Introduction

Many Danish households operate under a costly misconception: that buying higher insurance coverage (forsikringssum) will somehow earn them a discount or reward them with lower monthly premiums. This is the exact reverse of how insurance pricing actually works. The confusion often stems from mixing up two distinct policy variables — coverage limits and deductibles (selvrisiko) — and misunderstanding which lever actually moves premium costs in which direction.

The real-world consequences are significant. Some consumers lower their coverage limits trying to save money, exposing themselves to catastrophic financial risk if a large claim occurs. Others raise deductibles they can't actually afford, leaving them unable to file claims when they need to most.

Below, we break down how limits and deductibles actually work, why confusing them is an expensive mistake, and which strategies genuinely reduce your premiums without leaving you underinsured.

Key Takeaways

- Higher coverage limits increase your premium, not reduce it

- Higher deductibles reduce your premium by sharing more risk with you

- Exception: higher liability limits can sometimes improve renewal pricing indirectly

- Compare market rates annually to avoid the loyalty penalty

- Switching insurers delivers the biggest real-world savings

- Danish customers overpay by an average of 240–445 kr/year simply for staying with the same insurer

Insurance Limits vs. Deductibles: Two Terms People Mix Up

Defining Forsikringssum and Selvrisiko

In the Danish insurance market, the insurance limit (forsikringssum or dækningssum) is the absolute maximum your insurer will pay on a covered claim. If your home contents policy (indboforsikring) carries a limit of 800,000 kr and a fire destroys everything you own, the insurer pays no more than that amount, regardless of your actual loss.

The deductible (selvrisiko) works differently: it's the fixed amount you pay out of pocket before coverage kicks in. With a 3,000 kr deductible on a 10,000 kr claim, you cover the first 3,000 kr and the insurer pays the remaining 7,000 kr.

These two variables move premiums in opposite directions:

- Higher limits = higher premiums (insurer takes on more risk)

- Higher deductibles = lower premiums (you take on more risk)

Mix them up, and you'll misread your policy — and potentially your bill.

Where Each Variable Applies

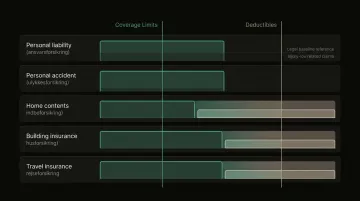

Not every coverage type uses both variables. Here's how they split across common Danish policies:

| Coverage Type | Has Limit? | Has Deductible? |

|---|---|---|

| Personal liability (ansvarsforsikring) | ✓ (statutory 10 million kr for injury) | — |

| Personal accident (ulykkesforsikring) | ✓ (fixed invalidity sum) | — |

| Home contents (indboforsikring) | ✓ | ✓ |

| Building insurance (husforsikring) | ✓ | ✓ |

| Travel insurance (rejseforsikring) | ✓ | ✓ |

Knowing which lever applies to your specific coverage tells you exactly which number to adjust — and which one won't move the needle on your premium.

Do Higher Insurance Limits Lower Your Premiums? The Direct Answer

The Simple Reality: No — Higher Limits Raise Premiums

Higher coverage limits do not reduce your premium. They strictly increase it. When you raise your forsikringssum, you are asking the insurer to assume greater financial exposure, and they price that additional risk directly into your monthly or annual cost.

Concrete example:

- Bodily injury liability at 250,000 kr per accident: Base premium

- Bodily injury liability at 1,000,000 kr per accident: Base premium + 8-12% increase

- Bodily injury liability at 5,000,000 kr per accident: Base premium + 18-25% increase

The increase exists because the insurer must reserve capital and price for the possibility that a claim could reach those higher amounts.

Why the Cost Increase Is Often Smaller Than Expected

The premium jump from minimum to mid-range limits is often smaller than consumers expect. Insurers price the probability of a claim reaching those higher amounts — and statistically, large claims are rare. A claim exceeding 250,000 kr is uncommon; one exceeding 5,000,000 kr is exceptional.

In practice, that looks like this:

- 250,000 kr → 500,000 kr: roughly 150 kr extra per year

- 500,000 kr → 1,000,000 kr: roughly 100 kr more on top of that

Doubling your coverage for 250 kr annually is rarely a bad trade.

