The core dilemma: single-trip policies offer comprehensive protection for one journey, while annual multi-trip policies promise convenience and savings for frequent travelers. Most insurers never clearly explain which option actually matches your travel patterns — or what coverage you're sacrificing when you choose the cheaper option.

Key Takeaways

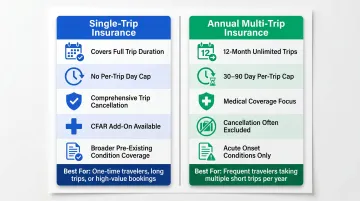

- Single-trip plans cover one journey; annual plans cover unlimited trips within 12 months, with per-trip duration caps of typically 30–90 days

- Annual plans pay off at roughly 3+ trips per year, but often exclude trip cancellation and Cancel for Any Reason coverage

- Single-trip policies typically cost 4–8% of total trip value; annual plans vary by insurer — compare Danish carriers like Tryg, Alka, and Topdanmark for current rates

- If any trip exceeds your annual plan's duration cap, you'll need supplementary single-trip coverage to close that gap

- Pre-existing condition coverage favors single-trip plans, which offer broader waivers versus annual plans' acute-onset-only restrictions

Single-Trip vs. Annual Travel Insurance: Quick Comparison

| Dimension | Single-Trip | Annual Multi-Trip |

|---|---|---|

| Coverage Duration | Departure to return, one trip only | 12 months, unlimited trips |

| Per-Trip Duration Cap | None (can cover trips up to 18 months with insurers like Tryg) | 30, 60, or 90 days per trip (Codan offers these tiers) |

| Trip Cancellation | Comprehensive; higher limits; covers prepaid non-refundable costs | Often excluded or available only as optional upgrade with lower limits |

| Medical Coverage | Strong emergency medical and evacuation coverage | Primary focus; strong medical/evacuation coverage with aggregate annual limits |

| Cancel for Any Reason (CFAR) | Available as add-on on comprehensive plans | Typically not available |

| Pre-Existing Conditions | 2-month look-back period standard; SOS International pre-assessment available for Danish policyholders | Limited to acute onset only; stricter eligibility |

| Baggage Coverage | Included as standard with higher limits | Included but often limited; varies by plan |

| Best Suited For | 1–2 annual trips, high-value bookings, trips >45 days, travelers with chronic conditions | 3+ annual trips, each under 30–90 days, medical coverage priority, frequent business/leisure travelers |

One detail buried in annual plan marketing deserves attention: "unlimited trips" does not mean unlimited trip length. Danish insurer Codan covers only the first 30, 60, or 90 days per trip depending on your tier — exceed that cap and coverage stops without warning mid-trip.

What is Single-Trip Travel Insurance?

Single-trip travel insurance covers one specific journey from departure to return, for however long that trip lasts. It's a straightforward fit when you travel infrequently or when a single trip carries enough financial risk to justify dedicated coverage.

Core coverage includes:

- Reimburses prepaid, non-refundable costs if you cancel before departure or cut a trip short

- Covers emergency medical treatment, hospital stays, evacuation, and repatriation (standard across Danish insurers like Codan and Tryg)

- Pays out for baggage loss and delay — Codan covers delayed baggage after 6 hours for up to 4 days

- Allows optional add-ons: Cancel for Any Reason (CFAR), adventure sports coverage, winter sports supplements

Each single-trip policy starts with full coverage limits — they don't carry over or deplete across trips, unlike annual plans with aggregate caps.

When Single-Trip Insurance Makes Sense

The type of trip matters as much as the number. Single-trip policies tend to be the better fit when:

- You travel 1–2 times a year — buying separate single-trip policies costs less than an annual plan at that frequency

- The trip runs longer than 45 days — annual plans cap individual trips at 30–90 days, leaving extended travelers without cover (Tryg's single-trip policies extend to 18 months)

- You've booked cruises, luxury tours, or package holidays with large non-refundable deposits where cancellation protection is non-negotiable

- You have pre-existing conditions — Danish insurers offer medical pre-assessment through SOS International, and single-trip plans generally provide broader coverage than the acute-onset-only restrictions common in annual plans

Concrete example: A two-week European cruise with €5,000 in prepaid costs. At 4–8% of trip cost, a single-trip policy runs approximately €200–400. That protects the full €5,000 through cancellation coverage and CFAR add-ons, coverage that annual plans often exclude or sharply limit.

What is Annual Multi-Trip Travel Insurance?

