Introduction

Most homeowners assume their policy will cover them when disaster strikes. It often doesn't. Research consistently shows that a significant share of homes carry policies riddled with exclusions that only surface at claim time—when there's nothing left to do about it.

The problem isn't simply lacking a policy. It's the gap between what households expect to be covered and what their insurer actually pays out.

Global economic losses from disasters reached ca. 2.226 milliarder DKK in 2024, with 57% remaining uninsured—leaving a protection gap of ca. 1.267 milliarder DKK. In Europe, the natural catastrophe protection gap remains at 65%, meaning nearly two-thirds of disaster damage falls on households and governments rather than insurers.

That aggregate gap plays out at the individual level in predictable ways. Coverage limits fail to keep pace with rising construction costs, standard exclusions leave entire risk categories unprotected, and policy language shifts at renewal to narrow coverage in ways most policyholders never notice. This article breaks down where those gaps appear, what the data shows, and what to check in your own policy.

Key Takeaways

- Most Danish households have insurance — but a significant share are underinsured without knowing it

- Standard policies routinely exclude backed-up drain damage, subsidence, and specific storm damage scenarios

- Danish premiums rose 6.7% in 2024 while construction costs climbed nearly 20% since 2021

- Coverage gaps trace back to opaque policy language, low consumer awareness, and limited market transparency

- Tools like Inzure can now pinpoint missing coverage and pricing discrepancies across Danish carriers in under 60 seconds

What Are Home Insurance Coverage Gaps?

A home insurance coverage gap is the difference between the losses a homeowner reasonably expects to be covered and the protection their policy actually provides. Most homeowners discover this difference only after filing a claim.

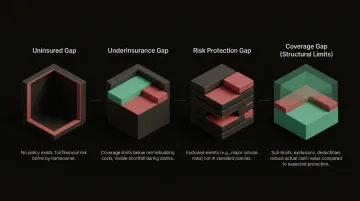

The Four Types of Coverage Gaps

| Gap Type | What It Means | Why It Happens |

|---|---|---|

| Uninsured Gap | No policy exists; the homeowner absorbs all financial risk | Deliberate choice or oversight; affects a minority but with total exposure |

| Underinsurance Gap | Policy limits fall short of actual rebuilding costs | Premiums set years ago haven't tracked construction cost inflation |

| Risk Protection Gap | High-impact risks (flood, earthquake, sewer backup) are excluded outright | Standard policies treat these as optional add-ons, rarely flagged at sale |

| Coverage Gap | Covered risks are subject to sub-limits, depreciation clauses, or high deductibles | Fine print reduces real payouts far below what policy language implies |

Most homeowners don't know which type applies to their own policy. Insurance policies are rarely written to be read — they're written to be filed away. The result is that gaps go undetected until a claim exposes them.

The Scale of the Problem: Key Statistics

The Uninsured Population

In the United States, 7.4% of homeowners—approximately 6.1 million households—carry no home insurance, leaving ca. 11,2 billioner DKK in property value completely exposed. Denmark performs considerably better, with 94% of the population holding home insurance, implying roughly 6% remain uninsured.

The Underinsurance Crisis

Even insured homes frequently carry insufficient limits. Verisk research shows that index-based valuations drift from actual replacement costs by nearly 4% after just three years, growing to approximately 7% by year four and approaching 11% at five years. Following the Marshall Fire in Colorado, state regulators found that at a rebuild cost of ca. 2.450 DKK pr. kvadratfod, 67% of total loss claims fell short of actual rebuild costs.

The Flood Coverage Misperception

Flooding drives up to 35-40% of weather-related disasters globally, yet only 3.9% of US housing units carry flood insurance. Outside mandatory floodplains, the rate drops to just 2.2%. Most homeowners assume their standard policy covers flood damage. It does not.

In Denmark, storm surges are covered through a public scheme charging a flat 40 kr annual fee across all fire policies. While this ensures broad participation, the flat-rate structure masks true risk costs and removes financial incentives for climate adaptation.

