Going direct feels simple, but that simplicity hides a real cost. When you buy from a single insurer, you see only their products, their pricing, and their version of "good value." You have no benchmark for comparison, no external check on whether the price is fair, and no expert review of whether the coverage actually matches your needs. The information imbalance favours the insurer consistently.

This article explains why working with an independent broker or platform delivers measurable advantages in coverage quality, cost, and transparency — and why that difference matters more than most Danish consumers realise.

Key Takeaways

- Independent brokers work for you, not the insurer — giving you access to multiple carriers and unbiased advice

- Going direct locks you into one insurer's products and no way to know if you're overpaying

- Brokers identify coverage gaps, duplicate policies, and overpayments that direct buyers typically miss

- Loyal customers who buy direct often pay more at renewal because insurers rely on inertia to keep raising premiums quietly

- Annual policy reviews catch price hikes and coverage drift before they cost you — something a direct insurer has no incentive to flag

What Is an Independent Insurance Broker?

An independent insurance broker is a licensed professional or platform that represents the policyholder — not the insurer — to find, compare, and optimise coverage across the market.

Where brokers operate:

- Personal insurance (home, travel, accident, contents, liability)

- Family coverage plans

- Whenever a consumer has a choice between multiple carriers

The broker's job is to deliver a specific outcome: better-matched coverage at a fair market price. In Denmark, truly independent brokers must represent only the customer, forward any insurer commissions in full to the client, and base advice on analysis of a sufficiently large number of contracts.

In practice, this means independent brokers work on a client fee basis — not hidden commissions tied to which insurer they recommend. The value shows up in tangible outcomes: identifying overpricing, closing coverage gaps, and surfacing market intelligence that direct buyers cannot access on their own.

Key Advantages of Choosing a Broker Over Buying Direct

The advantages below are grounded in practical, day-to-day outcomes — cost, coverage quality, risk exposure, and long-term value — rather than theoretical benefits.

Advantage 1: Access to the Whole Market, Not Just One Insurer's Products

When you buy direct from Tryg, Topdanmark, or Alka, you can only see that company's products. There is no built-in mechanism to compare pricing, coverage terms, or exclusions across competitors. You are negotiating with incomplete information.

How a broker creates this advantage:

A broker works across multiple carriers, surfacing options you would never encounter on your own — including specialised products better suited to your profile. For example, Forsikringsguiden.dk, a joint initiative by Insurance & Pension Denmark and Forbrugerrådet Tænk, compares offerings from approximately 86% of Danish insurers, enabling like-for-like quotes across the market.

Why this is an advantage:

Insurance premiums for the same level of coverage can vary significantly between carriers for the same applicant. Forbrugerrådet Tænk warns of "store prisforskelle" (large price differences) on home contents insurance and notes that consumers risk paying significantly more for coverage that is essentially the same as cheaper options.

Without market access, consumers systematically overpay — not through deception, but through ignorance of what's available.

When this advantage matters most:

This is especially important:

- At renewal time, when insurers often raise prices for existing customers (the "loyalty tax")

- When life circumstances change — new home, growing family, new bicycle — that alter the optimal coverage profile

- After several years with the same insurer, when loyalty penalties accumulate silently

A 2025 market study by the Danish Competition and Consumer Authority (KFST) found that customers with 10+ years of tenure pay margins 7–8 percentage points higher than new customers with the same risk. In some companies the difference is 30–35 percentage points for house and contents insurance. KFST quantified an average extra cost of about DKK 1,108 per year for a long-tenure customer across car, house, and contents combined.

Advantage 2: Expert Coverage Analysis — Identifying Gaps, Duplicates, and Mis-Matched Policies

Buying direct puts the entire burden of policy evaluation on you: understanding exclusions, assessing coverage limits, and spotting where two policies might overlap or where a critical gap exists. Most consumers are not insurance experts, and policy documents are rarely written with the reader in mind.

What a broker actually checks:

A broker reviews your full insurance picture, cross-referencing policies for:

- Redundant coverage that wastes money (e.g., travel insurance already included in your credit card or the Danish yellow health card for EU travel)

- Unprotected risks that create financial exposure at claim time (e.g., missing legal aid insurance, bicycle theft coverage, or family-member exclusions)

- Mis-matched coverage limits that leave you underinsured (e.g., inadequate sum-insured for valuables or insufficient liability limits)

The cost of getting it wrong:

A coverage gap means an unexpected bill when a claim is denied. A duplicate means paying twice for protection already in place. Either way, the financial damage only surfaces when it's too late to fix it.

The Danish Insurance Complaints Board (Ankenævnet for Forsikring) received 2,193 new complaints in 2025, with consumers obtaining a favourable outcome in only about 18% of materially decided cases. Many disputes hinge on exclusions, sub-limits, or conditions that consumers misunderstood at the time of purchase.

A broker's review shifts insurance from a passive annual purchase to an active risk management tool — one that directly affects both what you pay and what you receive when something goes wrong.

When this advantage matters most:

This is most critical for:

- Households with multiple policies (home, contents, travel, accident, liability), where overlaps and gaps accumulate silently over years

- Major life events — marriage, divorce, children, property purchase — that change your risk profile significantly

- Long-term policyholders who have never reviewed coverage terms since the initial purchase

Advantage 3: Independence and Alignment — Your Broker's Interests Are Aligned With Yours

A direct insurer's agent is paid to sell that insurer's products. An independent broker is structurally incentivised to find the best solution for you, because their value proposition depends on it.

