Introduction

Picture this: You receive your annual home insurance renewal notice, note the 6% price increase, and click "accept" without a second thought. You've been with the same insurer for seven years—surely loyalty means you're getting a fair deal?

Not quite. Data from the Danish Competition and Consumer Authority reveals that customers with 10+ years of seniority pay 1,108 DKK more annually than new customers for identical coverage. The home insurance market isn't just complex by accident—it's designed that way, making it nearly impossible for ordinary consumers to compare policies or challenge their premiums.

This guide cuts through that complexity. Here's what you'll come away with:

- How to evaluate coverage quality — not just price

- The key factors that determine what you should actually pay

- Proven tactics to lower your premium without losing the protection you need

Key Takeaways

- Home insurance policies vary dramatically in coverage quality—a lower premium doesn't mean better value

- Comparing quotes annually and claiming available discounts can meaningfully cut your premium

- The "loyalty penalty" means long-term customers often pay significantly more than new customers for identical cover

- AI tools can benchmark your existing policy against the Danish market in under 60 seconds

What Does Home Insurance Actually Cover?

Home insurance protects against financial loss from damage to your property structure, loss or damage to contents, liability for third-party injury on your premises, and in some cases, temporary accommodation costs. In Denmark, a single "home insurance" product typically bundles several of these components.

Danish home insurance generally includes two main categories:

- Indboforsikring (Contents Insurance): Covers personal belongings, temporary accommodation, and includes personal liability (ansvarsforsikring) and legal aid (retshjælp)

- Husforsikring (Building Insurance): Covers the physical structure against fire, storm, and water damage, plus homeowner's liability

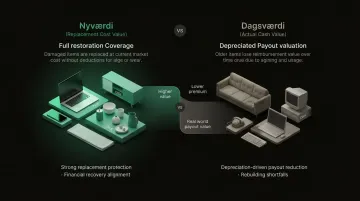

Nyværdi vs. Dagsværdi: The Payout Method That Changes Everything

Danish policies use two fundamentally different valuation approaches. Which one your policy uses determines how much you actually receive after a claim:

- Nyværdi (Replacement Cost Value): Pays the full cost to replace or repair items at today's prices, with no deduction for age or wear

- Dagsværdi (Actual Cash Value): Factors in depreciation — a five-year-old sofa that originally cost 15,000 DKK might only pay out 8,000 DKK

Nyværdi policies typically cost 15-25% more in premium. But if your home suffers major damage, a dagsværdi policy could leave you tens of thousands of kroner short of what you need to rebuild or replace.

What's NOT Covered: The Expensive Surprises

Standard Danish home insurance typically excludes:

- Groundwater and sea flooding — these require a separate policy

- Gradual wear and tear, or damage caused by poor maintenance

- Subsidence or ground movement

- High-value items above standard limits — jewelry, art, and electronics are often capped at 10,000-25,000 DKK per item unless specifically listed on your policy

Groundwater flooding is one of the most common gaps Danish homeowners discover only after a claim. Check your policy's exclusion list before you assume you're covered.

What to Look for When Choosing the Best Home Insurance Cover

Because policies differ so widely in structure, comparing home insurance requires looking beyond the headline premium. The right policy covers your actual risks without overpaying for coverage you don't need.

Coverage Limits and Adequacy

Underinsurance is one of the most expensive mistakes a homeowner can make. If your dwelling limit is set too low, you bear the shortfall in a major claim—and insurers apply the "average clause," reducing payouts proportionally.

UK benchmark data shows that 20-40% of residential properties are underinsured, with average shortfalls of 20-40% below true rebuild costs. Danish construction costs rose sharply between 2020 and 2023, meaning rebuild valuations set before that period are likely outdated.

Key principle: Insure at minimum for the full rebuild cost of your home—not its market value. A property worth 4 million DKK on the market might cost 5.5 million DKK to rebuild with matching materials and modern building codes. Personal property and liability limits should also reflect actual asset values.

Deductible Level (Selvrisiko)

The deductible trade-off is straightforward: a higher selvrisiko reduces your annual premium but increases your out-of-pocket cost when you claim. The right level depends on your emergency savings buffer and how frequently you're likely to claim.

Key things to know about selvrisiko:

- Danish insurers typically offer deductibles from 0 DKK up to 10,000+ DKK

- Peril-specific deductibles apply separately — cloudburst (skybrud) damage often carries a mandatory minimum of 6,000 DKK regardless of your standard selvrisiko

- A higher deductible can cut your premium by 10-20%, but only makes sense if you have the savings buffer to cover it

Insurer Reputation and Claims Handling

The true test of any insurer is how they behave when you file a claim. Before choosing a provider, check third-party ratings from Ankenævnet for Forsikring (the Danish Insurance Complaints Board) and EPSI Rating Denmark.

