The truth is that penalties for switching insurance companies in Denmark are conditional, typically small, and often completely avoidable. Under Danish law, you have the legal right to cancel any personal insurance policy with one month's notice to the end of any calendar month - no justification required. The real question isn't whether you can switch, but whether the fear of a small fee is keeping you trapped in an overpriced policy that quietly costs you thousands of kroner each year.

The Short Answer: Can You Switch Insurance Companies Without a Penalty?

You can switch insurance companies at any time in Denmark. Forsikringsaftaleloven § 34 grants consumers the unconditional right to terminate insurance contracts with one month's notice. Cancellation fees are not automatic — they depend on on when you cancel and your insurer's specific policy terms.

The key distinction:

- Switching at renewal: No fee. When you cancel at your policy's annual renewal date (hovedforfaldsdato), every major Danish insurer — Tryg, Topdanmark, If, Alm. Brand — allows fee-free cancellation.

- Switching mid-term: Some insurers charge a fee when you cancel before your policy period ends — for example, six months into a 12-month contract.

The average mid-term cancellation fee after the first policy year ranges from just 74–84 DKK — a one-time charge that's often recovered within weeks if you're switching to a cheaper policy.

When Do Cancellation Fees Apply?

Danish insurers use a two-tier fee structure that depends on timing and policy tenure.

Cancellation at Renewal: No Fee

If you cancel at your policy's annual renewal date, there is no cancellation fee at any major Danish insurer. Your renewal date appears on your policy documents and in the annual renewal notice your insurer sends (typically 4-6 weeks before the policy expires). Switching at this point costs you nothing.

Mid-Term Cancellation: Fees Vary

When you cancel before your policy period ends, insurers may charge an administration fee. Under Forsikringsaftaleloven § 34, paragraph 2, this fee must be "reasonable" and reflect actual costs incurred by the insurer.

Two fee tiers:

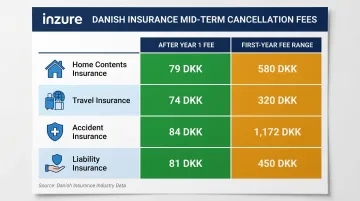

- After the first year: Flat administration fees of 74-84 DKK per policy across Tryg, Topdanmark, and Alm. Brand

- Within the first year: Higher fees ranging from 320 DKK to 1,172 DKK depending on insurer and product type

Which Policy Types Carry Mid-Term Fees?

| Insurance Type | Short-Notice Fee (After Year 1) | First-Year Fee Range |

|---|---|---|

| Home Contents (Indboforsikring) | 74-84 DKK | 320-502 DKK |

| Travel Insurance (Rejseforsikring) | 74-84 DKK | 484-1,172 DKK |

| Accident Insurance (Ulykkesforsikring) | 74-84 DKK | 484-502 DKK |

| Liability Insurance (Ansvarsforsikring) | 74-84 DKK | 320-770 DKK |

Source: Published fee schedules from Topdanmark and IDA Forsikring/Tryg

Travel insurance with world coverage carries the highest first-year fee at Topdanmark (1,172 DKK), while simpler products like accident insurance cluster around 500 DKK.

A Note on Variations

Fee amounts differ between insurers, and some charge nothing at all for mid-term cancellations. Always check your specific policy terms or contact your insurer directly to confirm what applies. You'll find the relevant details under "Gebyrer og afgifter" (Fees and charges) in your policy documents — knowing this figure upfront helps you weigh whether switching mid-term still makes financial sense.

How Much Are Insurance Cancellation Fees?

After the first year: Expect to pay 74-84 DKK as a flat administration fee when canceling mid-term. This is the most common scenario for consumers switching established policies.

Within the first year: Fees range from approximately 320 DKK to 1,172 DKK. Topdanmark's world travel insurance (single person) carries the highest fee at 1,172 DKK, while home contents and accident insurance typically fall between 320-502 DKK.

Percentage-based fees (rare): Some insurers use percentage-based fees for specific products. For example, Topdanmark charges 60% of the annual premium for first-year cancellation of dog and cat insurance — most personal lines use flat fees instead.

The Real Cost Comparison

Even the highest first-year cancellation fee (1,172 DKK) disappears quickly against real annual savings:

Case Study - Morten Olsen, Copenhagen:

- Loyal Tryg customer for 20+ years

- Received 12% price increase (487 DKK) on accident insurance

- Switched insurers and saved 8,000 DKK per year

- Even with a maximum 1,172 DKK cancellation fee, he recovered the cost in less than two months

Source: TV2 Nyheder, April 2025

Market-Wide Savings Potential: Forbrugerradet Taenk's August 2025 insurance package test found a price difference of 5,700 DKK (nearly 40%) between the cheapest and most expensive insurer for equivalent coverage across four insurance types.