How this plays out in real situations:

- At claim time, a broker advocates on your behalf

- At renewal, they challenge unfair price increases

- Throughout the relationship, they are a point of contact whose success depends on your satisfaction, not the insurer's sales volume

Under the EU Insurance Distribution Directive (IDD), where an intermediary claims to give advice on a "fair and personal analysis," it must base that advice on an analysis of a sufficiently large number of contracts on the market, and recommendations must match the customer's demands and needs.

Why this is an advantage:

This alignment changes the dynamic at the most important moment — a claim — when you most need someone in your corner. Knowing there is an expert who monitors your coverage, flags renewals, and challenges unfair pricing has ongoing value that a one-time price comparison cannot replicate.

Platforms like Inzure embody this principle digitally: the AI-driven analysis works on your behalf, benchmarking your policies against real-time market data from Danish insurers, identifying loyalty surcharges, and flagging gaps or overlaps. The service is free unless you save money by switching, aligning the platform's success with your financial benefit.

When this advantage matters most:

This matters most:

- During claims (stress, complexity, time pressure)

- During automatic renewals (where price increases go unnoticed)

- For consumers who have been with the same insurer for many years and have not benchmarked their premiums against the market

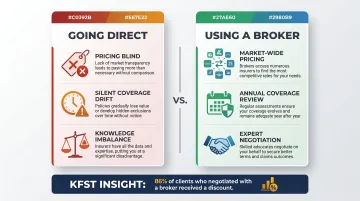

What Happens When You Skip the Broker and Go Direct

Going direct without independent guidance creates three compounding risks:

You're pricing blind. KFST found that 72% of Danish consumers had not switched, considered switching, or even obtained a quote from another company in the last two years. Of those who did switch, 61% collected only one alternative quote — meaning they still had no real benchmark.

Coverage mismatches compound silently. Without annual review, gaps widen, duplicate premiums accumulate, and loyalty pricing penalties grow unnoticed with each renewal.

The knowledge gap favours the insurer. Insurers know their products, pricing structures, and discount thresholds in detail. A consumer buying direct doesn't — and that imbalance is built into every quote they receive.

That knowledge gap has a direct cost. KFST reports that 86% of consumers who negotiated at purchase got a discount, and 79% who negotiated after becoming customers also succeeded — yet most never try, because they don't know what a fair price looks like in the first place.

How to Get the Most Value from an Independent Broker

The broker advantage works best when the relationship is ongoing, not transactional. An annual review of all active policies captures changes in both your circumstances and the market that a one-time purchase cannot.

To get the most from each review, come prepared with:

- A clear picture of existing policies

- Recent renewal notices

- Any life changes (new home, family additions, new valuables)

This lets your broker focus on gaps and opportunities rather than gathering basics.

That same preparation works equally well on digital platforms. By uploading existing policy documents (PDFs or photos), Inzure analyses coverage gaps, duplicates, and market pricing in 60 seconds. The analysis is free — you only pay 20% of the savings achieved if you switch to a better deal, which has ranged from kr. 2,800 to kr. 48,000 a year for users who found a mismatch.

Either way, surfacing overpayments and gaps is only half the job. The financial benefit only materialises when you act — switching, renegotiating, or adjusting coverage based on what you find.

Conclusion

The broker advantage is not about adding complexity — it is about putting market knowledge back in the consumer's hands. With full visibility across carriers, independent expertise, and interests that align with yours rather than the insurer's, coverage decisions simply land better than those made in isolation.

This advantage compounds over time. Each year of guided review is a year where overpayments get challenged and gaps get closed. Meanwhile, the direct buyer's position quietly erodes with every unchecked renewal.

For Danish consumers, tools like Forsikringsguiden and platforms like Inzure have made independent market analysis genuinely practical — no lengthy calls, no industry jargon, no obligation to switch. Getting clarity on what your insurance should actually cost has never been more straightforward.

Frequently Asked Questions

Is it cheaper to get insurance direct or through a broker?

In most cases the price is the same or lower through a broker. In Denmark, truly independent brokers forward any insurer commissions in full to you, working on a transparent fee basis. Brokers often find cheaper equivalent coverage by comparing across multiple insurers.

Do brokers charge consumers a separate fee for their services?

Independent brokers in Denmark work on a client fee basis, and any compensation from insurers must be forwarded to you in full. Some platforms like Inzure charge only if they save you money — 20% of the first year's savings — making the service risk-free.

What is the "loyalty tax" in insurance, and why does it matter?

The loyalty tax refers to the practice of insurers charging long-standing customers more at renewal than new customers for the same coverage. KFST documented that Danish customers with 10+ years of tenure pay margins 7–8 percentage points higher than new customers, costing about kr. 1.108 extra per year. An independent broker can identify and challenge this pricing practice.

Can a broker help me if I already have existing insurance policies?

Yes. Reviewing existing policies is one of the most valuable things a broker does — identifying overpayments, duplicate coverage, and gaps often delivers immediate savings without a full switch. Platforms like Inzure analyse your existing policies in 60 seconds and benchmark them against the Danish market.

How do I know if I am paying too much for my insurance?

Without an independent market comparison, there is no reliable way to know. That is precisely the problem with buying direct. An independent broker or AI-driven platform can benchmark your current premiums against the full market in minutes, revealing loyalty surcharges and better alternatives.

What should I look for when choosing an independent insurance broker?

Look for verified independence from all insurers, transparency about how they are compensated, access to a broad range of carriers, and a track record of proactive annual reviews rather than one-time sales. In Denmark, verify they comply with Finanstilsynet's requirements for independent intermediaries.