2024 Danish Insurer Performance:

| Insurer | Market Share | Total Complaints | Customer Win Rate | EPSI Score |

|---|---|---|---|---|

| Tryg | 19.1% | 85 | 14.1% | 72.7 |

| Topdanmark | 16.3% | 57 | 8.8% | 74.7 |

| Alm. Brand / Codan | 11.3% | 52 | 23.0% | 71.5 / 72.2 |

| If Forsikring | 4.6% | 30 | 23.3% | 75.2 |

| Alka | 5.7% | 23 | 4.3% | 77.2 |

Alka and Topdanmark have the lowest customer win rates in complaints — this may reflect strict but accurate initial assessments, or it may mean valid claims are being rejected on technicalities. Cross-reference with EPSI scores for a fuller picture. Tryg holds the largest market share but scores below average on customer satisfaction.

Policy Exclusions and Hidden Gaps

Once you've shortlisted insurers, dig into the policy wording — specifically the exclusions section. Common coverage gaps include:

- Damage from poor maintenance (insurers often deny these claims outright)

- Specific weather events not included in the base policy

- High-value items exceeding individual limits (jewelry, electronics, art)

- Gradual water damage versus sudden water damage distinctions

Ask your insurer directly about scenarios relevant to your property: "Is subsidence covered? What about water damage from an aging roof? Are my solar panels insured at replacement cost?"

Available Discounts and Bundling

Most Danish insurers offer discounts that are not automatically applied:

- Multi-policy bundling (home + car): 12-20% discount

- Security system installation: 5-15%

- Claims-free history: 5-10%

- Paying annually instead of monthly: 3-5%

- New customer incentives: 10-25%

Bundling Breakdown:

| Insurer | Maximum Discount | Required Policies |

|---|---|---|

| Tryg | 20% | 5 policies (including indboforsikring) |

| If Forsikring | 15% | 3 policies |

| Topdanmark | 12% | 3 policies (including indboforsikring) |

The table above shows the maximum possible bundling discount — but hitting that ceiling requires holding multiple policies with the same insurer. Consumer research from Taenk.dk shows bundling is rarely the cheapest overall option. Always compare the bundled quote against separate specialist policies before committing.

Proven Money-Saving Tips to Lower Your Home Insurance Premium

While you cannot control all pricing factors—location, build type, age of property—there are several levers fully within your control. These tips apply whether you're taking out a new policy or reviewing an existing one.

Shop Around Every Year—Not Just When It Feels Wrong

Auto-renewing is one of the most expensive habits in Danish home insurance. Insurers frequently raise premiums at renewal by more than the rate of inflation, betting on customer inertia.

Critical rule: Compare quotes on a like-for-like basis—same coverage limits, same deductible, same valuation method. A cheaper quote with lower limits is not a better deal; it's a coverage downgrade disguised as savings.

Increase Your Deductible (If Your Savings Allow)

Raising your selvrisiko from 1,000 DKK to 5,000 DKK can reduce your annual premium by 15-25%, depending on the insurer. The key qualifier: only increase your deductible to a level your emergency fund can cover.

Calculate the break-even point. If raising your deductible from 1,000 DKK to 5,000 DKK saves 1,200 DKK annually, you recover the higher deductible cost in roughly 3.3 years of claim-free coverage.

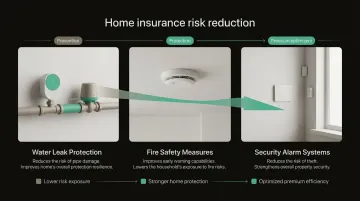

Install Security and Safety Features

Insurers price for risk. Verified risk-reduction measures lower your premium in concrete, measurable ways:

- Water leak sensors: Installing a CE-approved automatic shut-off system can trigger a 10% discount with If Forsikring and up to 25% off pipe damage coverage with Codan and Topdanmark

- Smoke detectors: EN 14604-compliant detectors yield 5-15% premium reductions

- Alarm systems: Certified burglar alarms can reduce premiums by 10-20%

Audit for Duplicate and Unnecessary Coverage

Many Danish homeowners unknowingly pay for the same protection twice. Emergency home cover may already exist through a premium bank account, utility provider plan, or an existing home insurance add-on.

Inzure's AI reads your uploaded policy documents and flags overlapping coverage in 60 seconds—no manual cross-referencing required.

Avoid Claiming for Small Repairs

Every claim, even a minor one, can increase your premium at renewal and potentially eliminate a no-claims discount. If the repair cost is close to or below your deductible, it's usually more cost-effective to pay out of pocket.

Break-even calculation: If your deductible is 5,000 DKK and the repair costs 6,000 DKK, you'll only receive 1,000 DKK from the insurer—but risk a premium increase of 500-1,000 DKK annually for the next 3-5 years.