Source: Taenk, August 2025

Unused Premium Refunds

Under Forsikringsaftaleloven § 6, insurers must refund the pro-rated unused portion of your premium when you cancel mid-term. This refund is calculated from your cancellation date forward and paid after deducting any applicable termination fee. In Morten's case, for example, a mid-year cancellation would have further reduced his effective switching cost below the 1,172 DKK fee.

The Hidden Penalty Most Loyal Customers Are Already Paying

The loyalty penalty is Denmark's worst-kept insurance secret. While you worry about a 74 DKK switching fee, your insurer quietly extracts thousands of kroner in extra premiums year after year.

The Danish Loyalty Tax: Quantified

In April 2025, Konkurrence- og Forbrugerstyrelsen (KFST) analyzed 7.4 million private insurance policies linked to individual-level register data from Danmarks Statistik. The findings were unambiguous:

Customers with 10 years of tenure pay on average 7-8 percentage points more than new customers at the same company with the same expected claims costs.

Source: KFST report, April 2025

Product-specific loyalty penalties:

- Home insurance (husforsikring): 443 DKK/year overpayment

- Home contents (indboforsikring): 240 DKK/year overpayment

- Accident insurance: No clear tenure-based penalty found

Forbrugerradet Taenk calculates that an average Danish household pays over 5,000 DKK more per year on non-life insurance than they would if prices had simply tracked general inflation.

Source: Taenk, September 2025

The Irony: The Penalty of Staying Exceeds the Fee for Switching

Compare the costs:

- One-time switching fee (mid-term, after year 1): 74-84 DKK

- Annual loyalty penalty (10-year customer): 5,000+ DKK

Over a decade of inaction, that loyalty penalty compounds to 50,000 DKK or more in cumulative overpayments. That's 50 to 100 times the cost of a single cancellation fee.

Real Savings: What Inzure Users Discovered

That 50,000 DKK figure isn't abstract. When real Danish households ran their policies through Inzure's AI platform, the loyalty surcharges they'd accumulated over years showed up in black and white — and the numbers were stark.

Documented savings range: Between 2,800 kr/year and 48,000 kr/year

Hans Henrik Beck, age 62:

- Eight years with Tryg

- Used Inzure to analyze family coverage

- Saved 48,000 kr/year (46% reduction in premiums)

Lise Nielsen, age 86:

- Discovered she'd been without home contents insurance for over 10 years

- Added proper coverage across three policies plus a fourth policy

- Still saved 2,800 kr/year (24% reduction) despite improving coverage

Both outcomes — and those in between — came from one thing: seeing the actual market price for the first time.

Regulatory Action Is Coming

On June 25, 2025, Konkurrenceradet formally launched a market investigation into private non-life insurance competition under Konkurrencelovens § 15 f. The Danish insurance market is under scrutiny precisely because of these loyalty penalty findings. For consumers, this signals that regulators now agree: the status quo isn't a neutral outcome — it's a structural disadvantage for anyone who stays put.

Source: KFST, June 2025

How to Switch Insurance Companies Without Paying a Penalty

Follow these five steps to switch insurers while avoiding fees and coverage gaps.

Step 1 - Time Your Switch to Renewal

Switching at your annual renewal date (hovedforfaldsdato) is the cleanest way to avoid cancellation fees. This date appears on your policy documents and in the renewal notice your insurer sends 4-6 weeks before expiry.

Action plan:

- Note your renewal date for each policy (different policies may renew on different dates)

- Start comparing quotes 4-6 weeks before that date

- Request cancellation at least one month before renewal to ensure fee-free exit

If you miss the renewal window, you can still cancel with one month's notice to the end of any calendar month. For example, canceling on July 10 means coverage ends August 31. The mid-term fee (74-84 DKK after year one) applies, but you'll receive a pro-rated refund for unused premium.

Step 2 - Compare Like for Like

A lower premium from a new insurer only benefits you if the coverage levels, deductibles (selvrisiko), and policy limits are equivalent or better.

Key elements to compare:

- Coverage types included (what perils are covered?)

- Sum-insured limits (where applicable)

- Deductible amounts (selvrisiko per claim)

- Exclusions and limitations (what's not covered?)

- Optional add-ons (bicycle theft, legal aid, etc.)

Don't assume "indboforsikring" means the same thing at every insurer. Coverage definitions vary. One policy's standard coverage may be another's premium tier.

Step 3 - Secure the New Policy Before Canceling the Old One

The new policy must be active before the old one ends. Even a single day without coverage creates risk — and may violate mortgage requirements if you own property.

