Introduction

Picture this: you're paying monthly premiums for home contents insurance, travel insurance, accident insurance, and liability insurance — four separate policies totaling thousands of kroner each year. Then something goes wrong. Maybe your bicycle is stolen from your apartment hallway, or you need legal help after a dispute with a contractor. You file a claim, confident you're covered. But you're not.

Buried somewhere in the exclusions section of your policy — probably clause 7.3, subsection (b), in eight-point font — is the exact exception that leaves you paying out of pocket.

This isn't bad luck. According to the International Association of Insurance Supervisors, exclusion clauses are among the top subjects of consumer complaints in the insurance sector globally — often "communicated in ways that are difficult for the average consumer to comprehend."

The average Danish household holds 6.1 insurance policies. Yet an EU Commission study found that only 2% of consumers use explanatory glossaries when comparing policies, and only 30% select the optimal provider for their needs.

This article explains how AI changes that. You'll see how automated policy scanning works, what it catches that manual review misses, and why Danish households with multiple policies have the most to gain from it.

Key Takeaways

- AI reads all your insurance documents simultaneously, not one at a time, extracting coverage details in under 60 seconds

- Three gap types exist: missing coverage, duplicate coverage, and loyalty price gaps (where long-term customers overpay)

- Manual review takes hours and still misses things — AI catches gaps, overlaps, and overpricing in seconds

- Danish users report annual savings between DKK 2,800 and DKK 48,000 by acting on AI findings

What Is an Insurance Coverage Gap?

A coverage gap is any real-life risk you face — illness, theft, fire, water damage, legal disputes — that your current insurance policies either don't cover at all or cover inadequately, meaning you'd pay the cost yourself if something went wrong.

Common examples in Danish households include:

- Home contents insurance that excludes slow water leaks or mold damage

- Missing personal liability coverage (ansvarsforsikring) despite owning property

- Travel insurance without coverage for quarantine costs or trip cancellations

- Bicycle theft coverage capped far below the actual replacement cost

- No legal aid insurance (retshjælp) when disputes with landlords or contractors arise

These aren't edge cases — regulators have documented them as a pattern. EIOPA's 2022 supervisory statement found that vague policy language creates predictable gaps across the market. Products advertised as "full coverage" or "complete coverage" frequently delivered far less.

As the report noted, many policies "only covered limited aspects like hospitalisation while excluding common related expenses like forced quarantines or cancellations" — exactly the scenarios consumers expected to be protected against.

Having multiple policies doesn't guarantee comprehensive protection. Individual policies are designed narrowly, covering specific risks within tight boundaries. Consumers naturally assume their combined policies provide blanket protection, but gaps slip through precisely because no one — not even the insurers — is looking at the portfolio as a whole.

Why Your Coverage Gaps Stay Hidden Without AI

Insurance companies benefit from complexity. Policy language is intentionally technical, exclusion lists run to dozens of clauses, and renewal terms often change without prominent notification. The business model depends on consumers not fully understanding what they're paying for.

The scale of the problem for Danish households:

- Average of 6.1 policies per household (Insurance & Pension Denmark)

- Each policy contains 20-40 pages of terms, conditions, and exclusions

- 97% of Danish households have home contents insurance

- 85% have personal accident insurance

- 75% have travel insurance

A genuine analysis would require reading 120-240 pages of legal text, cross-referencing coverage categories, and comparing market pricing — easily 10+ hours of work requiring legal comprehension most people don't have. That complexity alone keeps most people in the dark. But the hidden cost doesn't stop at confusion — research across multiple EU markets shows insurers also systematically overcharge long-standing customers:

| Country | Market | Finding | Source |

|---|---|---|---|

| Ireland | Home insurance | Customers with same insurer 9+ years pay 32% more than new customers | Central Bank of Ireland |

| Netherlands | Non-life insurance | Almost half of insurers charge higher margins to loyal customers | AFM, 2024 |

| UK | Contents insurance | Loyal customers (5+ years) pay 1.201 DKK vs. 487 DKK for new customers | FCA Market Study, 2020 |

With Nordic renewal rates of 80-90%, Danish consumers face the same market dynamics. Most auto-renew without ever checking whether their premium has risen year after year — a loyalty tax that can reach thousands of kroner annually. This is precisely the kind of pattern AI can surface in seconds, where manual review would take hours.

How AI Scans Every Insurance Policy in Your Portfolio

Reading Documents Like an Insurance Lawyer

Natural language processing (NLP) allows AI to read insurance policy PDFs — even those from different insurers with different formatting and terminology — and extract the essential terms: covered events, exclusions, deductibles, coverage limits, and renewal conditions.