Mistakes That Are Secretly Costing You More

Accepting the Renewal Price Without Challenge

The "loyalty penalty" is a documented phenomenon where long-standing customers are charged more than new ones. KFST data shows that customers with 10+ years of seniority pay an average of 1,108 DKK more annually for car, home, and contents insurance.

Insurers rarely volunteer this information. Customers who shop around — or simply ask for a better rate — consistently save money. The pattern is so widespread that regulators across Europe have moved to restrict it. In Denmark, the data is clear: loyalty costs you.

Choosing the Cheapest Policy Without Checking Coverage

A low premium can hide significant gaps in coverage — particularly around dwelling rebuild costs, contents valuation methods, and liability limits. If a major claim hits, that cheaper premium costs you far more than you saved.

Always verify that a cheaper quote includes:

- Replacement cost (nyværdi), not actual cash value (dagsværdi)

- Adequate dwelling limits based on rebuild cost, not market value

- Liability coverage of at least 5-10 million DKK

- Temporary accommodation and legal aid

Forgetting to Update the Policy After Changes

Significant changes to your property — renovations, new high-value items, a home office, or a change in occupancy — can affect both coverage adequacy and policy validity. Failing to inform the insurer could mean a claim is denied. It's a simple fix. Treat a policy review as an annual task alongside renewal: document major improvements, revalue high-ticket items, and confirm your coverage limits still reflect reality.

Avoiding these three mistakes won't just protect you from unexpected costs — it puts you in control of what you actually pay for coverage.

How Inzure Helps You Get the Best Deal

Inzure is Denmark's first independent, AI-driven insurance platform, founded on a straightforward idea: insurance complexity is not accidental — it's a business model. The platform reads and analyzes home insurance policies across all Danish insurers, including Tryg, Alka, and Topdanmark.

It identifies gaps, duplicates, and unjustified price increases, then benchmarks your current premium against the real market rate — all in 60 seconds.

Core benefits:

- No obligation to switch

- No insurer affiliation — Inzure works for you, not insurance companies

- GDPR-compliant EU data storage

- Transparent fee model: free to use; only 20% of savings if a better deal is found

- Ongoing market monitoring so your premium stays competitive year after year

The results from early users show what that kind of clarity is worth in practice. Savings have ranged from 2,800 DKK to 48,000 DKK per year. Hans Henrik Beck, a 62-year-old family coverage customer, achieved a 46% premium reduction (48,000 DKK annually) after 8 years with Tryg. Lise Nielsen, 86, saved 2,800 DKK annually while upgrading three existing policies and adding a fourth — discovering she'd been without home contents insurance for at least 10 years.

Upload your existing policy and find out what your home insurance should actually cost. For most users, the analysis takes 60 seconds and the savings run into thousands of kroner every year.

Conclusion

Finding the best home insurance isn't a one-time event — it requires annual review, active comparison, and a clear understanding of what your policy does and does not cover. The goal isn't the cheapest policy, but the one that gives you genuine protection at a fair, market-reflective price.

Active, informed consumers get better deals. The practical steps are straightforward:

- Review your policy annually, not just at renewal

- Request a market comparison before accepting any price increase

- Use an independent tool to identify gaps, duplicates, and overcharges

Inzure's AI analysis does this in 60 seconds — scanning your existing policy against the Danish market to show what you're actually paying versus what you should be. The savings people find are real: anywhere from 2,800 kr to 48,000 kr per year. The work required to find them no longer has to be.

Frequently Asked Questions

Frequently Asked Questions

How much does insurance cost for a high-value home in Denmark?

Premiums on high-value homes depend on rebuild cost, location, construction type, and coverage limits — not market value. Specialist Danish insurers typically price these policies from 17,000–35,000 kr annually for properties with rebuild costs in the 15–25 million kr range.

What not to say to home insurance?

Never speculate about the cause of damage before it's investigated, avoid admitting fault in liability situations, and do not provide inaccurate information about your property's condition or use. Misrepresentation—even unintentional—can void a claim.

How often should I review my home insurance policy?

Review your policy annually at minimum, ideally 4–6 weeks before renewal, and immediately after any significant home improvement, purchase of high-value items, or change in occupancy.

What is the difference between replacement cost and actual cash value coverage?

Actual cash value deducts depreciation from claim payouts, meaning older items pay out less. Replacement cost covers the full cost to replace items at today's prices — typically resulting in higher premiums but significantly better claim outcomes.

Does bundling home and travel insurance actually save money?

Bundling home insurance with travel, accident, or liability coverage typically results in a 10–20% discount in Denmark. That said, compare bundled quotes against separate specialist policies — the combined price is not always cheaper than buying each individually from the best provider in each category.