Introduction

You're planning your third trip of the year and staring at another single-trip travel insurance purchase screen. Should you just buy this one policy, or is it finally time to switch to annual coverage? The decision isn't as simple as counting trips.

Choosing the wrong policy type means either overpaying for coverage you don't use or, worse, being underprotected during a medical emergency abroad. Danish insurers rarely make this choice easy to navigate, with pricing structures that obscure the real value of each option and exclusions buried in policy documents.

TL;DR

- Single-trip policies cover one journey with fresh coverage limits and typically include trip cancellation as standard or add-on

- Annual multi-trip policies cover unlimited trips over 12 months, but cap each trip at 30–90 days and often exclude cancellation

- Break-even point: approximately 2 trips per year in the Danish market, though price alone shouldn't decide

- Pre-existing conditions require separate medical pre-assessment on annual plans — same as single-trip

- Trip length, cancellation risk, and health history matter more than the headline price

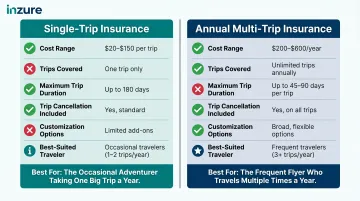

Annual vs. Single-Trip: Quick Comparison

| Feature | Single-Trip | Annual Multi-Trip |

|---|---|---|

| Typical cost range | 156-198 DKK (Europe, 1 week); 221-801 DKK (Worldwide) | 280-453 DKK/year (Europe coverage) |

| Number of trips covered | One specific journey | Unlimited trips within 12 months |

| Maximum trip duration | Up to 18-24 months (Tryg, Europæiske ERV) | 30-90 days per trip depending on insurer |

| Trip cancellation coverage | Often included or available as add-on | Typically excluded; purchased separately |

| Pre-existing condition coverage | Medical pre-assessment required (same process as annual) | Medical pre-assessment required; no structural difference |

| Customization/add-ons | Winter sports, baggage, adventure activities, travel accident | Limited; cancellation must be purchased separately |

| Best suited for | 1-2 trips/year; long journeys (45+ days); high trip costs; pre-existing conditions | 3+ shorter trips/year; low per-trip costs; spontaneous travelers |

Worth checking: Some annual plans use aggregate benefit pools shared across all trips. A large claim early in the year can reduce the coverage available for trips later — check whether your policy resets per trip or draws from a single annual limit.

What is Single-Trip Travel Insurance?

Single-trip travel insurance covers one specific journey from departure to return, with coverage limits that reset freshly for that trip alone. This reset matters when trip costs are high — a €4,000 family holiday gets its own full coverage pool, not a share of an annual aggregate limit.

Standard coverage typically includes:

- Emergency medical treatment (illness, injury, hospitalization, emergency dental)

- Repatriation and medical evacuation

- Baggage delay, loss, or damage

- Travel delays and missed connections

- Private liability coverage

- Search, rescue, and crisis assistance

Single-trip plans typically include trip cancellation as a standard feature or optional add-on, covering non-refundable expenses if illness, injury, or another covered event forces you to cancel.

Customization advantages:

Danish single-trip policies allow add-ons such as:

- Winter sports and skiing coverage

- Adventure sports protection

- Enhanced baggage coverage (theft, damage, delayed replacement)

- Sports equipment protection (damaged, delayed, stolen; includes rental replacement)

- Travel accident insurance (permanent disability or death)

Note: Cancel-for-Any-Reason (CFAR) coverage — common in US markets — Danish insurers do not offer. Danish cancellation insurance covers specific named perils — acute illness, death of a family member, unexpected job loss, mandatory re-examinations — not open-ended cancellation.

Use Cases of Single-Trip Insurance

Best suited for:

- Travelers taking 1–2 trips per year

- High-value trips with substantial non-refundable costs (flights, hotels, tours)

- Long journeys exceeding 45–90 days (sabbaticals, extended holidays)

- Travelers with pre-existing medical conditions requiring pre-assessment coverage

Real-world example: A Danish family books a two-week summer holiday to Greece with €4,000 in prepaid costs — flights, hotel, and guided tours. If a family member falls seriously ill before departure, trip cancellation coverage on a single-trip policy directly reimburses those non-refundable expenses.

An annual plan without a cancellation add-on would leave the family bearing the full €4,000 loss.

What is Annual Multi-Trip Travel Insurance?

Annual (multi-trip) travel insurance covers unlimited trips taken within a 12-month period, subject to a per-trip duration cap. The "unlimited trips" headline is misleading if you don't scrutinize the duration limit.