Annual multi-trip insurance covers unlimited trips within a 12-month period, with each individual trip capped at a provider-specified maximum — commonly 30, 45, 60, or 90 days per trip. Codan allows Danish consumers to select caps of 30, 60, or 90 days, providing flexibility for different travel patterns.

Think of it as "always-on" coverage — no purchasing required before each journey. The trade-off is focus: annual plans prioritize emergency medical coverage and typically exclude or limit trip cancellation, CFAR, and baggage benefits that drive up single-trip premiums.

Despite that trade-off, the practical advantages are significant:

- Covers all trips under one policy, eliminating repetitive purchasing before each departure

- Spreads a flat annual premium across multiple trips, reducing the effective per-trip cost

- Delivers comprehensive emergency medical and evacuation coverage with aggregate annual limits

- Danish insurers like Tryg and Codan structure annual plans to cover entire households, including shared and step-children, under one policy

Use Cases of Annual Multi-Trip Insurance

Annual plans deliver the best value for:

- Frequent travelers taking 3+ trips annually, where the annual premium becomes cheaper than cumulative single-trip costs

- Business travelers making regular short work trips, typically under 30–45 days each

- Families taking multiple holidays, since household-based pricing spreads costs across everyone

- Spontaneous travelers who book last-minute, with no risk of forgetting to arrange coverage in time

Break-even illustration: Consider a traveler taking four trips per year, each lasting 7 days. Single-trip premiums accumulate with each booking; an annual plan charges one flat rate regardless of how many trips follow. By the third or fourth trip, the cumulative single-trip cost typically meets or exceeds the annual premium — and every trip after that is covered at no additional cost. The catch: the annual plan provides medical-focused coverage, not the cancellation protection built into most single-trip policies.

Cost Breakdown: When Does Annual Travel Insurance Actually Pay Off?

The "break-even point" is the number of annual trips where cumulative single-trip costs exceed the flat annual premium. Three independent sources confirm this threshold: InsureMyTrip, Squaremouth, and International Citizens Insurance all state that annual plans typically become cost-effective at 3 or more trips per year.

Verified Cost Benchmarks

Single-trip insurance:

- 4–8% of total trip cost (US Travel Insurance Association standard)

- Average 6–7% of trip cost (NerdWallet 2024 data)

- Provider range: 4–16% depending on age, destination, and coverage level

Annual multi-trip insurance:

- $413/year average (Squaremouth May 2025–2026 data)

- Typical range: $250–700/year

- Full market range: $73–2,892/year

Danish-specific pricing: No publicly available benchmark data exists for Danish travel insurance premiums. Danish consumers should use Forsikringsguiden.dk (operated by Forbrugerrådet Tænk and insurance industry associations) for personalized price comparisons across Danish insurers.

Key Pricing Variables

Single-trip costs fluctuate based on:

- Traveler age — older travelers pay higher premiums due to elevated medical risk

- Destination — regions with expensive healthcare (US, Japan) cost more to insure

- Trip duration — longer trips increase exposure and premium

- Total trip value — insurance costs scale with prepaid, non-refundable expenses

- Add-ons selected — CFAR, adventure sports, and winter sports coverage inflate premiums

Annual plans cost less per trip because they exclude expensive add-ons like cancellation, CFAR, and extensive baggage coverage. Their lower premiums reflect a narrower focus on medical and evacuation coverage, where actuarial risk is most predictable.

Understanding this cost structure matters — but it's only half the picture. How you manage your policy over time affects your price just as much as what you choose upfront.

The Loyalty Penalty Risk

Loyal customers who renew annually without comparison shopping face significant overpayment. Forbrugerrådet Tænk reports that Danish consumers with 10-year insurance tenure pay approximately 1,200 kr/year more than new customers at the same company, citing Konkurrencerådet data. The average Danish household overpays approximately 5,000 kr annually on non-life insurance due to loyalty surcharges and price creep.

If you auto-renew your annual travel insurance without benchmarking against market rates, you're likely paying inflated premiums — even when your coverage hasn't changed.

Per-Trip Duration Trap

If you purchase an annual plan with a 30-day per-trip cap but take one 60-day sabbatical, you face two costs:

- Lost coverage — your annual plan covers only the first 30 days; Codan coverage simply ceases after the cap

- Supplementary policy required — you must purchase a separate single-trip policy for the 60-day journey

In practice: an annual plan at 2,500 kr plus a supplementary single-trip policy for the 60-day journey at 1,500 kr comes to 4,000 kr total — worth comparing against purchasing single-trip policies for all trips as needed.

If your cumulative single-trip spending approaches annual plan pricing, switching is worth evaluating. Just verify what coverage you'd lose in the process — cancellation, CFAR, and baggage protection are often stripped from annual plans.