Academic research from Uppsala University validated this approach using Swedish insurance documents (linguistically comparable to Danish). SBERT-based NLP models achieved 99.10% accuracy in text classification and 88.59% recall across 34 standardised coverage parameters including fire, burglary, travel, and weather damage.

The result: every document reviewed simultaneously, with gaps and exclusions flagged automatically — at a speed no manual process can match.

Cross-Policy Comparison and Risk Mapping

Once individual policies are extracted, AI maps every risk category — property damage, personal liability, medical, theft, travel disruption, legal expenses — against your actual portfolio.

The system identifies:

- Which risks are covered

- Which are covered by more than one policy (overlap)

- Which have no coverage at all (gaps)

Inzure's platform, for example, reads policies from Tryg, Topdanmark, Alka, Codan, GF, Alm. Brand, If, and Lærerstandens Brandforsikring, benchmarking your coverage against real-time Danish market data.

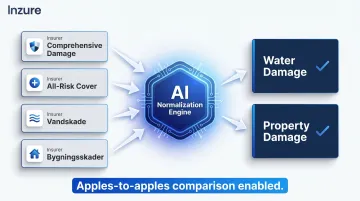

Handling Inconsistent Terminology Across Insurers

Cross-policy comparison only works if the underlying language is consistent — and it rarely is. Different insurers use different terms for identical concepts. One calls it "comprehensive damage," another "all-risk cover." "Vandskade" (water damage) appears explicitly in some policies, while others bury it under the broader "bygningsskader" (building damage).

AI models trained on insurance data normalise these differences, enabling genuine apples-to-apples comparison across your entire portfolio — regardless of which insurer issued each policy.

Continuous Monitoring vs One-Time Analysis

Unlike a manual review you might do once every few years, AI can monitor policies continuously, detecting:

- Renewal term changes that reduce coverage

- Premium increases above market inflation

- New market alternatives offering better pricing or coverage

- Life changes (new car, home renovation, child born) creating new coverage needs

Inzure's continuous monitoring alerts users only when there's actionable value — a better deal, a coverage upgrade at the same price, or a price hike worth challenging.

GDPR Compliance and Data Security

When you upload insurance documents, you're sharing sensitive personal and financial data. Responsible platforms must protect this under GDPR.

Look for platforms that offer:

- EU-based data storage (not US or non-EU servers)

- Explicit consent mechanisms before any AI processing begins

- No third-party data sharing without permission

- Clear data retention and deletion policies

Following the Datatilsynet's June 2024 ruling against IDA Forsikring, Danish platforms must obtain granular, informed consent specifically for AI analysis — users must be able to upload documents without automatically consenting to AI processing.

Inzure stores all data on EU servers, operates in full GDPR compliance, and shares no data with insurers or third parties unless explicitly authorised by the user.

The Three Types of Coverage Gaps AI Detects

Missing Coverage: The Risks You're Unprotected Against

Missing coverage is the most financially dangerous gap type: entire risk categories simply absent from your portfolio.

Common Danish examples:

- No contents insurance in a rental apartment

- Home insurance without personal liability cover

- Family policy missing critical illness coverage

- No legal aid insurance despite property ownership

These gaps are especially dangerous because you discover them only after a loss event. By then, it's too late.

How AI identifies missing coverage: By mapping your demographic profile (homeowner, renter, driver, family with children, frequent traveller) against your actual policies and flagging risk categories that match your profile but appear nowhere in your combined coverage.

For instance, if you're a homeowner with children but have no personal liability insurance, AI flags this immediately: you're exposed to potentially unlimited legal costs if your child accidentally damages someone else's property.

Duplicate Coverage: Paying Twice for the Same Protection

Duplicate coverage is extremely common and almost invisible to consumers.

EIOPA's Consumer Trends Report found that 14% of EU consumers purchased insurance bundled with non-insurance products — premium credit cards, bank accounts, employer benefit schemes — often duplicating separately purchased policies.

Most common overlaps:

- Travel insurance bundled with credit cards, premium bank accounts, and purchased separately as rejseforsikring

- Personal accident insurance overlapping between ulykkesforsikring, workplace coverage, and travel policy sub-covers

- Legal expenses insurance included in home contents policies while also purchased separately as retshjælp

AI detects overlap by mapping coverage categories across all policies simultaneously and flagging where two or more policies provide materially identical protection for the same risk event.

One Inzure user discovered she had been paying for travel insurance three ways: through her premium credit card, her bank account's insurance package, and a standalone rejseforsikring policy. Three separate charges. One layer of actual protection.

