

FEMA implemented Risk Rating 2.0 in April 2022, replacing flood zone maps with individual property risk factors — distance to water, flood frequency, replacement cost, and building characteristics. The result is more accurate premiums, with some policyholders seeing reductions and others facing gradual increases toward their full risk rate.

What is the 100 year flood rule?

The "100-year flood" refers to a flood with a 1% chance of occurring in any given year (also called the base flood). Properties in 100-year floodplains (Special Flood Hazard Areas) are typically required to carry flood insurance if they have federally backed mortgages. Over a 30-year mortgage, a property in this zone has a 26% chance of experiencing flood damage.

What is the 50% rule in FEMA?

The FEMA 50% rule (Substantial Improvement rule) requires that if a structure in a flood zone is improved or repaired to 50% or more of its market value, it must be brought up to current floodplain management standards—often requiring full structural elevation to or above the Base Flood Elevation. This rule significantly affects renovation decisions and can impact long-term insurance costs.