Per-trip duration caps in the Danish market:

- IF: 30 days (Travel basic) or 60 days (Travel Super)

- Alka (Tryg): 60 days maximum; cannot extend beyond 60 days

- Topdanmark: 60 consecutive days

- Codan: Choice of 30, 60, or 90 days per trip

- Gjensidige: 60 days

- Europæiske ERV: 30 days per trip

Standard coverage typically includes:

- Emergency medical expenses and evacuation

- Repatriation

- Baggage delay

- Travel delays and missed connections

- Private liability

- 24/7 Danish-speaking emergency assistance

What's commonly excluded:

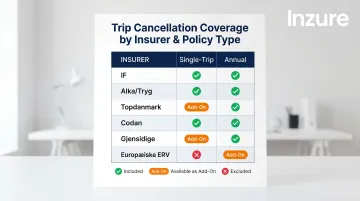

- Trip cancellation coverage (sold separately at most insurers; exceptions: IF Travel Plus/Super and Gjensidige include it as standard)

- Most customizable add-ons available on single-trip policies

- Coverage for trips exceeding the per-trip duration cap

Unlike single-trip policies where limits reset each trip, annual plans may share one total coverage cap across all trips in the year. A large medical claim in January could reduce available protection for later journeys. Always check whether limits are per-trip or aggregate when comparing policies.

Use Cases of Annual Multi-Trip Insurance

Knowing how the product works helps identify who it actually suits. Annual policies are best suited for:

- Frequent travelers taking 3+ shorter trips per year (business travelers, families visiting relatives, weekend enthusiasts)

- Travelers whose individual trips are low-cost without large prepaid non-refundable expenses

- Those who value convenience and always-on coverage without purchasing new policies

Once purchased, annual policies cover last-minute and unplanned trips automatically. For people with unpredictable travel schedules, this removes the friction of arranging cover before each departure.

All major Danish insurers structure annual policies to cover the entire household — everyone registered at the same address. This includes spouses, partners, and children living at home or away (typically under 18–21). Coverage applies even when family members travel to different destinations simultaneously, which is a meaningful cost advantage for families.

Annual vs. Single-Trip Cost Breakdown: Where Is the Break-Even Point?

Current pricing in the Danish market:

| Scenario | Single-Trip Cost | Annual Plan Cost | Break-Even |

|---|---|---|---|

| 1 trip (Europe, 1 week) | 156-198 DKK | 280-453 DKK/year | Annual not cost-effective |

| 2 trips (Europe, 1 week each) | 312-396 DKK total | 280-453 DKK/year | Annual becomes cheaper |

| 3+ trips (Europe, 1 week each) | 468-594+ DKK total | 280-453 DKK/year | Annual significantly cheaper |

| 1 trip (Worldwide, 1 week) | 221-801 DKK | 280-453 DKK/year (Europe only) | Depends on zone; worldwide annual plan required |

Break-even insight: Europæiske ERV states that annual coverage is typically cheapest if you travel more than 7 days total per year. In the Danish market, the break-even point is approximately 2 trips per year for Europe-only coverage.

The 4–8% pricing rule:

Single-trip policies are typically priced as 4–8% of total insured trip value. On a high-cost trip, this percentage-based pricing generates higher premiums. For example, a DKK 20,000 trip would cost approximately DKK 800–1,600 in single-trip insurance.

Annual policies charge a flat annual rate regardless of trip value, making them a relative bargain for frequent, lower-cost trips but a poor fit for one expensive journey.

The per-trip duration trap:

If your annual plan caps trips at 30 days and you take a 45-day journey, you're uninsured for the final 15 days. Alka explicitly states it "cannot extend coverage beyond 60 days." This gap costs nothing extra on a single-trip policy but requires purchasing a separate policy mid-trip on an annual plan.

Example: A traveler on a 75-day backpacking trip with a 60-day annual plan would face 15 days of complete exposure to medical emergencies, evacuation costs, and liability — tens of thousands of kroner in uncovered expenses.

Hidden cost of aggregate limits:

A large claim early in the year can significantly reduce available coverage for subsequent trips. If you require emergency evacuation in February that depletes a shared medical limit, your summer holiday may have reduced protection. This makes the nominal annual price misleading when assessing total protection value.

These hidden variables make comparing single-trip and annual plans genuinely difficult without the right tools. Inzure analyses your existing travel policy — whether single-trip or annual — and shows whether you're paying market rate or overpaying. It flags duplicate coverage (such as protections already provided by credit cards or the Danish public health card for EU travel), identifies coverage gaps, and compares pricing across Danish insurers.

Beyond Price: 5 Factors That Should Influence Your Choice

1. Pre-Existing Medical Conditions

Both single-trip and annual policies in the Danish market require medical pre-assessment (medicinsk forhåndsvurdering) for travelers with chronic or recent illnesses. This assessment, typically conducted through SOS International, provides binding advance approval for specific conditions.

Key requirements:

- Europæiske ERV recommends applying at least 2 weeks before departure or trip purchase

- Codan generally excludes conditions with symptoms within 2 months prior to travel or booking without pre-assessment

- Coverage applies to "acutely arising" illness; chronic conditions require assessment

Pre-existing condition coverage works the same way regardless of policy type in Denmark. Both single-trip and annual plans require the same medical pre-assessment process before departure.

