Introduction

Accidents don't send a warning. A slip on ice, a cycling collision, or a kitchen burn can happen in seconds—and the bills that follow can stretch for months. Even with Denmark's public healthcare system covering acute treatment, the hidden costs add up fast: physiotherapy co-payments, lost income during recovery, transportation to appointments, and dental repairs outside public coverage.

Standard health insurance (sundhedsforsikring) covers illness and chronic conditions, but it often leaves gaps when an accident strikes. Deductibles, rehabilitation expenses, and everyday costs while you're unable to work can pile up quickly.

That's where accident insurance steps in. The problem is that "accident insurance," "accidental death insurance," and "health insurance" all sound similar, yet they serve completely different purposes. Choosing the wrong one—or missing coverage entirely—can mean thousands of kroner out of pocket.

This guide breaks down what each type actually covers, how they interact with your existing policies, and what to look for when choosing the right protection for your situation.

Key Takeaways

- Personal accident insurance pays cash benefits directly to you for covered injuries like fractures, burns, and hospitalization—use it alongside health insurance, not instead of it

- AD&D insurance pays a lump sum for accidental death or severe dismemberment, but offers little for non-fatal injuries

- Health insurance covers illness and chronic conditions but typically leaves gaps in deductibles, copays, and rehabilitation that accident insurance fills

- Your best fit depends on your lifestyle, existing coverage, and financial resilience

- Many people benefit from holding both personal accident and AD&D coverage together

- Comparing policies side by side prevents overpaying or underinsuring yourself

Accident Insurance vs. Accidental Death Insurance: Quick Comparison

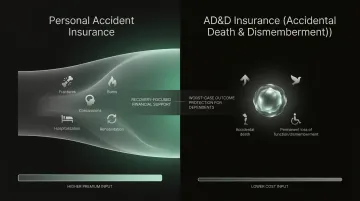

Understanding the difference between personal accident insurance (Ulykkesforsikring) and accidental death and dismemberment (AD&D) insurance is essential before making any purchase. Both fall under the "accident insurance" umbrella, but they serve distinct financial purposes.

| Dimension | Personal Accident Insurance | AD&D Insurance |

|---|---|---|

| Coverage Scope | Non-fatal injuries from accidents: fractures, burns, concussions, emergency treatment, hospitalization, rehabilitation | Death or severe permanent outcomes: loss of limb, sight, paralysis caused by an accident |

| Payout Structure | Scaled to injury severity (minor injury = smaller payout; paralysis or coma = significantly higher) | Predetermined lump sum for accidental death; percentage of that sum for dismemberment |

| Primary Purpose | Financial cushion for medical treatment, recovery costs, and daily living expenses while injured | Financial protection for your family if you die accidentally, or for you if you suffer permanent loss of function |

| Cost | Generally higher premiums due to broader coverage scenarios | Lower premiums because it covers fewer, more specific events |

| Best For | Anyone with an active lifestyle, family dependents, or high-deductible health plan | People seeking affordable worst-case outcome protection, often added as a life insurance rider |

Coverage Scope

Personal accident insurance addresses the injuries most people actually experience: a broken arm from a fall, a concussion from a cycling accident, burns from a kitchen mishap. It covers emergency room visits, X-rays, hospitalization, surgery, and rehabilitation.

AD&D insurance focuses exclusively on catastrophic outcomes: death or the permanent loss of a limb, eyesight, or mobility.

Payout Structure

Personal accident policies pay benefits based on injury severity. A fractured wrist might trigger a payment of 10,000–15,000 DKK, while total disability could pay hundreds of thousands. AD&D policies pay a fixed lump sum (often 500,000–1,000,000 DKK) for accidental death, or a percentage for dismemberment: 50% for loss of one hand, 100% for loss of both.

Cost & Affordability

AD&D premiums are typically lower, often 50–100 DKK per month, since they cover only extreme scenarios. Personal accident insurance costs more (150–300 DKK monthly for standard coverage) due to the broader range of events covered. For most Danish households, the right choice depends on whether you need everyday injury protection or a safety net for worst-case outcomes only.

What is Personal Accident Insurance?

Personal accident insurance (Ulykkesforsikring) is a supplemental insurance product that pays cash benefits directly to you when you suffer an injury covered by the policy as the result of an accident. It does not replace health insurance—it fills the financial gaps health insurance leaves behind.

How it works:

- You pay monthly premiums (typically 150–300 DKK for standard coverage)

- A covered accident occurs (fracture, burn, concussion)

- You file a claim with medical documentation

- The insurer pays cash directly to you (not to the hospital or doctor)

- You use the cash for any expense—medical bills, rent, childcare, lost income

Main categories of coverage commonly included:

- Ambulance, ER visits, X-rays, and diagnostic imaging

- Fractures, burns, concussions, and dental trauma

- Hospitalization benefits paid per day

- Surgical procedures required as a direct result of an accident

- Physiotherapy and chiropractic care (up to 12 months post-injury)

- Accidental death benefit, either built-in or as an add-on

Policy terms differ meaningfully between Danish providers like Tryg, Alka, and Topdanmark — the same injury can trigger full payout under one policy and partial payment under another.

