Introduction

Most people with insurance believe they're protected—until something goes wrong. That's when they discover critical gaps in coverage, exclusions they never knew existed, or liability limits set years ago that no longer match their current assets and property value.

Insurance gap analysis is the structured process that reveals the difference. Done properly, it transforms how you assess and manage personal financial risk—showing not just where you're exposed, but where you're paying for duplicate coverage you don't need.

Key Takeaways

- Insurance gap analysis compares your actual financial risks against your existing coverage to find dangerous shortfalls

- The costliest gaps hide in exclusions, outdated valuations, and liability limits that no longer reflect your assets

- A 4-step process—inventory assets, assess risks, review policies, prioritize gaps—gives you a clear action plan

- Being underinsured and overpaying for duplicate coverage are two sides of the same problem that only gap analysis can solve

- Life changes—marriage, new home, children, job change—signal when a full coverage review is most urgent

What Is Insurance Gap Analysis and How Does It Sharpen Risk Assessment?

Insurance gap analysis is a systematic comparison between the risks you actually face and the protection your current policies provide—with the explicit goal of identifying where coverage is insufficient, absent, or redundant. Unlike a casual policy review, it's a structured risk management exercise with a defined output: knowing exactly where you're exposed.

The Relationship Between Risk Assessment and Gap Analysis

Risk assessment identifies and quantifies potential threats by calculating likelihood × financial impact. Gap analysis maps those threats against existing policies. Together, they answer the question every insured person should be asking: "If something goes wrong, how much of this am I actually covered for?"

Without this pairing, you operate under false security. Only 17% of EU consumers hold specific property coverage for natural catastrophes, despite high perceived coverage—a gap that exists precisely because people assume their standard policies protect them when they don't.

Why Individuals Need Gap Analysis as Much as Businesses

For individuals and families, the stakes in insurance gaps are personal — liability claims, property loss, and income disruption from disability can be financially devastating without the right coverage. Standard off-the-shelf policies are built for a generic customer, not your specific circumstances.

Your policy doesn't automatically adjust when:

- Your home increases in value

- Your net worth grows

- Your family expands

Gap analysis surfaces those mismatches before a claim does — so you're not learning about missing coverage at the worst possible moment.

The Most Common Coverage Gaps Hiding in Plain Sight

Coverage gaps aren't rare edge cases—they're built into how standard insurance products are designed. Insurers offer baseline policies that exclude specific events or cap payouts at levels set years ago. The fine print in exclusions and sub-limits is where real vulnerability lives.

Personal Property and Home Valuation Gaps

When a home is insured for its market value or an outdated replacement estimate, the actual rebuilding cost can be higher than expected. Rebuilding requires demolition, code compliance upgrades, and current materials pricing—all of which rise faster than general inflation. In Denmark, construction costs for new residential buildings rose 1.90% year-on-year in March 2024, compounding over time.

The Central Bank of Ireland found that underinsurance in the home insurance market increased from 6.5% in 2017 to 16.5% in 2022—a pattern familiar to Danish homeowners facing the same rising rebuild costs.

Standard homeowners policies also carry another hidden risk: flood and earthquake exclusions. A policy that covers fire and theft but not flooding is only a partial safety net for anyone in a risk-prone area. In Denmark, standard husforsikring covers cloudbursts (skybrud) but strictly excludes flooding from the sea, fjords, or lakes (stormflod). Compensation relies on the state-backed Naturskaderådet scheme, which mandates a 5% deductible with a minimum of 5,000 DKK.

Common valuation and perils gaps to check in your husforsikring:

- Rebuilding value set at purchase price, not current construction cost

- No inflation adjustment clause in the policy

- Stormflod damage excluded (requires separate Naturskaderådet claim)

- Skybrud covered but sub-limits apply to basements and outbuildings

- Earthquake damage excluded without a rider

Liability Limits That Don't Match Your Net Worth

Auto and home policies include liability protection, but the limits are often set at default levels that bear no relationship to your actual net worth or income. If your net worth is higher than your liability ceiling, the difference is directly exposed in the event of a serious lawsuit.

For example, if your homeowner's policy includes 1,000,000 DKK in liability coverage but your net worth is 3,000,000 DKK, a successful lawsuit for 2,500,000 DKK would leave you personally liable for 1,500,000 DKK—potentially wiping out your savings and assets.

The standard mechanism for closing this gap is a personal umbrella policy (ansvarsforsikring med udvidet dækning), which provides additional liability coverage above your home and auto limits. Many people don't know it exists or assume it's only for wealthy households. In reality, umbrella policies are relatively inexpensive and worth considering for anyone with substantial assets or income.

Gaps in Travel and Accident Coverage

Beyond home and liability coverage, Danish consumers frequently discover gaps in two areas that feel like afterthoughts until something goes wrong: travel insurance (rejseforsikring) and accident insurance (ulykkesforsikring).

