Introduction

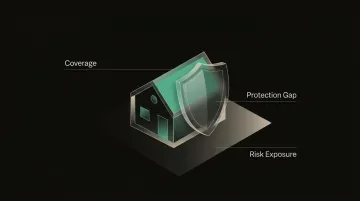

Most Danish consumers assume they're covered—until they're not. An insurance "coverage gap" describes any situation where your policy fails to fully protect you financially. That gap might be the missing theft coverage you never knew was absent from your home contents policy until you filed a claim. Or the travel insurance exclusion that surfaces only after a cancelled trip leaves you 12,000 kr. out of pocket.

Coverage gaps are common because insurance policies are deliberately complex. This isn't an accident—it's a business model. Contracts are written in technical language, exclusions are buried in fine print. Most Danes renew year after year without checking what they're actually paying for. Critical gaps stay invisible until a financial shock forces them into view.

This article focuses on the gaps most likely to affect Danish households: hidden shortfalls within home contents, travel, accident, and liability policies. By the end, you'll know how to spot them, understand what they cost you, and close them before claim time.

TLDR:

- Coverage gaps appear when your policy doesn't cover a loss you assumed it would—usually discovered at the worst possible moment

- Home contents policies often have outdated sums insured that leave you undercompensated after a burglary or fire

- Travel and accident policies frequently exclude specific scenarios buried in fine print most people never read

- Duplicate coverages and missing protections cost Danish households thousands of kroner each year

- Proactive policy review every two years prevents expensive surprises and closes gaps before they materialise

What Is an Insurance Coverage Gap?

An insurance coverage gap is any instance where your existing insurance does not fully cover a financial loss you reasonably expect it to cover. The critical word is "expect"—most consumers only discover what their policy actually excludes, limits, or fails to protect at the moment they file a claim.

The term "coverage gap" applies across different policy types:

- Home insurance gaps — Contents undervalued, high-value items excluded, or water damage scenarios not covered

- Travel insurance gaps — Missing cancellation coverage, exclusions for pre-existing conditions, or caps too low to cover actual costs

- Accident and liability gaps — Coverage limits that haven't kept pace with your actual financial exposure

- Overlap gaps — Duplicate coverages you're paying for twice without realizing it

Why Coverage Gaps Are So Common

Coverage gaps persist because insurance policies are structurally complex. Across the EU, 18% of citizens display low financial literacy, while 64% have only medium-level understanding. This literacy gap translates directly into coverage gaps — consumers struggle to parse technical exclusions, policy limits, and the rights embedded in their contracts.

The structure of insurance products makes comparison impractical by design:

- Terms differ between carriers for the same type of coverage

- Exclusions are buried in dense policy language

- Pricing structures obscure the actual value you'd receive in a claim

The result is predictable. Most Danish consumers renew automatically each year without reviewing what they're paying against what they'd actually receive if they filed a claim — allowing gaps to persist undetected for years.

How Auto Gap Insurance Works

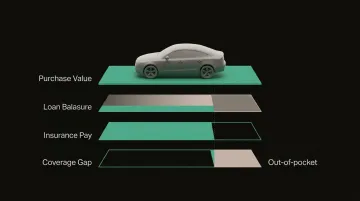

The Core Mechanic: ACV vs. Loan Balance

When a financed or leased vehicle is totalled or stolen, a standard Danish comprehensive auto insurance policy (kaskoforsikring) pays only the car's current market value—known as markedsværdi or Actual Cash Value (ACV). It does not pay the outstanding balance on your loan.

Because new cars depreciate rapidly, a gap opens almost immediately after purchase. Danish vehicles typically lose about 20% of their value during the first year, and 30-40% after three years. If you financed with a small down payment or a long loan term, you'll owe more than the car is worth for years.

Concrete Example:

- Car purchase price: 300,000 kr.

- Loan balance after 18 months: 240,000 kr.

- Insurer's ACV payout: 195,000 kr.

- Gap you must pay out of pocket: 45,000 kr.

That 45,000 kr. becomes your liability — regardless of whether you still have the car.

What Auto Gap Insurance Covers (and Doesn't)

Covered:

- The difference between the insurer's ACV payout and your remaining loan or lease balance

Not Covered:

- Mechanical repairs or breakdowns

- Rental car costs

- Personal injuries

- Damage to other vehicles or property

- Deductibles on your primary kaskoforsikring

Gap insurance also requires that you maintain active comprehensive (hel kasko) and collision coverage. If you drop to liability-only (ansvarsforsikring), gap coverage becomes void.