Standard exclusions:

- Injuries from illness or disease

- Self-inflicted harm

- Injuries sustained under the influence of alcohol or drugs

- Injuries from illegal activities

Danish accident insurance policies generally have no waiting period—coverage begins immediately or within a few days of approval, unlike health insurance, which can impose waiting periods of up to 90 days.

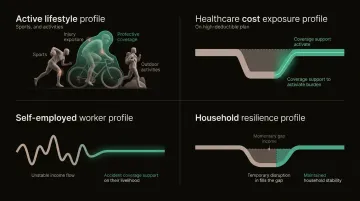

Who Typically Benefits Most from Personal Accident Insurance

Personal accident insurance provides the most value for:

- Sports enthusiasts, cyclists, and outdoor activity participants with higher injury exposure

- People in high-deductible health plans facing large out-of-pocket costs before coverage kicks in

- Self-employed workers without employer-provided sick pay

- Households that couldn't absorb several weeks of lost income after an accident

A broken leg treated in Denmark can cost 15,000–25,000 DKK in total expenses when accounting for physiotherapy, transportation, and lost income. For a household earning median Danish wages, that represents three to five weeks of take-home pay absorbed with no safety net.

What is Accidental Death & Dismemberment (AD&D) Insurance?

AD&D insurance pays a lump sum to your designated beneficiaries if you die in an accident, or pays you directly if you suffer dismemberment (loss of a limb, sight, or other serious permanent injury) from an accident. It does not cover death from illness, natural causes, or pre-existing conditions.

Typical payout structure:

- Accidental death: Full benefit amount (e.g., 500.000–1.000.000 kr.)

- Dismemberment: Percentage of full benefit based on severity:

- Loss of one hand or foot: 50%

- Loss of both hands or feet: 100%

- Total blindness: 100%

- Partial blindness in one eye: 25%

AD&D does not cover medical expenses from non-fatal injuries. Break your leg, and AD&D pays nothing — only personal accident insurance addresses injury-related costs short of death or dismemberment.

Common exclusions:

- Deaths from risky or extreme activities (skydiving, BASE jumping)

- Illegal acts

- Substance abuse

- Suicide

This limited scope keeps AD&D premiums lower than personal accident or life insurance.

When AD&D Makes Sense as Part of Your Coverage Portfolio

AD&D is most commonly purchased as a rider attached to a life insurance policy rather than as a standalone product, making it cost-effective for people who want extra financial protection for their family without upgrading their full life insurance coverage.

The right product depends on your primary concern. AD&D makes sense when your family needs a financial safety net in the event of accidental death. If your bigger worry is recovering financially from a non-fatal injury — covering treatment, rehabilitation, or lost income — personal accident insurance is the more relevant choice.

How Does Accident Insurance Differ from Health Insurance?

Health insurance (sundhedsforsikring) pays healthcare providers directly for a broad range of events: illness, chronic conditions, injury, and preventive care. Accident insurance is supplemental. It pays cash directly to you for accident-specific costs that health insurance doesn't fully cover.

Three practical distinctions that matter most:

- Who gets paid: Accident insurance pays you directly in cash; health insurance pays the provider

- When coverage starts: Health insurance can have a 6-12 month waiting period for pre-existing conditions; accident insurance typically starts immediately with no waiting period

- What's covered: Health insurance covers illness and chronic disease; accident insurance covers only accident-related injuries

Why Carry Both?

Even with solid health insurance, an accident can leave you covering costs your policy doesn't touch:

- Deductibles and copays

- Lost wages during recovery

- Transportation to medical appointments

- Childcare while you're unable to work

- Rehabilitation not covered by public vederlagsfri fysioterapi

The Danish public system covers acute hospital care, but rehabilitation often requires co-payments unless you meet strict criteria for free physiotherapy. Private accident insurance fills this gap, covering treatment costs for typically up to 12 months.

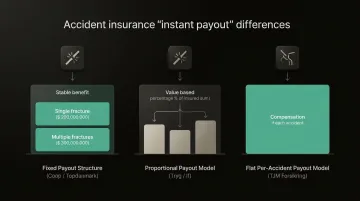

What is Strakserstatning (Immediate Compensation)?

One of the most valuable features of Danish accident insurance is strakserstatning—immediate compensation paid as a fixed lump sum upon medical documentation of specific severe injuries. This benefit bridges the financial gap in the weeks immediately after a severe accident — well before a final permanent impairment (varigt mén) rating can be assessed.