Premium Inflation Outpacing Coverage Quality

Home insurance premiums have risen sharply across markets:

| Geography | Premium Increase | Timeframe |

|-----------|------------------|-----------|

| Denmark | +6.7% | 2023-2024 |

| Europe | +3.0% | Q1 2024 |

| United States | +11.2% | 2021-2022 |

Danish premium growth outpaced the broader European average, driven by higher indexation and elevated claims costs. That cost pressure doesn't distribute evenly — it hits hardest among lower-income households and specific property types, which is where coverage gaps concentrate most severely.

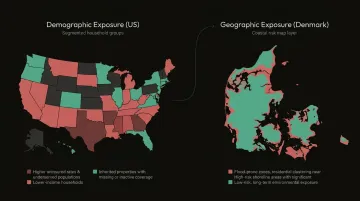

Geographic and Demographic Concentration

Coverage gaps cluster around specific populations and geographies. In the US, uninsured rates break down sharply by income and property type:

- 15% of homeowners earning under 350.000 DKK om året lack insurance — double the national average

- Manufactured homes carry a 35% uninsurance rate

- 29% of inherited homes have no coverage at all

Denmark faces serious geographic exposure on a different dimension. The country holds the 5th highest coastal flood risk in the OECD, with roughly 1 in 20 residents living in areas likely to flood every ten years. Over 8,000 new residential buildings were still constructed in flood-prone zones between 2009 and 2021.

Why Coverage Gaps Are So Widespread

Insurer-Side Dynamics

Insurance companies operate in intensely competitive, price-focused markets where reducing coverage depth is a low-visibility method to keep premiums attractive. Non-standard policy language, added exclusions, and narrowing of previously standard terms have become routine. These changes are rarely communicated clearly at renewal, meaning policyholders accept modifications without understanding their impact.

Consumer-Side Dynamics

Most homeowners buy insurance infrequently, anchor to price rather than coverage terms, and rarely read policy documents fully. Renewal inertia compounds this: most households accept auto-renewal without reviewing what has changed, letting gaps accumulate quietly across multiple policy cycles.

Information Asymmetry Problem

Standard policy documents are long, technical, and difficult to compare across providers. That complexity serves a purpose: insurers and intermediaries who compete on price have little incentive to make terms easier to evaluate. Without specialist knowledge or an independent tool, most consumers cannot identify coverage gaps on their own.

The Regulatory Gap

Insurance is regulated at national or regional levels, but regulatory focus traditionally centers on insurer solvency and pricing rather than coverage quality and adequacy. This leaves real consumer protection gaps the market has no incentive to close.

In Denmark, the relevant frameworks include:

- Finanstilsynet (Danish Financial Supervisory Authority) — supervises sector conduct and solvency

- Forsikringsaftaleloven (Insurance Contracts Act) — mandates clear disclosures to policyholders

- EU Insurance Distribution Directive — establishes Product Oversight and Governance requirements across member states

Each addresses disclosure and process. None directly requires that coverage terms remain adequate as household risks evolve over time.

How to Identify Your Own Coverage Gaps – Step by Step

Most Danish households have never systematically reviewed their own coverage. This five-step audit changes that — no specialist required.

Step 1 – Map Your Actual Risk Profile

List the specific risks your home faces based on location, construction type, age, and value. Include flood zone proximity, climate-related hazards, and local rebuilding costs before comparing anything against your policy. Without this baseline, you're reviewing your coverage blind.

Step 2 – Review Your Current Policy for Exclusions

Identify specific exclusions in your policy—flood, earthquake, sewer backup, mold, certain water damage, law and ordinance costs—and compare them against your actual risk profile from Step 1. The most dangerous exclusions are often buried in definitions or exception clauses rather than clearly labelled sections.

Step 3 – Verify Your Replacement Cost Coverage

Check whether your policy covers replacement cost or actual cash value for your home and contents. According to Eurostat's construction cost index data, EU residential building costs rose 52% between 2010 and 2023 — with Danish construction costs climbing nearly 20% since 2021 alone. Limits set just a few years ago are now severely insufficient.