2. Trip Cancellation Risk and Trip Value

If you're booking expensive, non-refundable holidays (flights, cruises, guided tours), trip cancellation coverage delivers essential financial protection. Europeans spent an average of EUR 1,053 per person on foreign trips in 2024, representing significant exposure if cancellation occurs.

Coverage patterns in Denmark:

- Single-trip policies: Cancellation often included or readily available as add-on

- Annual policies: Cancellation typically excluded; sold separately at Tryg, Alka, Topdanmark, and Codan

- Exceptions: IF includes cancellation in Travel Plus/Super tiers; Gjensidige includes it as standard

Critical timing requirement: Topdanmark requires cancellation insurance to be purchased at least 14 days before departure and before the trip is paid for. Missing this window eliminates cancellation protection entirely.

Annual plans that omit cancellation leave you bearing the full financial risk. That exposure can easily exceed whatever you saved by choosing annual over single-trip coverage.

3. Age and Eligibility Restrictions

Many annual plans impose upper age limits or premium surcharges:

- Europæiske ERV applies premium surcharges starting at age 60 and markets dedicated senior travel insurance for those over 70

- UK insurers commonly cap annual coverage around age 74, though single-trip policies remain available with no upper limit

Single-trip plans typically carry higher or no age caps and can be tailored per destination — a practical advantage for older travelers.

4. Destination Zone Coverage

Annual plans typically require choosing between Europe-only and Worldwide zones:

- Europe-only option: Lower cost; available at IF, Topdanmark, Codan, Gjensidige, Europæiske ERV

- Worldwide option: Higher cost; necessary for travel outside Europe

- Alka exception: Offers only worldwide coverage (no cheaper Europe option)

Single-trip policies allow destination selection per journey, avoiding overpayment for worldwide coverage when you're only traveling within Europe.

5. Trip Duration Flexibility

Duration caps are where annual plans hit a hard wall. Most cap individual trips at 30–90 days depending on the insurer and tier — fine for standard holidays, but unworkable for longer travel.

Single-trip policies:

- Tryg: Up to 18 months, extendable

- Europæiske ERV: 1 day to 24 months

Annual policies:

- Capped at 30–90 days per trip depending on insurer and tier

For sabbaticals, extended backpacking, or long-term stays abroad, a single-trip policy is the only viable option.

Conclusion

There's no universal winner in the annual vs. single-trip debate. Single-trip insurance delivers more comprehensive, customizable protection per journey and suits travelers with fewer trips involving significant prepaid costs or specific medical needs. Annual insurance offers unbeatable convenience and cost efficiency for frequent, shorter trips with lower individual financial risk.

What costs travelers most isn't picking the wrong policy type — it's buying any policy without understanding what it excludes. Trip cancellation coverage, per-trip duration caps, and pre-existing condition requirements vary widely between insurers and policy types. Those gaps can cost far more than any premium savings.

Independent comparison is the clearest way to check whether your policy actually matches your needs. Use Inzure to analyze your travel insurance against what Danish carriers currently charge. Upload your policy in 60 seconds to identify coverage gaps, duplicate protections, and whether you're overpaying.

Frequently Asked Questions

Why is annual multi-trip travel insurance often cheaper than single-trip insurance?

Annual plans are cheaper per trip because they focus primarily on emergency medical coverage and exclude more expensive benefits like trip cancellation, comprehensive add-ons, and longer trip durations. Lower insurer risk across shorter, simpler trips translates to a lower flat annual premium.

How much does travel insurance cost for a DKK 20,000 trip?

Single-trip policies typically cost 4–8% of total insured trip value. On a DKK 20,000 trip, expect approximately DKK 800–1,600 depending on traveler age, destination, and coverage selected. Annual plans aren't priced based on trip value, making them unsuitable for one high-cost journey.

Should I buy annual (multi-trip) or single-trip travel insurance?

The decision depends on travel frequency, trip length, and trip cost. Choose annual if you take 3+ shorter trips per year without major cancellation risk. Choose single-trip for high-value journeys, long trips (45+ days), or expensive prepaid costs that require comprehensive cancellation protection.

Should I buy individual or family travel insurance, and how do the plans differ?

In the Danish market, annual policies are structured as household plans covering everyone at the same registered address, while individual plans cover only one person. Danish annual plans automatically provide family coverage at no extra cost, so the choice comes down to whether you need coverage for one person or your full household.

Can I get travel insurance if I have a pre-existing medical condition such as diabetes, gallstones, or pancreatitis?

Yes, travel insurance is available with pre-existing conditions, but coverage requires medical pre-assessment (medicinsk forhåndsvurdering) through your insurer's alarm center. Apply at least 2 weeks before departure. Both single-trip and annual plans use the same assessment process in Denmark — the process is the same regardless of policy type.