Loyalty Price Gaps: Overpaying for Identical Coverage

With loyalty price gaps, your coverage is fine. The problem is what you're paying for it. Auto-renewing for years without comparing the market means insurers quietly raise premiums while you assume you're getting a fair deal.

The pattern shows up across markets. A UK FCA market study found that 6 million policyholders paid 10,44 milliarder DKK in excess premiums in a single year, with loyal contents customers paying 1.201 DKK annually versus 487 DKK for new customers — nearly 2.5 times as much for identical coverage. Danish insurers use the same renewal model.

How AI detects pricing gaps:

- Compares your current premium against live market rates for equivalent coverage across all relevant Danish insurers

- Surfaces the true market price of your protection, often for the first time

- Flags how much your premium has drifted from the market over successive renewal cycles

Inzure reads across all Danish insurers — Tryg, Topdanmark, Alka, Codan, GF, Alm. Brand, and others — without ties to any of them. One user saved DKK 48,000 annually after the platform showed his premiums had climbed 46% over eight years with the same insurer.

What Happens After AI Finds Your Gaps

Understanding Your Gap Report

A useful AI gap report doesn't just list problems — it provides a prioritised action plan.

A good report includes:

- Which gaps pose the highest financial risk

- Which duplicates are easiest to cancel immediately

- Where switching providers would yield the greatest savings

- Plain-language explanations of complex policy terms

The report translates insurance jargon into actionable recommendations anyone can understand and act on. Instead of "inadequate liability limit vis-à-vis replacement cost valuation," you see: "Your bicycle coverage caps at DKK 5,000, but replacement cost is DKK 12,000 — you'd pay DKK 7,000 out of pocket if stolen."

Your Options After Gap Detection

Once you know where the problems are, you have three clear paths:

- Cancel duplicates immediately. Stop paying for coverage you already have elsewhere — the fastest route to savings, no comparison shopping needed.

- Add missing coverage. Upgrade your existing policy or switch to a more comprehensive provider. Prioritise gaps that pose the highest financial risk first.

- Switch to a better-priced alternative. Use market price comparisons to negotiate with your current insurer or move to a competitor offering the same coverage for less.

Inzure's platform facilitates the actual switching process, managing cancellation timelines, ensuring continuous coverage with no gaps, and handling documentation. But only if you choose to proceed — there's no obligation, and you can back out at any point.

The Value of Ongoing Monitoring

Coverage needs change with life circumstances. You buy a new bicycle. You renovate your kitchen. A child is born. Each creates new risks requiring updated coverage.

Insurer pricing also shifts constantly. A competitor launches a promotional rate. Your insurer raises premiums at renewal. The market moves.

Continuous AI monitoring catches these changes automatically, alerting you only when there's actionable value:

- A better deal has emerged from a competing carrier

- A coverage upgrade is now available at your current price point

- A premium increase has appeared that's worth challenging at renewal

You never fall back into the same problem because the system continuously monitors the market for you.

Frequently Asked Questions

What is an insurance coverage gap?

A coverage gap is any risk you face in daily life — theft, fire, liability, illness, legal disputes — that your current insurance policies don't cover or cover inadequately, meaning you'd bear the full cost personally if that event occurred.

How does AI detect gaps in my insurance coverage?

AI reads every insurance document using natural language processing, extracting coverage terms, limits, and exclusions across all policies simultaneously. It then flags missing risks, duplicate coverage, and overpriced premiums by benchmarking against current Danish market data.

Can I really have duplicate insurance coverage without knowing it?

Yes, and it happens more often than most people expect. Travel insurance frequently appears across premium credit cards, bank accounts, and standalone policies. Most consumers never compare the benefits of all their policies side by side, so they pay two or three times for the same protection.

How often should I check my insurance portfolio for coverage gaps?

Check at every policy renewal, after any significant life event (moving home, buying expensive items, having children, changing jobs), and ideally through a platform that monitors continuously so changes are caught automatically as they happen.

Is it safe to upload my insurance documents to an AI platform?

Look for GDPR-compliant EU data storage and a clear policy against sharing documents with insurers or third parties. Inzure stores all data on EU servers, requires explicit consent before processing, and operates independently with no insurer affiliations.

What should I do if AI detects a coverage gap in my insurance?

Start with the highest-risk gaps — personal liability, critical illness, and legal aid coverage. Then cancel confirmed duplicates to recover wasted premiums, and use the market price comparison to switch or negotiate anywhere you're overpaying.