When Auto Gap Insurance Makes Sense

Auto gap insurance is essential if you:

- Made a small or no down payment (less than 20%)

- Financed for 60 months or longer

- Leased your vehicle (private leasing accounted for 38.48% of new car acquisitions by Danish consumers in 2023-2024)

- Bought a model with high depreciation rates

- Rolled over negative equity from a previous vehicle into the new loan

In these situations, the loan balance stays above the vehicle's market value for several years — meaning a total loss at any point leaves you with an out-of-pocket bill. The longer your loan term or the faster the car depreciates, the larger that bill can be.

Gap coverage makes financial sense for exactly as long as that imbalance exists.

When Gap Insurance Is NOT Worth It

Once your loan balance drops below your vehicle's current market value, there's no gap left to cover. Here's how to track this:

- Annually: Compare your remaining loan balance against your car's estimated value

- Use: Valuation tools like Bilbasen or FDM's pricing guides for a reliable market estimate

- Act: When the numbers cross — loan balance below market value — cancel gap coverage immediately

Continuing to pay premiums past that point is money with no protective purpose.

How Health Insurance Coverage Gaps Work

Personal Health Coverage Gaps

A health insurance coverage gap is any period during which you have no active supplementary health insurance (sundhedsforsikring). Even a short gap can expose you to catastrophic out-of-pocket costs if illness or injury occurs during that window.

Common triggers include:

- Job transitions (between employer-provided policies)

- Losing parental coverage at age limits

- Waiting periods with a new employer

- Retirement, when employer coverage ends

In 2023, 2.9 million Danes held supplementary private health insurance, but 94% of these policies are employer-provided. Because coverage is tied to individual employment contracts, it typically ceases when you leave your job or retire, creating a severe hidden gap during transitions.

Personal gaps aren't the only risk. Denmark's tiered public-private system also leaves some individuals without adequate cover at the structural level.

Systemic Health Coverage Gaps

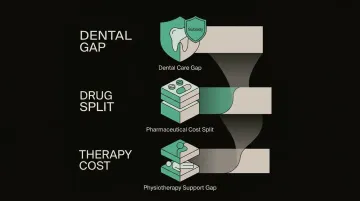

Some people fall between income thresholds — too high to qualify for certain public subsidies but unable to afford robust private premiums. Denmark's universal public healthcare (sygesikring) covers hospital care, but it stops well short of full coverage.

Out-of-pocket realities:

| Service | Public Coverage | Your Cost |

|---|---|---|

| Adult Dental Care | Limited subsidies; adults over 21 generally pay for exams and treatment | Over 9% of Danish adults reported unmet dental needs due to cost |

| Outpatient Pharmaceuticals | Only 42% publicly covered | Patients directly contribute 52% of retail pharmaceutical costs |

| Physiotherapy | Approx. 40% subsidized with doctor's referral | You pay remaining ~60% unless covered by private insurance |

Without supplementary coverage, dental care, physiotherapy, and most prescriptions come entirely out of your own pocket — even within Denmark's well-funded public system.

Consequences of a Health Coverage Gap

Even short gaps carry serious risk:

- Delayed or foregone medical care due to cost concerns

- Accumulation of medical debt for treatments not covered by the public system

- Locked out of private specialist care when you need it most

Accidents and illness don't wait for your next policy to activate. Being uninsured during even a brief window can create financial and health consequences that take years to resolve.

Hidden Coverage Gaps in Your Existing Policies

The most overlooked coverage gaps aren't lapses or canceled policies. They're missing protections buried inside active policies you're already paying for.

Missing or Inadequate Coverage

Common examples:

- A travel insurance policy (rejseforsikring) that excludes pre-existing conditions the policyholder assumed were covered

- A contents policy (indboforsikring) with a sum insured that hasn't kept pace with inflation, leading to severe underpayment in a total loss

- A "sumløs" (sumless) home contents policy that appears unlimited but contains hidden per-item limits—such as 15,000 kr. caps on jewelry or bicycles

Danish consumer authority Forbrugerrådet Tænk warns that many consumers believe they have comprehensive coverage, only to discover critical exclusions or caps when they file a claim.

Duplicate Coverage: Wasting Money Without Gaining Protection

The mirror problem to missing coverage is paying for the same protection twice. Many premium credit cards (Mastercard Gold/Platinum, Visa Premium) include annual travel insurance for Europe or worldwide trips. Consumers who purchase standalone travel insurance (rejseforsikring) without checking their card benefits pay twice for identical coverage, wasting hundreds of kroner annually.

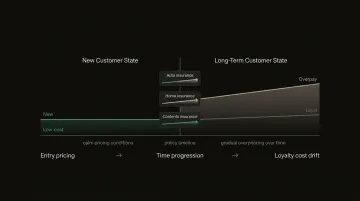

The "Loyal Customer Penalty"

Danish insurers systematically overcharge long-term customers. A 2025 report by Konkurrence- og Forbrugerstyrelsen revealed that insurers achieve margins 7-8 percentage points higher on loyal customers compared to new ones, costing households:

- Auto insurance: 425 kr. annually for customers with 10+ years tenure

- House insurance: 443 kr. annually

- Home contents: 240 kr. annually

This penalty is driven by automatic indexation clauses that raise premiums quietly at renewal without explicit warnings. Over a decade, this compounds into thousands of kroner paid unnecessarily, creating a growing gap between what you pay and what fair market pricing would be.