Why Cutting Your Coverage Limits to Save Money Backfires

Faced with rising premiums, some consumers lower their coverage limits to reduce costs. The risk is significant: if a claim exceeds your limit, you are personally liable for the difference — meaning your savings, assets, and future income can all be pursued to cover the shortfall.

Claims inflation has significantly outpaced general consumer inflation from 2020 to 2022, driven by construction and repair costs. What seemed like adequate coverage five years ago may now leave you underinsured. Medical costs and property damage expenses have risen sharply — even routine accidents can generate unexpectedly high liability claims.

The Correct Mental Model

Insurance limits are financial protection against worst-case scenarios. They are not a pricing lever you adjust month to month to trim costs. Your liability limits should match or exceed your net worth — that is the threshold that actually protects what you own.

The right question is never "how low can I go?" It is "am I covered for what a serious claim could actually cost?"

How Higher Deductibles DO Reduce Your Premiums

The Inverse Relationship That Actually Works

When you agree to pay more out of pocket in the event of a claim (higher deductible), the insurer's maximum liability per claim effectively drops. You are sharing more of the risk, so they charge you less for the coverage.

Typical savings potential in Denmark:

- Raising deductible from 1,000 kr to 3,000 kr: 12-18% annual premium reduction

- Raising deductible from 3,000 kr to 5,000 kr: Additional 8-12% reduction

These percentages vary significantly by insurer and coverage type, but the direction is consistent: higher deductibles directly reduce what you pay.

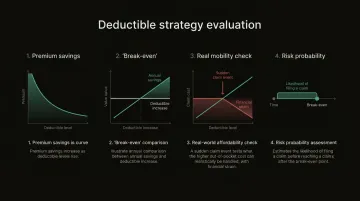

The Break-Even Calculation You Should Run

The Danish Consumer Council recommends a straightforward calculation: if raising your deductible by 2,000 kr saves you 500 kr annually, you must go more than four years without a claim for the decision to be profitable.

Step-by-step:

- Calculate annual premium savings from raising the deductible

- Divide the deductible increase by the annual savings = break-even period in years

- Ask: Can I afford the higher out-of-pocket cost if a claim occurs tomorrow?

- Ask: How likely am I to file a claim in the break-even period?

When a High Deductible Makes Sense

Once you know your break-even period, the decision comes down to your financial cushion and your risk profile.

Go higher if:

- You have a solid emergency fund (3-6 months of expenses)

- You have a clean claims history

- You're a low-risk homeowner or renter

- You prefer to self-insure small losses and save on premiums

Stay lower if:

- Cash flow is tight and you can't absorb a 5,000 kr surprise expense

- You live in a high-risk area (flood-prone, high crime)

- Your property insurer has specific deductible requirements tied to your coverage tier

The Lender Constraint

If you have a mortgage on your home, your lender may impose a maximum deductible to protect their collateral. Danish mortgage lenders require fire insurance and use panthaverdeklarationer (mortgagee clauses) to monitor coverage terms. This means you may not have full freedom to raise your home insurance deductible as a cost-saving tool.

The One Scenario Where Higher Limits Can Work in Your Favor

The Indirect Pricing Benefit

While higher limits don't directly reduce premiums, there is one scenario where they can work in your favor: insurers view policyholders who consistently carry higher liability limits as lower-risk and more financially responsible. At renewal time or when switching providers, having a track record of higher limits can result in more favorable pricing offers or preferential underwriting treatment.

Think of it as a longer-term positioning benefit, not a guaranteed short-term discount.

The Uninsured/Underinsured Motorist Coverage Link

Your uninsured/underinsured motorist (UM/UIM) coverage can typically only be set as high as your liability limits. By carrying higher liability coverage, you can also carry higher UM/UIM protection if an at-fault driver can't cover your damages.

This creates an indirect benefit: higher liability limits give you access to better protection for your own injuries and damages in scenarios where the at-fault party cannot pay.

Keep It in Perspective

Do not use higher limits as a strategy to reduce premiums. Use them because the protection level is appropriate for your assets and risk exposure.