In Denmark, the Construction Cost Index shows dramatic increases across key trades by Q4 2024:

- Earth and concrete work: 119.0 (19% above 2021 baseline)

- Bricklaying: 118.3 (18.3% above baseline)

- Electrical work: 120.7 (20.7% above baseline)

Policy limits set in 2021 and left unchanged almost certainly leave you underinsured by 15–20% or more.

Step 4 – Check for Duplicate or Redundant Coverage

Identify whether you're paying for coverage across multiple policies that overlaps unnecessarily—contents coverage in both a home policy and a separate policy, or liability coverage duplicated elsewhere. Duplicate coverage wastes premium budget that could fill genuine gaps.

Step 5 – Compare Your Policy Against the Current Market

The most effective step—and the hardest to do manually—is comparing your existing policy's coverage terms and price against what is currently available. Inzure's platform does this automatically: upload your policy document and within 60 seconds you'll see exactly where your coverage falls short, where you're paying for overlap, and what comparable policies from Danish carriers actually cost.

How Inzure Can Help

Inzure is Denmark's first AI-powered, independent insurance analysis platform — built to cut through the confusion that makes home insurance coverage gaps so common. Upload your existing policy and the platform reads it, identifies problems, and produces a clear report with no obligation to switch.

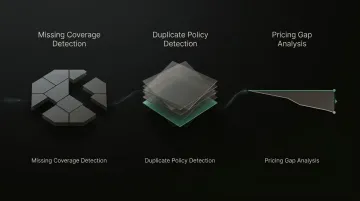

Core Capabilities

The analysis covers all Danish insurers and runs in approximately 60 seconds in a GDPR-compliant, EU-based environment. It identifies:

- Missing coverage, including the gaps described throughout this article

- Duplicate or overlapping policies you may be paying for unnecessarily

- Real-time pricing gaps between what you pay and what the market currently offers

Consumer-Aligned Model

Inzure's model aligns with consumer interests rather than insurer preferences. The platform is free to use and earns only a share of verified savings, meaning there is no financial incentive to recommend coverage that doesn't genuinely benefit the user. Early users have achieved savings ranging from 2,800 kr/år to 48,000 kr/år while simultaneously improving coverage quality.

Traditional brokers earn commissions from insurers, which shapes what they recommend. Inzure has no carrier relationships and no commissions — only a share of what you actually save.

Frequently Asked Questions

What percentage of homeowners file a claim each year?

In the US, approximately 5.3% of insured homeowners file claims annually. Danish insurers report frequencies between 6.8% and 15.1% depending on the carrier and coverage type. Because claims are rare, coverage gaps typically go unnoticed until the moment they matter most.

What are the most common types of home insurance coverage gaps?

The four main types are: being uninsured entirely, being underinsured (policy limits too low to rebuild at current costs), risk protection gaps (excluded perils like flood or earthquake), and coverage gaps (hidden limitations on otherwise covered losses). Of these, underinsurance affects the largest share of Danish policyholders.

Does standard home insurance cover flood damage?

No — flood damage is excluded from standard home insurance and requires separate coverage. In Denmark, storm surges fall under a public scheme, but regular flooding often remains excluded entirely.

What does it mean to be underinsured on a home policy?

Being underinsured means your policy limits are insufficient to fully cover rebuilding costs at current prices. With Danish construction costs rising nearly 20% since 2021, this is now the most common form of coverage gap affecting insured homeowners.

Why have home insurance premiums risen while coverage has narrowed?

Rising premiums are driven by increased climate-related claims, higher reinsurance costs, and rising construction prices. Coverage narrows because insurers manage risk through policy language changes—meaning homeowners often pay more for less protection.

How can I check if my home insurance has coverage gaps?

Conduct a structured review of exclusions, verify your replacement cost coverage, and compare your policy against current Danish market options. Platforms like Inzure can automate this analysis in about 60 seconds, flagging gaps, duplicates, and overpricing across carriers.