In Denmark, approximately 37 accidents happen every day — that's 13,459 police-registered traffic accidents in 2024 alone. Each one represents both a safety risk and a financial liability that affects not only repair costs but also long-term insurance premiums. The good news? Most accidents are preventable, and the same habits that keep you safe also keep your insurance rates low.

This article covers 10 practical ways to achieve both objectives at once — from behind-the-wheel behaviours that reduce crash risk to smarter policy decisions that unlock hidden savings.

Key Takeaways

- Safe driving habits — following distance, no distractions — directly reduce your claims history and lower your premium

- In Denmark, telematics programmes like Tryg Drive offer up to 30% discounts for demonstrating safe driving through app-based scoring

- Raising your deductible or claiming unapplied discounts can cut premiums without reducing your actual protection

- Long-term customers in Denmark pay an average of 1,108 DKK more per year than new customers for identical coverage — comparing annually prevents overpaying

- Platforms like Inzure analyse your existing policies in 60 seconds to surface savings you would otherwise miss

Driving Habits That Prevent Accidents and Lower Your Premiums

Your driving record is your financial report card in the eyes of insurers. Every at-fault accident, speeding ticket, or moving violation becomes part of your claims history — the single most important factor in calculating your premium. Insurers in Denmark share claims data through the EDI platform with your consent, meaning one mistake can follow you across multiple carriers.

The impact is long-lasting: causing an accident typically raises your excess and insurance cost, and those violations stay on your record for years. Conversely, a clean record qualifies you for discounts and lower base rates. The connection is direct — safer driving behaviour results in fewer claims, which signals to insurers that you're a lower-risk customer.

Eliminate Distractions Behind the Wheel

Distracted driving remains one of the leading causes of accidents worldwide. Inattention was a contributing factor in 29% of Denmark's fatal crashes in 2022, making it a leading preventable cause of fatal crashes on Danish roads.

The "2-second rule" explains why: tasks that involve looking away from the roadway for more than 2 seconds are highly dangerous. Using a handheld mobile phone increases crash risk by 3.6 times, whilst texting increases it by 6.1 times and dialling by 12.2 times.

Eliminating distractions is the easiest behavioural change a driver can make:

- Put your phone in silent mode or a glove compartment before starting the car

- Set navigation and music before driving, not during

- Avoid eating, drinking, or grooming whilst behind the wheel

- Pull over safely if you need to handle something that requires your attention

Each of these removes a variable your insurer would otherwise hold against you.

Practise Defensive Driving Techniques

Defensive driving means anticipating hazards before they become emergencies. The goal is to spot risk early enough that you never have to react suddenly.

Core defensive driving habits include:

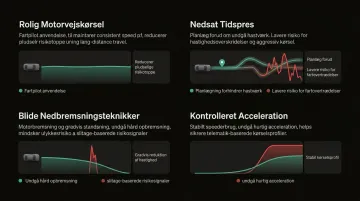

- Maintain safe following distance — Use the 3-second rule: pick a fixed point ahead, and ensure at least 3 seconds pass between when the car ahead passes it and when you do

- Check blind spots before every lane change — Mirrors don't show everything; a quick shoulder check prevents sideswipe collisions

- Anticipate other drivers' actions — Watch for turn signals, brake lights, and erratic behaviour; assume others may make mistakes

- Adjust speed for conditions — Rain, fog, and ice change stopping distances dramatically; posted limits assume ideal conditions

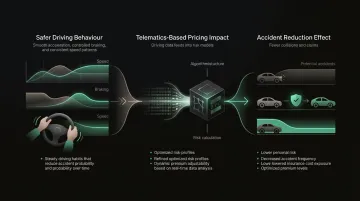

In Denmark, formal defensive driving courses are less common for universal insurance discounts compared to telematics programmes. However, Tryg Drive offers up to 30% premium discounts based on a driving score tracked through an app. The app monitors acceleration, braking, cornering, and speed, rewarding drivers who demonstrate consistent safe behaviour.

If your insurer offers a telematics programme, enrolling formalises these defensive habits and directly reduces your premium.

