Introduction

For most Danish households, insurance is a set-and-forget expense. You renew automatically each year, assume everything is in order, and move on. A recent investigation by the Danish Competition and Consumer Authority found that customers with 10+ years of tenure pay profit margins 7-8 percentage points higher than new customers for identical coverage, costing the average household over DKK 5,000 annually.

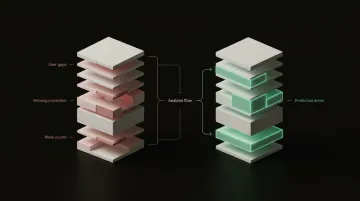

A policy gap analysis fixes that. It compares your current coverage against what you actually need, identifying where protection is missing, duplicated, or outdated.

This isn't just about paying too much. Policy gap analysis uncovers missing coverage that only reveals itself when a claim is rejected, duplicate policies that waste premiums, and outdated coverage limits that no longer reflect what your assets are actually worth. Most people discover these gaps only when it's too late.

This guide walks you through what a policy gap analysis involves, what to look for in your own policies, and how to conduct one without spending hours buried in fine print.

Key Takeaways

- Policy gap analysis compares your existing insurance against your real needs to uncover coverage gaps, duplicate policies, and premiums above market rate

- The process covers four steps: inventory your current policies, map your actual risk exposure, compare the two, then act on what you find

- Common gaps include missing coverage, duplicate policies, outdated limits, and loyalty premiums above market rate

- Conduct this analysis annually or after major life changes (buying a home, having a child, a significant change in income)

- AI-powered platforms like Inzure automate this process in 60 seconds rather than hours

What Is a Policy Gap Analysis?

A policy gap analysis is a structured review that measures the difference between the insurance coverage you currently hold and the coverage you actually need based on your current circumstances. The audit gives you a clear, actionable picture of where you are underinsured, overinsured, paying too much, or missing protection entirely.

The outcome is straightforward: you understand exactly what coverage you have, what you're missing, what's duplicated, and whether you're paying a fair market price. That kind of visibility makes it possible to act — not just wonder.

Not Just a Price Comparison

A policy gap analysis differs from a simple price comparison. Price comparison only looks at premium cost — what you pay each year. A gap analysis goes further:

- Evaluates whether your coverage is sufficient for your actual situation

- Checks policy conditions and exclusions, not just headline price

- Flags duplicate policies that are quietly draining your budget

You might find a cheaper policy through price comparison. But if it carries exclusions your current policy doesn't, you've closed a premium gap while opening a coverage gap.

Why Insurance Policy Gap Analysis Matters

Insurance policies are written in deliberately complex language. Insurers rarely tell you when your coverage becomes inadequate — that information asymmetry works in their favor, not yours.

The Loyalty Penalty Problem

Research and consumer advocacy groups have identified that long-term customers at the same insurer often pay significantly more than new customers for identical coverage. The Danish Consumer Council (Forbrugerrådet Tænk) calculates that automatic, unnotified price increases cost the average Danish household over DKK 5,000 more annually for non-life insurance compared to general inflation trends. That's real money leaving your account each year — not because your coverage improved, but simply because you didn't switch.

What Goes Wrong Without a Gap Analysis

The loyalty penalty is just one failure mode. Without regular gap analysis, coverage problems compound quietly across three fronts:

- Gaps surface at claim time — your bicycle is stolen and you discover theft wasn't covered, or a family member isn't listed on your travel policy

- Coverage goes stale as life changes: a new home, added family members, or recently acquired assets may fall outside policies written years ago

- Duplicate coverage wastes premiums when, for example, credit card travel insurance and a standalone policy both cover the same medical costs with no added benefit

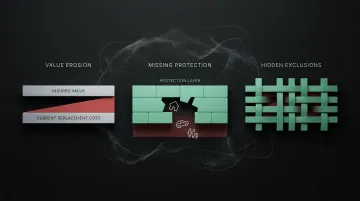

Types of Policy Gaps in Insurance

Policy gaps fall into three main categories, each representing a different type of financial or protection risk.

Coverage Gaps

Coverage gaps occur when a specific risk or asset is not covered at all, or coverage limits are too low to cover the actual value of a loss. Common examples include:

- Home contents insured at 2015 values in 2025, leaving a significant shortfall if you need to replace everything today

- Missing family members on existing policies — left completely unprotected

- Exclusions for risks you assumed were covered (bicycle theft, legal assistance, cancellation protection)

According to EIOPA's Consumer Trends Report, 22% of consumers are unsure about their exact coverage or exclusions, leading to unexpected out-of-pocket costs at claim time.

Duplicate Coverage Gaps

When multiple policies cover the same risk, you pay twice for protection you can only use once. Insurers pay out per incident — not per policy — so overlapping coverage generates no extra benefit, only extra cost.

Common duplication scenarios include:

- Standalone travel insurance when your premium credit card already includes global travel coverage

- Separate electronics insurance when your contents policy already covers high-value items

- Cancellation insurance purchased for each trip when your home insurance includes this as an add-on

Premium Gaps

Premium gaps occur when you pay significantly above market rate for your current level of coverage — typically because policies renew automatically without any price benchmarking against the market.

Danish insurance customers with 10+ years of tenure pay margins 7-8 percentage points higher than new customers for identical coverage. For a household spending DKK 22,281 annually on insurance (the Danish average), this penalty compounds year after year through automatic indexation.