The Invisibility Problem

That compounding cost is difficult to see because these gaps are built into the fine print. Manually reading policy documents, comparing exclusion clauses across carriers, and tracking market pricing takes hours of work.

Most consumers don't have that time, and insurers know it.

The Real Consequences of a Coverage Gap

Financial Exposure

The direct cost of an uninsured loss can be catastrophic:

- A 45,000 kr. car loan shortfall after a total loss

- Thousands of kroner in uncovered dental or physiotherapy bills

- A rejected home contents claim due to a per-item limit you never knew existed

These losses wipe out emergency savings, force debt, and derail financial plans built on the assumption that your insurance would protect you.

Psychological and Practical Fallout

Discovering a coverage gap at claim time triggers stress, delays in recovery, and long-term financial anxiety. When an expected safety net fails to hold up, it undermines trust and forces difficult decisions — skip treatment, delay repairs, or go into debt.

In Denmark, 15% of consumers reported having a claim rejected within the last three years. Across the EU, claims-related issues account for 58% of all insurance complaints.

Who Gets Hit Hardest

Those complaint numbers aren't random. Coverage gaps disproportionately affect loyal, set-and-forget customers who trust their insurer but never review their policies. Year after year, they pay rising premiums for coverage that no longer matches their needs — or worse, never matched them in the first place.

How to Identify and Close Your Coverage Gaps

Practical Review Checklist

To uncover hidden gaps:

- Gather all active policies in one place (home, contents, travel, accident, liability)

- Check sum insured figures against current replacement costs—has inflation left you underinsured?

- Read exclusion clauses carefully—what specific situations does your policy refuse to cover?

- Compare your current premium against market rates for equivalent coverage

- Verify you're not paying twice for the same coverage (for example, travel insurance via credit card + standalone policy)

The Time Problem (and the Technology Solution)

Traditionally, this review process takes many hours. You must manually read dense policy documents, call multiple insurers for quotes, decipher technical insurance jargon, and compare terms that insurers write deliberately to resist comparison.

Inzure's AI-powered platform cuts that process to 60 seconds, analysing your existing Danish insurance policies and automatically flagging:

- Missing coverages you need but don't have

- Duplicate coverages draining your budget

- Whether your premium reflects the current market rate

The analysis is free—you only pay if you switch, and even then it's just 20% of the annual savings you achieve. If no better deal exists, you walk away with a clear picture of where you stand.

When to Review

Best times to check for coverage gaps:

- Before renewal — Don't wait for automatic renewal to lock in another year of overpayment

- After major life events — New home, new car, new family member, job change, or retirement

- After a significant premium increase — Unexplained jumps often signal the loyalty penalty at work

Forbrugerrådet Tænk advises consumers to actively re-shop and compare policies at least every two years to combat the loyalty penalty and ensure adequate coverage. Don't wait until a claim reveals the gap.

Frequently Asked Questions

What does gap insurance cover?

Auto gap insurance covers the difference between your car's actual cash value (the insurer's payout after a total loss) and the outstanding balance on your loan or lease. It does not cover repairs, mechanical breakdowns, injuries, or damage to other property—only the loan shortfall.

At what point is gap insurance not worth it?

Once your remaining loan balance equals or falls below your vehicle's current market value, the gap no longer exists. At that point, you're paying for nothing—cancel the coverage immediately.

What happens if you have a gap in insurance coverage?

Any loss, illness, or accident during an uninsured period becomes entirely your financial responsibility. This can mean large out-of-pocket expenses, medical debt, or going without necessary treatment or repairs.

How does a gap in health insurance coverage work?

A health coverage gap is a period without active supplementary health insurance, during which costs outside Denmark's public system—dental, certain pharmaceuticals, physiotherapy—must be paid entirely out of pocket. Denmark's universal healthcare does not cover everything, and private supplementary gaps leave those specific treatments unprotected.

Is it bad to have a gap in health insurance coverage?

Yes, even a brief gap is risky because accidents and illness are unpredictable. The financial and health consequences of being uninsured—even temporarily—can be serious and hard to recover from, particularly for treatments the public healthcare system does not fully cover.

What happens if your car is a total loss and you have gap insurance?

Your standard comprehensive (kaskoforsikring) pays the car's current market value first. Your gap insurance then covers the remaining loan balance above that amount, eliminating the out-of-pocket shortfall so you don't owe money on a car you no longer have.