This guide covers every natural trigger that lowers premiums, the actions you can take right now to accelerate savings, and the hidden reason loyal customers often pay more than they should.

Key Takeaways

- Rates drop naturally at key age milestones (especially around 25), after accidents and violations expire from your record (3–5 years), and as your vehicle depreciates

- Shopping the market at every renewal saves drivers thousands of kroner annually — yet the majority of drivers never compare quotes

- Raising your deductible can reduce premiums by 10–25% — one of the fastest ways to cut costs without changing your coverage

- Loyalty penalties are real: renewing customers consistently pay more than new applicants for identical coverage — switching or re-applying as a new customer regularly reveals lower prices

- Doing nothing costs you — a single market comparison at renewal takes minutes and routinely uncovers better deals

Why Car Insurance Rates Change Over Time

Insurers price premiums based on assessed risk—the higher the perceived likelihood you'll make a claim, the more you pay. When your risk profile improves, rates should follow. But there's a catch: insurers don't automatically update your premium mid-term when your situation changes for the better.

Key factors that feed into your risk score:

- Age and driving experience — younger, less experienced drivers pay significantly more

- Claims history — at-fault accidents and violations inflate premiums for years

- Vehicle type and age — high-theft or expensive-to-repair cars cost more to insure

- Annual mileage — more kilometers driven means higher exposure to accidents

- Location — areas with high theft, vandalism, or traffic density increase your risk score

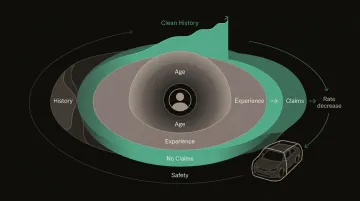

- No-claims bonus history — a clean record builds discount eligibility over time, while claims reset or reduce it

These factors don't update your premium automatically. Insurers typically reassess your risk at renewal, not continuously throughout the year. Even if you've moved to a safer area, reduced your mileage, or cleared a violation from your record, those improvements won't be reflected until your next renewal—and even then, only if you prompt the conversation or actively compare the market.

When Car Insurance Rates Go Down Naturally

Age and Driving Experience

Young and inexperienced drivers pay significantly higher premiums because they statistically have more accidents. In Denmark, 18-year-olds pay 10,000–18,000 DKK annually, while drivers aged 25+ pay 5,500–9,000 DKK—nearly half the cost. Crash rates for 16–19-year-olds are nearly four times higher than drivers aged 20 and above.

The age 25 milestone:

The reduction around age 25 is tied directly to a clean record alongside the age milestone. Progressive reports that drivers see an average 8% rate reduction at age 25, but this assumes no accidents or violations during the preceding years. One speeding ticket or at-fault claim can delay or eliminate this natural decrease.

Beyond 25:

Rates continue to stabilize and gradually decline through middle age. At age 60, drivers typically enjoy the lowest premiums of their driving lives. However, rates may rise again after age 75, as insurers factor in the increased severity of accidents involving older drivers. Between ages 60 and 80, premiums rise by 32% on average.

How Your Driving Record Affects Rates

Accidents and violations don't stay on your record forever—but they do linger long enough to meaningfully impact your premiums.

The 3-to-5-year rule:

At-fault accidents, speeding tickets, and other violations typically stay on your record and inflate your premiums for 3–5 years, depending on severity and insurer. Once they drop off, a rate reduction usually follows. A single speeding ticket raises rates by 10–30%, while an at-fault accident can increase premiums by 45% or more.

The clean record requirement:

Maintaining a spotless record continuously is what allows the drop to materialize. One new ticket resets the clock, extending the penalty period and delaying the reduction you've been waiting for.

Vehicle Age and Coverage Adjustments

As your car ages and depreciates in value, the cost to insure it—especially for comprehensive and collision coverage—typically decreases. The reason: the maximum payout the insurer owes for a total loss is lower.

The 10% rule:

Industry guidance recommends dropping comprehensive and collision coverage when the annual premium exceeds 10% of the vehicle's current market value. For example, if your car is now worth 30,000 DKK and your comprehensive/collision premium is 3,200 DKK annually, you're paying more than 10% of the vehicle's value. That's a clear indicator it's time to adjust coverage.

Vehicle type matters:

Switching to a car with better safety ratings and lower repair costs can produce an immediate rate drop. Key factors insurers weigh include:

- Theft frequency for the model in your region

- Repair cost and parts availability

- Active safety features (automatic braking, lane assist)

- Historical claims data for that vehicle class

In Denmark, vehicles with higher theft rates or costly repairs consistently attract higher premiums — regardless of the driver's record.

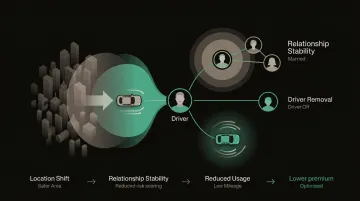

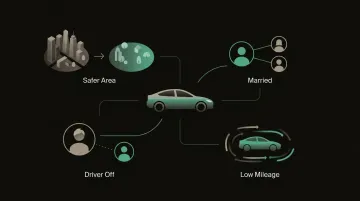

Life Changes That Trigger Lower Rates

Beyond age and record, changes in your personal situation can shift your risk profile — and your premium along with it:

- Moving to a lower-risk area - In Denmark, Roskilde is 23% cheaper than the country average, while Aalborg is 15% more expensive

- Getting married - Married drivers pay an average of 2,350 DKK less annually than single drivers (though widows may face a penalty)

- Removing a young driver from your policy - When a young driver moves out and gets their own coverage, your premium drops immediately

- Reducing annual mileage - Working from home or switching jobs can qualify you for low-mileage discounts (typically 5,000–7,500 miles per year)

What You Can Do to Lower Your Rates Sooner

Natural rate drops require patience. But there are concrete actions that can accelerate savings—and most people only use one or two of them.