Obey Speed Limits and Avoid Aggressive Driving

Speeding and aggressive driving (tailgating, hard braking, rapid acceleration) are high-risk behaviours that insurers increasingly track through telematics and usage-based programmes.

According to the Nilsson Power Model, a 1% increase in mean speed produces a 4% increase in fatal crash risk, a 3% increase in severe injury accidents, and a 2% increase in injury accidents. The relationship is exponential, not linear, meaning small speed increases carry disproportionately large consequences.

Aggressive driving amplifies the risk further. Tailgating cuts reaction time, hard braking invites rear-end collisions, and rapid acceleration reduces vehicle control. All three are red flags for telematics programmes, which penalise these behaviours with higher premiums or disqualification from discount tiers.

To avoid these penalties:

- Set cruise control on motorways to maintain steady speed

- Leave earlier to reduce time pressure and the temptation to speed

- Use engine braking and gradual deceleration instead of hard stops

- Maintain consistent throttle pressure to avoid rapid acceleration spikes

Telematics programmes score exactly these behaviours, so smooth and predictable driving translates directly into documented premium savings.

Smart Policy Moves That Cut Your Premium

Even the safest driver can overpay for insurance if they're not actively managing their policy. You can't control other drivers, but you can control what you pay.

Increase Your Deductible Strategically

A deductible (selvrisiko in Danish) is the amount you pay out-of-pocket before your insurance coverage kicks in. The higher the deductible you choose, the lower your premium, because you're assuming more financial risk in the event of a claim.

This strategy works best for drivers with a clean record who rarely file claims. If you haven't made a claim in years, raising your deductible from 2,000 DKK to 5,000 DKK could reduce your monthly premium noticeably.

Important caveat: Only raise your deductible to an amount you could comfortably pay in an emergency. If a 5,000 DKK expense would cause financial hardship, a lower premium isn't worth the risk.

Review Your Coverage for Your Current Situation

Life changes, but insurance policies often don't keep pace. Many drivers pay for coverage they no longer need because their circumstances have shifted.

Consider whether any of these apply to you:

- Working from home or switching to public transport reduces accident exposure; some insurers offer low-mileage discounts

- Vehicles valued below 30,000–40,000 DKK may cost more to insure comprehensively than they're worth to replace

- Once a car loan is paid off, lenders no longer require comprehensive coverage — dropping it can free up meaningful savings

- Removing children or other drivers who've left the household cuts premiums without affecting your own protection

A platform like Inzure can scan your policy documents and flag redundant coverages, missing protections, and overpriced premiums in about 60 seconds — without the hours of manual comparison work.

Improve Your Credit Score

Your financial profile can affect what you pay for insurance, even if indirectly. In Denmark, insurers cannot deny mandatory liability coverage due to debt register (RKI) registration, though they may demand higher prices or specific payment terms. Strengthening your credit standing can help you qualify for better payment terms and avoid surcharges.

In Denmark, insurers cannot deny mandatory liability coverage due to debt register (RKI) registration, though they may demand higher prices or specific payment terms.

Actionable steps to improve credit:

- Pay all bills on time, every time

- Reduce credit utilisation to below 30% of available credit

- Check your credit report annually for errors and dispute inaccuracies

- Avoid opening multiple new credit accounts in a short period

Explore Anti-Theft Devices and Safety Features

Vehicles equipped with anti-theft devices and modern safety features often qualify for insurance discounts because they reduce the probability of theft claims and serious collisions.

Anti-theft devices recognised by insurers:

- GPS trackers with real-time monitoring

- Steering wheel locks and immobilisers

- Alarm systems with tamper alerts

For highly sought-after vehicles, insurers like Tryg mandate GPS tracker installation to maintain theft coverage, and the company partners with providers to offer discounts on the hardware itself.

Modern safety features that may reduce premiums:

- Lane departure warning and lane-keeping assist reduce at-fault collision risk

- Automatic emergency braking (AEB) is one of the most widely recognised discount-qualifying technologies

- Adaptive cruise control and blind-spot monitoring lower the likelihood of rear-end and lane-change incidents

One caveat: Advanced Driver Assistance Systems (ADAS) can increase repair costs when sensors are damaged, which sometimes offsets premium discounts. Always confirm with your insurer which technologies qualify before assuming savings.