Qualifying injuries typically include:

- Bone fractures (skull, collarbone, arm, leg)

- Completely or partially torn cruciate ligaments

- Totally torn Achilles tendons

- Totally torn collateral ligaments in the knee

Payout structures vary by insurer:

| Insurer | Strakserstatning Payout |

|---|---|

| Coop / Topdanmark | 12,000 DKK for one fracture; 18,000 DKK for multiple simultaneous fractures |

| Tryg / If | 1% of total insured sum |

| TJM Forsikring | 12,000 DKK per accident |

This payout typically arrives within 10-14 days of medical documentation, helping households cover immediate costs like transportation, specialized equipment, or lost income during acute recovery. Crucially, the benefit is paid regardless of whether the injury ultimately results in permanent impairment — a varigt mén rating can only be assessed once a condition has stabilized, often 12 months or more after the accident. Where strakserstatning delivers immediate liquidity, varigt mén addresses long-term life alteration.

Which Type of Accident Insurance Is Right for You?

There is no universal "best" type—the right choice depends on three factors:

- What existing coverage you already have — employer-provided group accident insurance, health insurance, life insurance

- Your lifestyle and risk profile — active sports participation, cycling commute, physical job

- Your financial resilience — how much unexpected expense you could absorb without hardship

Situational Guidance

Choose personal accident insurance if:

- Your primary concern is covering medical and recovery costs from injuries

- You have a high-deductible health plan

- You're self-employed without sick pay

- You participate in active sports or outdoor activities

- You couldn't cover several weeks of lost income

Choose AD&D if:

- You want affordable protection for your family against worst-case outcomes

- You already have health insurance

- Your main concern is leaving your family financially secure if you die accidentally

If neither option alone fits, a combination may make sense. Consider both if:

- You have an active lifestyle and dependents

- You have a high-deductible health plan

- You want comprehensive protection covering both recovery costs and catastrophic outcomes

Common Mistakes to Avoid

- Buying the cheapest policy without checking exclusions — a low premium means nothing if the policy doesn't pay when you need it

- Duplicating coverage that already exists — many employer group plans provide accident or AD&D coverage; purchasing a separate policy may be redundant

- Failing to reassess coverage as life changes — marriage, children, job changes, or income increases should trigger a coverage review

The Role of Policy Comparison

Premium costs, coverage limits, exclusions, and claim settlement speed vary significantly between Danish providers like Tryg, Alka, and Topdanmark. Two policies that appear similar on the surface may differ considerably in what they actually pay out. Most consumers decide based on one provider's offer rather than a market-wide comparison—which means overpaying becomes the default.

Inzure addresses this directly. Upload your policy documents and the platform analyzes your coverage in 60 seconds—identifying gaps, overlaps, and whether you're missing coverage like rehabilitation benefits or strakserstatning. It then maps your policy against current pricing from Danish insurers so you can see what the market actually charges for equivalent cover. The analysis is free with no obligation to switch; you only pay 20% of the annual savings if you choose a better policy.

Conclusion

Personal accident insurance and AD&D insurance are both useful, but they solve different problems. Accident insurance covers you during recovery from injury—paying for medical bills, rehabilitation, and lost income. AD&D protects your family in worst-case scenarios: death or permanent dismemberment. Understanding which risk each policy addresses is the first step toward knowing whether your current coverage actually protects you.

From there, the practical question is whether your full coverage picture holds together — or whether you're paying for overlapping policies while a real gap goes unnoticed. Upload your policy documents to Inzure in 60 seconds and get a clear breakdown of what you're covered for, what you're missing, and what the market actually charges for the same coverage.

Frequently Asked Questions

How much is personal accident cover per month?

Personal accident insurance premiums in Denmark typically range from 150–300 DKK per month, depending on your age, coverage level, lifestyle risk, and provider. More comprehensive policies with higher benefit limits and additional features like strakserstatning cost more.

Is there a waiting period for personal accident insurance?

Personal accident insurance typically has no waiting period, and coverage begins immediately or within a few days of approval. Unlike health insurance, which can impose waiting periods of 6-12 months for pre-existing conditions.

What are the different types of accident insurance?

The main types are personal accident insurance (covers injury costs), accidental death and dismemberment (AD&D) insurance (covers death or permanent loss), and group accident insurance (employer-provided). Riders can expand coverage to include dental trauma, increased rehabilitation limits, and similar benefits.

What is the difference between personal accident insurance and group personal accident insurance?

Personal accident insurance is purchased individually and tailored to your needs, while group accident insurance is employer- or organization-provided. Group plans are typically less flexible but cost less due to shared risk pricing.

Does accident insurance cover surgery?

Most personal accident insurance policies include surgical care as a covered benefit when surgery is required due to a covered accidental injury. Coverage details vary by policy — always check the benefit schedule before purchasing.

Is accident insurance worth it?

Accident insurance is worth considering if you have a high-deductible health plan, an active lifestyle, or a limited financial buffer. At 150–300 DKK per month, it's affordable protection — and a single serious injury can easily cost tens of thousands of kroner out of pocket.