How to Conduct a Policy Gap Analysis

A thorough policy gap analysis follows a logical sequence: understand what you have, define what you need, compare the two, then act on the findings. The process can be done manually, though the right tools make it considerably faster.

Step 1: Inventory Your Current Policies

Collect all active insurance policies — home (indboforsikring), travel, accident, liability, legal aid, bicycle theft, and contents — and record key details for each:

- Provider name

- Annual premium

- Coverage limits (sum insured)

- Key exclusions

- Renewal date

Many Danish households have policies spread across multiple providers (Tryg, Alka, Topdanmark) and struggle to get a complete picture without deliberate effort. Gather policy documents as PDFs or take photos of physical documents.

Step 2: Map Your Actual Risk Exposure

List all assets, liabilities, and life circumstances that require protection. This "needs inventory" becomes the benchmark against which existing coverage is measured.

Your risk inventory should include:

- Current property value (not purchase price from years ago)

- Number of household members and their needs

- Vehicle value

- Income level and dependents

- Outstanding loans or liabilities

- High-value possessions (electronics, jewelry, bicycles)

- Regular travel patterns

Step 3: Compare Coverage Against Needs

For each risk category, compare the coverage you hold against the exposure you identified:

- Is coverage absent entirely for any risk?

- Are coverage limits below the asset value?

- Do policies contain exclusions that leave significant risks unprotected?

- Are all household members listed on relevant policies?

Flag any area where there's a mismatch. According to Insurance Complaints Board data, insurers successfully defend their coverage exclusions in approximately 75% of consumer disputes, meaning gaps discovered at claim time rarely resolve in the customer's favor.

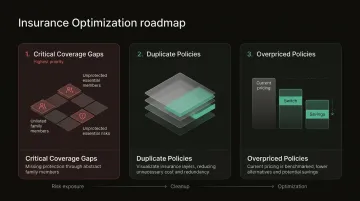

Step 4: Identify Duplicates and Overpricing

Review policies for overlapping coverage across multiple providers. Do you have travel insurance through your credit card and a standalone policy? Are you paying for cancellation protection twice?

Benchmark each premium against current market rates to check whether you're paying a loyalty premium. Done manually, this means requesting quotes from multiple insurers for comparable coverage — a time-consuming process.

Inzure automates this by reading your uploaded policy documents and running a full comparison across Danish insurers in 60 seconds, flagging duplicates, coverage gaps, and above-market pricing in one pass.

Step 5: Build an Action Plan

Prioritize identified gaps by severity:

- Address missing critical coverage — family members not listed, essential risks unprotected

- Eliminate duplicate waste — cancel redundant policies you're paying for twice

- Renegotiate or switch overpriced policies — benchmark against market rates and ask for new-customer pricing

For each item, set a deadline and note who to contact and what to request. According to KFST's 2025 analysis, 79% of existing customers who negotiate their current agreements successfully secure a lower price.

Common Mistakes and Misconceptions in Policy Gap Analysis

Most coverage gaps don't come from ignoring insurance altogether — they come from assuming that what you have is still working. These three mistakes are the most common reasons a gap analysis gets skipped or done wrong.

Treating Auto-Renewal as a Coverage Review

Many people treat annual renewal as confirmation that nothing needs to change. In reality, coverage limits, personal circumstances, and market prices may have shifted significantly since the policy was first purchased. Auto-renewal is a billing event, not a coverage review.

Switching to the Cheapest Policy Without Checking Coverage Terms

Switching to the cheapest policy without reviewing coverage terms can close a premium gap while simultaneously opening a coverage gap. The cheapest policy may carry exclusions the previous one did not, or may have lower coverage limits. Price is one variable, not the only variable.

Overlooking Smaller Policies Because the Premiums Seem Minor

Concentrating only on the most expensive policy — such as home insurance — while ignoring smaller ones like travel, contents, or personal liability means gaps in those areas stay hidden until a claim is rejected. A complete review covers every policy, not just the ones with the largest premiums.

A useful way to avoid all three mistakes:

- Treat renewal notices as a trigger to review, not a sign that coverage is current

- Compare coverage terms alongside price — exclusions and limits matter as much as the premium

- List every active policy before starting the analysis, including those with low annual costs

Frequently Asked Questions

What is policy gap analysis?

Policy gap analysis is the process of comparing your current insurance coverage against your actual needs to identify missing protection, duplicate coverage, and overpriced premiums. It reveals where you're underinsured, overinsured, or paying above market rate.

What are the steps in a policy gap analysis?

The five key steps are: inventory your current policies, map your actual risk exposure, compare coverage against needs, identify duplicates and overpricing, and build a prioritized action plan with clear next steps and timelines.

What are the types of policy gap analysis?

The three main types are coverage gaps (missing or insufficient protection), duplicate gaps (overlapping policies wasting premiums), and premium gaps (paying above market rate for identical coverage due to loyalty penalties).

How often should you conduct a policy gap analysis?

Conduct a policy gap analysis at least once a year, and also after any major life change such as a home purchase, new family member, change in income, or significant asset acquisition.

What is the difference between a policy gap analysis and a risk assessment?

A risk assessment identifies potential threats and their likelihood, while a policy gap analysis evaluates whether your existing insurance policies adequately cover those threats. The two tools work together: one defines the risks, the other checks your protection.

What should you do after identifying a gap in your insurance policy?

Prioritize the most critical uncovered risk first, then contact your insurer to request an amendment or additional rider. Before committing, compare alternative policies to verify coverage terms — not just premium cost.