Travel policies vary widely in what they actually cover. Common gaps include:

- Medical evacuation costs exceeding policy sub-limits

- Adventure sports and activities excluded by default

- Cancellation coverage that doesn't apply to pre-existing conditions

- Delayed baggage reimbursement capped well below actual loss

Accident insurance gaps tend to surface during claims. A standard ulykkesforsikring may cover permanent injury but exclude temporary disability, or cap payouts at levels that don't reflect current costs of rehabilitation. Reviewing the specific definitions of "accident" and "permanent disability" in your policy documents often reveals these distinctions before they matter.

A 4-Step Framework to Conduct Your Own Insurance Gap Analysis

Most households carry insurance without ever confirming what it actually covers. This four-step process changes that—moving from a rough inventory of what you own to a ranked list of specific gaps that need attention.

Step 1: Take Stock of Everything You Own and Owe

The process begins with creating a complete financial inventory:

- All assets: Real estate, vehicles, valuables, savings, investments

- All liabilities: Mortgages, loans, debts

This snapshot defines the total value at risk. Most people underestimate this figure, especially for high-value personal items like jewelry, electronics, or collectibles that have strict sub-limits in standard policies.

For example, your homeowner's policy may cover 1,000,000 DKK in contents, but jewelry might be capped at 20,000 DKK unless you purchase a rider.

Step 2: Map Out Every Meaningful Risk You Face

Risk identification requires brainstorming every scenario that could result in financial loss, tied to specific assets:

- Natural disasters (flooding, storms, cloudbursts)

- Accidents (fire, water damage, theft)

- Liability events (someone injured on your property)

- Personal risks (accident-related disability, loss of income from injury)

The key is to move beyond generic thinking and consider geography, lifestyle, profession, and dependents—factors that make your risk profile unique. A family living near a fjord faces different flood risks than one in central Copenhagen. A consultant faces professional liability risks that a salaried office employee does not.

Step 3: Read Your Policies for What They Actually Cover

Step three requires pulling every policy document and examining four specific elements:

- Coverage limits: The maximum your insurer will pay for a covered loss

- Deductibles: The amount you pay out-of-pocket before coverage kicks in

- Exclusions: Events or situations explicitly not covered

- Endorsements or riders: Additional coverage you've purchased

Few policyholders read past the summary page. The exclusions section is where this step pays off most—it often contains language that voids coverage for scenarios most people assume are included.

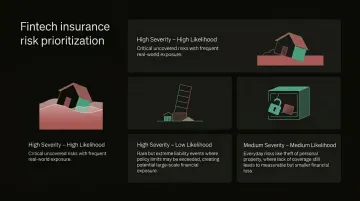

Step 4: Compare, Identify Gaps, and Prioritize

The final step: map risks against coverage to reveal gaps, then rank them by:

- Severity: Financial impact if the event occurs

- Likelihood: Realistic probability

The output is a prioritized gap list with specific amounts attached to each exposure. For example:

- High severity, high likelihood: Flood damage to home (no coverage, 500,000 DKK+ exposure)

- High severity, low likelihood: Liability lawsuit exceeding policy limits (1,500,000 DKK exposure)

- Medium severity, medium likelihood: Bicycle theft (no coverage, 15,000 DKK exposure)

Not every gap demands immediate action. Start with whatever sits at the intersection of high severity and realistic probability—those are the exposures that can genuinely damage your financial position if left uncovered.

The Double Risk: Underinsured and Overpaying Simultaneously

Most conversations focus only on missing coverage, but a proper gap analysis also reveals where you're paying for overlapping or duplicate policies. Both problems cost you money. One leaves you exposed; the other wastes the premiums you're already paying.

The Underinsurance Problem

Underinsurance occurs when coverage limits are lower than the actual potential loss. This is extremely common because most policies are set up once and never revisited as asset values rise or circumstances change.

Global property underinsurance is estimated at $221 billion annually. In Denmark, nearly 20% of young adults aged 18-30 lack basic contents insurance (indboforsikring)—leaving them entirely exposed to theft, fire, or water damage.

The Overinsurance and Duplication Problem

Duplicate coverage occurs when multiple policies cover the same risk. Examples include:

- Travel insurance included in a credit card benefit that overlaps with a separately purchased travel policy

- Home contents coverage that duplicates a renters policy

- Bicycle theft coverage purchased separately when it's already included in your home policy

These overlaps cost money while providing no additional protection — funds that could close real coverage gaps instead.

The Loyalty Premium Trap

The "loyalty tax" is structural in the insurance industry, not random. Insurers frequently raise premiums gradually for long-standing customers while offering significantly lower rates to new customers for equivalent coverage.