Discounts Most Drivers Are Leaving on the Table

Most insurers publish a long list of discounts they never volunteer to existing customers. Knowing what to ask for can cut your premium before you even consider switching.

Common discount categories include:

- Bundling home and auto policies saves 10–15% when you consolidate with one insurer

- Driving fewer than 10,000 km per year qualifies for low-mileage reduced rates

- Families with teen drivers who keep high grades can claim good-student discounts

- Going paperless (billing and e-signature) typically adds 1–3% off

- Insuring two or more vehicles with the same company lowers the per-vehicle cost

Loyalty doesn't pay — it costs. A 2025 report by the Danish Competition and Consumer Authority found that long-term customers pay an average of 1,108 DKK more per year than new customers for identical coverage. That's a loyalty penalty of 7–8 percentage points — and most policyholders have no idea it's happening.

Before each renewal, call your insurer and ask specifically which discounts apply to your policy. Don't assume they're already reflected in your bill — in most cases, they aren't unless you ask.

How to Compare Rates Without Spending Hours on It

Rate comparison is one of the highest-ROI actions a driver can take. Prices vary significantly between insurers for the same driver profile, and Danish consumer authorities recommend checking the market regularly to see if you can get a better offer.

Compare at least once a year, ideally before policy renewal. Your risk profile and market prices both change over time, and what was competitive last year may no longer be your best option.

One caveat: The cheapest policy is not always the best. Coverage quality, claims service, and financial stability matter. A policy that saves you 500 DKK annually but denies a legitimate claim costs far more in the long run.

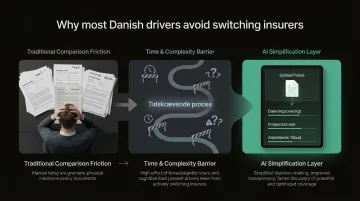

Why Most Drivers Skip This Step

Traditionally, comparing insurers meant:

- Calling multiple providers individually

- Reading through dense, jargon-heavy policy documents

- Manually cross-referencing coverage fine print

That process could easily take 10 hours or more — which is why most drivers simply don't bother.

For household insurance policies — home, travel, accident, and liability — platforms like Inzure cut that process to 60 seconds. You upload your policy as a PDF or photo, and the AI reads the document, extracts coverage details, and compares pricing and terms across Danish insurers.

The platform is independent (not tied to any insurer), GDPR-compliant with EU data storage, and free to use. You only pay 20% of the first year's savings if a better deal is found — and nothing if no better option exists.

Annual comparison is what consumer authorities recommend. Tools like this make it realistic to actually follow through.

Frequently Asked Questions

What are the solutions to reduce road accidents?

The most effective solutions are behavioural: eliminate distractions (especially mobile phones), practise defensive driving by maintaining safe following distances, obey speed limits, and anticipate the actions of other drivers. Driver education and awareness are consistently cited by road safety authorities as the foundation of accident prevention.

What are the 3 C's of driving?

The 3 C's of driving are Concentration, Caution, and Courtesy — staying focused on the road, exercising care in all manoeuvres, and respecting other road users to reduce conflict and collision risk.

Does taking a defensive driving course actually lower my insurance premium?

In Denmark, universal discounts for certified defensive driving courses are rare. However, telematics programmes like Tryg Drive offer up to 30% discounts for demonstrating safe driving behaviour through app-based scoring. Contact your insurer to confirm whether they offer telematics or course-based discount programmes.

How much can safe driving habits lower your insurance rate?

Avoiding even one at-fault accident can save thousands of kroner annually. A clean, claims-free record over several years compounds those savings further — qualifying drivers for lower base premiums and loyalty discounts that vary by insurer.

How often should I compare my car insurance rates?

Compare your rate once a year, timed before policy renewal. Both market prices and your personal risk profile shift over time, so regular comparison protects you from the loyalty penalty and surfaces better deals as they emerge.

What is the fastest way to lower car insurance costs right now?

Three moves work fastest: raise your deductible to a level you can comfortably cover, check for unapplied discounts (bundling, low mileage, paperless billing), and compare your current rate against the market using a tool like Inzure to see what you're actually overpaying.