Introduction

For Danish motorcycle owners, the renewal notice in your inbox is your annual window to switch providers on your own terms. Switching at renewal means no cancellation penalties, no partial refund calculations, and no risk of a coverage gap — as long as you time it correctly.

Most Danish motorcyclists let their policies auto-renew without questioning whether they're overpaying. Research from Forbrugerrådet Tænk confirms that loyal customers who stay with the same insurer for 10 years pay roughly 1,200 DKK more per year than new customers for identical coverage. Insurers price this in deliberately, counting on policyholders not to shop around.

This guide walks you through why renewal is the ideal switching window, what documents and information to prepare, and the exact six-step process to switch motorcycle insurance providers without losing your no-claim bonus or riding uninsured for even a single day.

Key Takeaways

- Renewal is the cleanest time to switch — no cancellation fees, no coverage gaps

- Secure your new policy before canceling the old one to avoid uninsured riding

- Check your current policy's opsigelsesvarsel (cancellation notice period) — most Danish insurers require 30 days' written notice

- Compare beyond price: coverage scope, theft-abroad protection, and selvrisiko (excess) all affect real value

- Start comparing 3-4 weeks before renewal to meet opt-out deadlines in time

Why Renewal Is the Best Time to Switch Motorcycle Insurance

What "Switching at Renewal" Actually Means

When your policy expires naturally at its annual renewal date, you simply choose not to renew with your current insurer and activate a new policy with a different provider instead. There's no early termination penalty, no short-rate cancellation fee, and no complicated partial refund calculation—your contract ends cleanly, and the new one begins the next day.

This makes renewal fundamentally different from switching mid-term, which typically involves an administration fee and potential gaps in your coverage timeline.

The Loyalty Trap: Why Long-Term Customers Pay More

Danish insurers systematically charge loyal customers higher premiums than new customers for identical coverage. The data is stark:

- 10-year customers pay approximately 1,200 DKK more per year than new customers for the same policy, according to a 2025 analysis by the Danish Competition and Consumer Authority

- The average Danish household overpays more than 5,000 DKK annually on non-life insurance, per Forbrugerrådet Tænk — driven by index-linked price increases that raise premiums year after year without alerting policyholders

- Only 17% of Danish customers who experience a price increase actually switch, according to Finanswatch (March 2025) — most never notice the increase at all

Renewal Triggers Mandatory Disclosure

Under Danish law (Forsikringsaftaleloven section 31), insurers must notify policyholders between one and three months before the cancellation deadline if a policy is set to auto-renew for more than one year. This notification window gives you a formal, informed basis for comparison—making renewal the one moment each year where you're contractually entitled to full transparency about what happens next.

What to Review Before You Start Shopping

Cross-Check Your Renewal Notice Against Last Year

Pull out your current renewal notice and compare three specific items:

- Premium change: What's the new annual premium versus last year's? Calculate the percentage increase, not just the DKK amount

- Coverage term changes: Have deductibles increased? Has your coverage tier changed without your consent?

- Add-on pricing: Have roadside assistance, equipment coverage, or zero-depreciation options been silently removed or repriced as optional extras?

Many Danish insurers apply automatic index adjustments without highlighting the change, meaning a seemingly routine renewal notice can hide a 5-10% price increase.

Benchmark Your Current Policy Against Market Rates

Before comparing external quotes, understand your current policy's actual market value. Tools like Inzure can analyze your existing bike insurance policy in 60 seconds by uploading a PDF or photo of your policy documents. This establishes a clear baseline—showing what you're paying versus what the market actually charges for equivalent coverage—so you know exactly where you stand before requesting a single quote.

Cyclists who've held the same policy for several years are the most likely to benefit — loyalty surcharges accumulate quietly, and most riders never think to question them.