The Danish data makes this concrete:

- A 2025 report by the Danish Competition and Consumer Authority (KFST) found that loyal customers with 10+ years of seniority pay margins 30-35 percentage points higher for home and contents insurance than new customers

- In the UK, the FCA found that in 2018, 6 million loyal policyholders overpaid by £1.2 billion — a pattern regulators across Europe have since moved to address

Comparing your current premium against live market prices for identical coverage is how that 30-35 point margin gap becomes visible — and actionable.

Key Life Events That Should Trigger an Immediate Gap Analysis

Insurance needs are not static—risk profiles change dramatically when major life events occur. A policy that was adequate three years ago may have significant gaps today.

These events typically warrant an immediate review:

- Getting married or divorced shifts asset ownership, liability exposure, and who needs to be covered

- Having children raises accident risk, household liability, and the scale of assets worth protecting

- Purchasing a home or significant asset requires updated property and liability limits

- Moving to a new address changes local risk factors, theft rates, and coverage requirements

- Receiving an inheritance increases net worth and the liability exposure that comes with it

- Major income changes affect how much coverage is appropriate across your household policies

Triggered reviews catch the gaps that gradual life changes quietly create. But life events aren't the only reason to look closer.

The Case for Routine Annual Reviews

Even without a triggering event, a routine annual review is a baseline habit. Premium increases, policy renewals, and changes in local risk factors (climate events, neighborhood changes) can all quietly erode coverage adequacy over time.

The data suggests most Danish households aren't reviewing often enough. Over half of Danish consumers obtained a quote within the last 2 years, but more than 25% haven't done so in over 5 years, and 10% never have.

How Inzure Enables Continuous Monitoring

Inzure monitors your policies continuously, flagging premium increases, coverage gaps, and better market options as they appear. Danish consumers don't need to wait for a life event to find out they're underinsured or overpaying. Inzure's AI analysis scans policies across Danish insurers, identifying gaps, duplicates, and price discrepancies in 60 seconds.

How AI-Powered Tools Are Transforming Coverage Gap Analysis

Traditional gap analysis required manually gathering policy documents, reading dense legal language, and either consulting a professional or spending hours comparing coverage on your own. AI-powered platforms now automate policy reading, risk comparison, and gap identification at scale — cutting a process that once took hours down to seconds.

The results across the industry are measurable. Insurer AI deployments have cut complex assessment timelines by weeks and improved document routing accuracy by 30%, according to McKinsey's analysis of AI in insurance. An EY case study of a Nordic insurer found that 70% of policy documents are correctly extracted and interpreted automatically using AI.

Specific Capabilities That Make AI Gap Analysis More Effective

AI platforms excel at tasks that are difficult or time-consuming to do manually:

- Cross-referencing policy language against databases of known exclusions and industry benchmarks

- Detecting subtle wording differences between policies that create coverage gaps

- Flagging duplicate coverage across multiple products

- Comparing individual premiums against real-time market pricing

The Independence Factor

Independence is critical to genuine gap analysis value. Tools or advisors tied to specific insurers have an inherent conflict of interest when recommending coverage changes. An independent platform with no financial ties to insurers provides analysis aligned with the consumer's actual needs, not a sales quota.

Inzure is built on this principle. As an independent Danish platform, it earns revenue only when users switch and save (20% of annual savings) — meaning there's no incentive to recommend a change unless it genuinely benefits the consumer.

Frequently Asked Questions

What is insurance gap analysis?

Insurance gap analysis is a structured review that compares your actual financial risks and assets against your existing insurance policies, identifying where your coverage is insufficient, absent, or duplicated. The goal is to take targeted action to close those exposures before a loss occurs.

What is coverage gap analysis?

Coverage gap analysis examines the terms, limits, exclusions, and valuations within your current policies to determine precisely where your protection falls short of your real exposure. This goes beyond simply knowing which policies you hold — it's about understanding what they actually cover.

What are the 4 steps in a gap analysis?

The four steps are: (1) inventory all assets and liabilities, (2) identify and assess your realistic risks, (3) review your existing policies for limits, exclusions, and conditions, and (4) compare your risk map against your coverage to pinpoint and prioritize gaps.

What are the four types of gap analysis?

The four main types relevant to insurance are: limit gaps (coverage ceiling is too low), peril gaps (certain events are excluded), valuation gaps (insured value doesn't reflect true replacement cost), and time element gaps (for example, travel insurance that doesn't cover an extended delay, or home insurance that won't fund temporary accommodation during repairs).

Do I actually need gap insurance?

In everyday usage, "gap insurance" refers to coverage that fills the space between what your current policy pays out and what you actually need. For Danish households, this often means discovering that a home policy doesn't fully cover contents replacement, or that a travel policy excludes a specific activity. Insurance gap analysis is the process of finding and closing those shortfalls across all your personal policies.

What is a needs gap analysis?

A needs gap analysis evaluates the difference between the coverage a household actually requires — based on their home, belongings, travel habits, and family situation — and what their current policies provide. It forms the foundation for building a complete and appropriate insurance portfolio.