Process:

- Purchase the new policy with a start date that matches or precedes your old policy's end date

- Confirm the new insurer's activation date in writing

- Only then cancel the old policy

Step 4 - Formally Cancel Your Old Policy

Under Danish law, the policyholder — not the new insurer — is responsible for canceling the old contract. In practice, most insurers now simplify this considerably. Many will handle the cancellation on your behalf, which also eliminates the risk of coverage gaps.

Option A — Insurer-Handled Cancellation (Preferred): If Forsikring and IDA Forsikring/Tryg both confirm they can cancel your old policy on your behalf if you provide explicit consent and current policy numbers. Forsikring & Pension's digital switching platform, launched February 2025, enables instant, secure data transfer between insurers when you authorize it.

Option B — Self-Managed Cancellation:

- Contact your old insurer by phone, email, or digital self-service platform

- Request cancellation with one month's notice (or at renewal date)

- Receive written confirmation of the cancellation date

- Verify the end date aligns with your new policy's start date

Most insurers accept cancellation by email or digital channels, though some products (certain accident policies) may require written notice.

Step 5 - Check for a Pro-Rated Refund

If you cancel mid-term, you're entitled to a refund for the unused portion of your premium under Forsikringsaftaleloven § 6. The insurer will deduct any applicable cancellation fee from this refund first.

Ask explicitly:

- "What is the pro-rated refund amount for my unused premium?"

- "When will the refund be processed?"

- "Will it be paid to my NemKonto or by check?"

Refunds are typically processed within 2-4 weeks of the confirmed cancellation date.

What Else to Watch Out for When Switching Insurers

Lost Discounts and Bundles

Danish insurers offer multi-policy discounts (samlerabat) ranging from 5-20%:

- Tryg: Up to 20% for 5+ policies

- If: Up to 15% via Fordelsprogram

- IDA Forsikring: 15% for IDA Gold members

Source: Tryg samlerabat

If you currently bundle home and auto (or other policies) for a discount, switching one policy without the other may remove that discount. Calculate whether the switch still makes financial sense with this in mind.

Critical counterpoint: Taenk's August 2025 test found that 4 of the 6 best-performing insurers offered no bundle discount at all. The cheapest overall packages came from companies without samlerabat. In 8 of 15 test cases, the insurer cheapest for one product was among the most expensive for others.

Source: Taenk, August 2025

Don't assume bundling equals savings. Compare total annual costs with and without the discount.

One other factor worth pricing in: if you hold multiple policies with the same insurer and a single event (like a burglary) triggers claims on both, you typically pay only one deductible. With different insurers, you may pay two.

Beyond pricing, switching also triggers some administrative steps worth handling proactively.

Notify Lienholders

If you have a mortgage on your home, your lender requires proof of continuous home insurance (husforsikring or indboforsikring) as a loan condition. When switching:

- Send your new proof of insurance (police eller dækningsbevis) to your bank or mortgage lender immediately after the switch takes effect

- Verify they've updated their records

Even a short coverage gap may violate your mortgage covenant.

Claims in Progress

You can switch insurers while a claim is open. The existing claim will continue to be handled by the insurer with whom it was originally filed — that claim belongs to whichever insurer was covering you when it happened.

Settle or at least formally file any open claims before switching to avoid communication complications between old and new insurers.

Frequently Asked Questions

Will my new insurance company cancel my old policy?

Many Danish insurers now handle the cancellation on your behalf if you provide explicit consent and policy numbers. If Forsikring and IDA Forsikring both offer this service, and Forsikring & Pension's February 2025 digital platform automates secure data transfer between member companies to streamline switching.

Is there a penalty for switching insurance mid-term?

A mid-term switch may result in a cancellation fee - typically 74-84 DKK after the first policy year, or 320-1,172 DKK within the first year depending on product type. However, insurers refund unused premium, and the fee is almost always smaller than the annual savings from a better policy.

Will switching insurance companies affect my credit score?

No. Denmark's RKI (Ribers Kredit Information) is a debtor registry for unpaid debts — not a credit inquiry system. Switching insurers, requesting quotes, or canceling policies has no impact on your RKI status.

Can I switch insurance companies if I have an active claim?

Yes. You can switch insurers while a claim is open. The existing claim stays with your current insurer — they remain contractually responsible for it regardless of when you leave.

What happens to my unused premium if I cancel early?

Danish law (Forsikringsaftaleloven § 6) requires insurers to refund the pro-rated unused portion of your premium when you cancel mid-term. Any applicable cancellation fee is deducted from this refund first, and the balance is paid to your NemKonto within 2-4 weeks.

How do I know if switching insurance is actually worth it?

Compare the total annual cost of both policies (including any cancellation fee), verify that coverage levels are equivalent or better, and check for lost bundle discounts. Tools like Inzure can also run this comparison for you — uploading your policy documents takes 60 seconds and shows the real market price for your coverage with no obligation to switch.