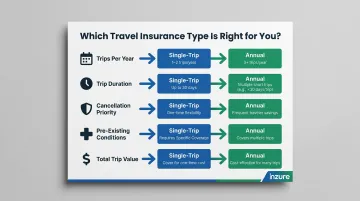

Which Type of Travel Insurance Is Right for You?

Choosing between single-trip and annual coverage hinges on five key factors:

- Number of trips per year — 1–2 trips favor single-trip; 3+ favor annual

- Duration of individual trips — any trip exceeding 45 days requires single-trip coverage

- Trip cancellation priority — significant non-refundable bookings demand single-trip comprehensive coverage

- Pre-existing medical conditions — single-trip plans offer broader coverage through waivers or SOS International pre-assessment

- Total value at risk — high-value trips justify higher single-trip premiums for full protection

Situational Recommendations

Choose single-trip if:

- You take 1–2 trips annually

- Any trip exceeds 45 days

- You have significant prepaid, non-refundable costs (cruises, package tours, luxury hotels)

- You have chronic health conditions requiring medical pre-assessment or waivers

- Trip cancellation and CFAR coverage are priorities

Choose annual if:

- You take 3+ trips yearly, each under 30–90 days

- Trips are primarily short business or leisure getaways

- Emergency medical coverage is your top priority

- You value convenience and don't want to repurchase coverage for each trip

- You travel with family (household-based pricing delivers substantial savings)

Family Travel Insurance Considerations

Both single-trip and annual policies are available as family or group plans in Denmark. Codan and Tryg structure annual plans to cover entire households, including shared children from previous relationships, under one policy at a combined rate. This is far cheaper than buying individual policies for each family member.

Key differences in family plan pricing:

- Flat household rate — Danish insurers charge one premium covering all household members, whether traveling together or separately

- Per-person vs. household excess — verify whether your excess (egenrisiko) applies per person or per claim; household-based excess reduces out-of-pocket costs per incident

For households taking multiple trips together throughout the year, a flat annual household premium spreads across all trips and all travelers — making annual plans the stronger value in most cases.

How to Evaluate Your Current Policy

Once you know which policy type fits your travel patterns, the next question is whether your current plan is priced fairly. Inzure is an independent Danish platform that reads and compares policy documents — uploaded as PDFs or photos — across Danish insurers including Tryg, Alka, Topdanmark, Codan, and GF.

The analysis identifies common issues like:

- Duplicate travel coverage already provided by credit cards or the Danish public health card (det gule sundhedskort) for EU travel

- Coverage gaps for adventure activities, winter sports, or pre-existing conditions

- Inadequate medical evacuation or cancellation limits

- Loyalty surcharges where renewal premiums exceed market rates

The platform benchmarks your policy against current Danish market data and flags specific gaps — like an annual plan with a 30-day cap that leaves you uninsured for longer trips. The analysis takes about 60 seconds and gives you clear recommendations with no obligation to switch.

Frequently Asked Questions

Why is multi-trip travel insurance often cheaper per trip than single-trip travel insurance?

Annual plans focus primarily on medical coverage and exclude or limit expensive benefits like trip cancellation and CFAR, keeping premiums lower. Spreading the flat annual cost across multiple trips reduces the effective per-trip price, making it cheaper for frequent travelers prioritizing medical protection.

How much does travel insurance cost for a 20,000 kr trip?

Single-trip travel insurance typically costs 4–10% of total trip cost, meaning a 20,000 kr trip would cost 800–2,000 kr to insure. Actual cost varies by traveler age, destination, trip duration, and coverage level selected.

Should I buy single-trip or annual (multi-trip) travel insurance?

The decision comes down to travel frequency: single-trip is better for 1–2 annual trips, especially high-value ones with significant cancellation risk. Annual plans are more cost-effective and convenient for travelers taking 3+ trips per year, each within the per-trip duration limit (typically 30–90 days).

Can travel insurance cover pre-existing medical conditions like gallstones, kidney stones, or diabetes?

In Denmark, insurers typically apply a 2-month look-back period — conditions requiring hospitalization or medication changes in that window are excluded unless pre-approved through SOS International assessment. Single-trip policies generally offer broader pre-existing condition coverage than annual plans, which usually limit coverage to acute onset only.

Should I get individual or family travel insurance, and how do they differ?

Family travel insurance covers multiple travelers under one policy at a combined household rate, which is often cheaper than buying separate individual policies. Danish insurers like Tryg and Codan structure annual family plans to cover entire households, including shared children — a strong option for families traveling together several times a year.