Shopping the Market at Every Renewal

Insurers price new customers differently from existing ones. Industry surveys consistently show that the majority of drivers who switch carriers save money — often hundreds of kroner annually. Yet a large share of policyholders never seek an additional quote at renewal, leaving significant savings on the table. Comparing quotes takes minutes but can cut your annual premium substantially.

Adjusting Your Deductible

Increasing your deductible (the amount you pay out-of-pocket before insurance kicks in) directly lowers your premium.

How much can you save?

Raising your deductible can reduce premiums by 10–25% on average. The trade-off: you pay more out-of-pocket if you make a claim. This works well if you have emergency savings and a clean driving record. A lower deductible is the safer choice if you drive frequently in high-risk conditions.

Taking Advantage of Available Discounts

Many drivers qualify for multiple discounts but never ask. A 5-minute call or review at renewal can unlock:

- Bundling home and auto policies typically saves 7–25% on combined premiums

- Clean driving records qualify for safe driver discounts up to 22% off

- Driving fewer than 12,000 km per year often unlocks low-mileage pricing

- Students with strong academic results may qualify for 10–15% reductions

Enrolling in Telematics or Usage-Based Insurance

Apps or devices that track driving behaviour reward low-mileage, safe drivers with lower rates. Some programmes offer discounts up to 30% for qualifying drivers.

The telematics reality:

While insurers promote potential discounts, independent reviews suggest only around a third of enrolled drivers actually see premiums decrease — some even see rates increase. Telematics works best for drivers who work from home, drive infrequently, or maintain consistently safe habits.

Reviewing Your Policy Annually

Loyalty doesn't always pay. Danish insurers regularly raise premiums for existing customers while offering lower entry prices to new ones — a pattern known as the loyalty penalty. Reviewing your full policy each year, not just the premium total, can reveal price increases buried in renewal documents and coverage changes you never agreed to.

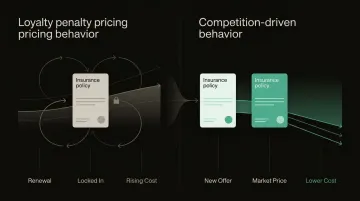

Why Waiting and Staying Loyal Can Cost You More

The "loyalty penalty" is a well-documented but rarely advertised practice where insurers offer new customers better rates than they charge existing, long-term policyholders. From the insurer's perspective, the math is straightforward: loyal customers rarely shop around, so there's little pressure to price competitively for them. The system rewards comparison and switching — not loyalty.

Regulators have taken notice. In 2022, the UK's Financial Conduct Authority banned price walking outright, estimating the reform would save consumers £4.2 billion over 10 years. Even so, a 2024 Which? survey found that 51% of renewing UK customers were still offered lower prices when they applied as a new customer for the same cover. The problem proved harder to eliminate than the regulation anticipated.

Across the EU, the issue follows the same pattern. In 2023, the European Insurance and Occupational Pensions Authority issued a supervisory statement directly targeting unfair price walking practices in European markets — a signal that regulators consider it widespread enough to warrant coordinated action.

The practical consequence for you: even if your risk profile has improved — longer policy history, no recent claims, better coverage fit — your premium may not reflect it. Insurers recalculate at renewal but don't always pass savings through proactively, particularly when they assume you're unlikely to leave.

Key Signs It's Time to Review Your Car Insurance Rate Right Now

Clear trigger events:

- Your annual renewal is approaching — the optimal window to shop is 30 days before expiry

- You've passed the 3-to-5-year mark since an accident or violation

- You've had a major life change: moved, got married, changed vehicles, reduced mileage, removed a driver from your policy

Less obvious triggers:

- You received an unexplained rate increase at renewal with no change in your own behaviour (a sign your insurer is betting you won't bother to shop around)

- You haven't compared quotes in more than 12 months (market rates shift, and your current rate may no longer reflect what's available)

Reviewing your rate doesn't mean committing to a switch. It means knowing what your policy should actually cost given your profile today. If your insurer won't match the market, that's useful information. If they will, that's a win without changing a thing.

Frequently Asked Questions

What can lower the cost of your insurance?

Shopping the market at renewal, bundling home and auto policies, increasing your deductible, and qualifying for discounts (safe driver, low mileage, good student) are the primary levers. Improving your credit score can help in markets where it's permitted.

How long until my insurance gets cheaper?

After an accident or violation, expect 3–5 years before rates return to normal. Actively comparing quotes at every renewal can deliver savings sooner than waiting for your risk profile to change on its own.

At what age do insurance prices go down?

Rates typically begin declining year-over-year from age 18–19, with a more noticeable drop around age 25. Premiums continue falling through middle age, reaching their lowest point around age 60, before potentially rising again after age 75.

Is it better to have a 500 kr. deductible or 1,000 kr.?

A higher deductible (1,000 kr.) lowers your premium by 10–25%, but means more out-of-pocket cost if you make a claim. It makes sense if you have emergency savings and a clean record. A lower deductible is safer if you drive frequently in high-risk conditions.

Will my car insurance go down in 2026?

Broad market rates have been rising industry-wide due to repair cost inflation and claims frequency. Whether your individual rate goes down depends on changes to your personal risk profile. Comparing quotes 30 days before renewal — rather than auto-renewing — gives you the best chance of seeing a lower rate.

What time of year is insurance the cheapest?

There is no single universally cheap season for car insurance. Rates vary based on your individual risk factors, not the time of year. The optimal time to compare and negotiate is 30 days before your renewal date; switching mid-term is possible but often comes with fees.