Consider what's actually at stake:

- Asset exposure: If you have 2,000,000 kr in net worth, carrying only 500,000 kr in liability leaves 1,500,000 kr vulnerable to a judgment

- False economy: The premium difference between coverage tiers is often modest — the catastrophic downside is not

- Right-sizing coverage: Match your limits to your actual net worth and risk profile, not to the minimum required

What Actually Reduces Your Insurance Premium

The Real Premium-Lowering Levers

Five levers reliably reduce what you pay without cutting what you're covered for:

- Raise your deductible — the most direct way to lower premiums while keeping coverage limits intact

- Bundle home, travel, and accident policies with one insurer for 10-20% multi-policy discounts

- Maintain a claims-free record; no-claims bonuses compound year over year

- Complete safety or telematics programs offered by your insurer (home security, safe driving)

- Compare the market annually — most Danes who skip this step are quietly overpaying

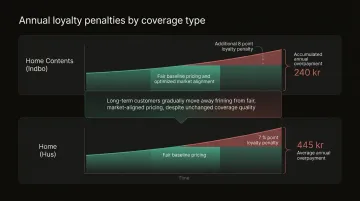

The Loyalty Trap: How Loyal Customers Overpay

Research from the Danish Competition and Consumer Authority reveals a systematic pattern: loyal customers with 10+ years of seniority pay significantly higher margins than new customers.

Annual loyalty penalty by coverage type:

| Insurance Type | Margin Increase | Average Overpayment |

|---|---|---|

| Home Contents (Indbo) | +8 percentage points | 240 kr/year |

| Home (Hus) | +7 percentage points | 445 kr/year |

Insurers use "price walking" to gradually increase premiums for existing customers in line with wage indices, while offering discounted introductory rates to attract new customers. If you auto-renew year after year without comparing, you are likely paying a loyalty premium of hundreds of kroner annually.

Remove Coverage Duplicates

Many Danish households unknowingly pay for the same coverage twice:

- Roadside assistance included in both car insurance and home contents

- Travel insurance through both a credit card benefit and a standalone policy

- Legal aid (retshjælp) duplicated across multiple policies

While the industry has administrative agreements to handle overlapping claims, you still pay two premiums for the same protection. Identifying and removing duplicates cuts costs without sacrificing coverage.

How Inzure Automates This Entire Process

Inzure's AI platform does this analysis automatically. Upload your policies (PDF or photo) from any Danish insurer, and the platform scans all your coverage in 60 seconds — identifying gaps, duplicate policies, and your real market rate before your next renewal.

The platform compares your coverage, prices, and terms against the full Danish market — including Tryg, Alka, and Topdanmark. Using Inzure is free; a 20% fee on annual savings only applies if you choose to switch to a better deal. Find better coverage at the same price, or no better option at all? You pay nothing.

Getting the full picture — what you hold, what it costs, and what the market offers — is the only reliable way to cut premiums without cutting protection.

Frequently Asked Questions

How can I reduce my insurance price?

Compare market rates annually instead of auto-renewing, raise your deductible if your finances allow, remove duplicate coverages across policies, and bundle multiple insurance types with one provider. The single biggest opportunity is avoiding the loyalty penalty by comparing offers.

What is the difference between an insurance limit and a deductible?

A limit is the maximum your insurer pays out on a claim; a deductible is what you pay first before the insurer steps in. They affect premiums in opposite ways: higher limits increase premiums, higher deductibles reduce premiums.

Do higher coverage limits always mean better protection?

Higher limits mean better protection against large claims but come with higher premiums. The right limit depends on your assets — ideally your liability limits should match or exceed your net worth to fully protect what you own.

Is it worth paying more for higher liability limits?

Often yes, especially for liability coverage, because the premium difference between minimum and mid-to-high limits is smaller than most people expect, while the financial protection gap is significant given rising medical and repair costs.

How much can a higher deductible save on my premium?

Savings vary by insurer and coverage type, but increasing your deductible from 1,000 kr to 3,000 kr can reduce your premium by 12–18%, with additional savings possible at higher deductible levels.