Update Personal Inputs That Affect Pricing

Note any changes since last year that should affect your premium:

- New motorcycle (make, model, engine size, market value)

- Change in annual mileage or riding patterns

- New parking location (covered garage vs. street parking)

- Accumulated claim-free years (your no-claim bonus may have increased)

Updating these inputs before shopping ensures quotes reflect your real situation, not an outdated profile that could result in inaccurate pricing or rejected claims later.

How to Switch Motorcycle Insurance at Renewal: Step-by-Step

The process takes 4-6 steps over a 3-4 week window before renewal. Done in the right order, it guarantees no coverage gap and no lost benefits.

Step 1: Confirm Your Renewal Date and Opt-Out Deadline

Most Danish insurers require written notice if you don't want your policy to auto-renew—typically one month's notice to the first of a month. Missing this deadline can trigger automatic renewal and lock you in for another year.

What to do: Check your policy documents or call your insurer to confirm:

- The exact renewal/expiry date (hovedforfaldsdato)

- The deadline for written cancellation notice

- Whether your policy is set to auto-renew

Under current Danish law, you can cancel non-life insurance with one month's notice to the first of a month year-round—you're not required to wait for the annual renewal date. However, canceling at the anniversary avoids any administration fees.

Step 2: Gather Quotes from at Least Three Providers

Request formal written quotes from at least three Danish insurers using identical inputs across all providers:

Critical comparison factors:

- Coverage type: Third-party liability (ansvarsforsikring) vs. comprehensive (kasko)

- Deductible amount (selvrisiko)

- Add-ons: Roadside assistance, equipment coverage, zero-depreciation

- Riding season: Year-round vs. seasonal (March-November)

Major Danish motorcycle insurers to consider include Tryg, If Forsikring, Topdanmark, Alka, and FIRST (MCforsikring.dk). Use comparison tools like Forsikringsguiden.dk, which compares approximately 86% of all Danish insurance companies.

Warning: Online quotes are indicative only. Request formal written quotes before making a decision, and watch for introductory pricing that increases sharply at first renewal.

Step 3: Compare Policies Side by Side—Not Just Price

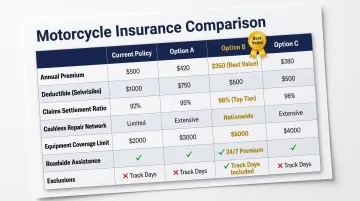

Price is important, but it's not the full picture. Create a simple comparison table with these dimensions:

| Factor | Current Policy | Option A | Option B | Option C |

|---|---|---|---|---|

| Annual premium | ||||

| Deductible (selvrisiko) | ||||

| Claims settlement ratio | ||||

| Cashless repair network | ||||

| Equipment coverage limit | ||||

| Roadside assistance | ||||

| Exclusions |

Key dimensions beyond price:

- Claims settlement ratio: How reliably and quickly does the insurer pay out? In 2025, motor vehicle complaints to Ankenævnet for Forsikring rose to 249 cases—consumers won favorable outcomes in only 9.6% of them

- Approved repair centers: Does the insurer have a network of cashless garages in your area?

- Exclusions: What damage types or scenarios are excluded? Some policies exclude theft from unlocked garages or damage from non-approved modifications

- Customer service: What are complaint volumes and resolution rates for each insurer?

A 15% lower premium means little if a claim takes six weeks to resolve. Factor settlement speed and exclusion scope into your final decision before moving to Step 4.

Step 4: Confirm Your No-Claim Bonus Transfer

If you have not made any claims in the current policy year, you are entitled to a no-claim bonus (NCB) that reduces your next premium. At renewal, this NCB can be transferred to a new insurer—but only if you follow the correct process.

Steps to protect your NCB:

- Request an NCB certificate (bonuscertifikat) from your current insurer before switching

- Present this certificate when activating your new policy

- Confirm with the new insurer that the NCB has been applied to your premium

Warning: Skipping this step means starting at zero with the new provider—forfeiting years of accumulated discounts. The NCB belongs to you, not your insurer.

Industry practice — not statutory law — governs NCB portability in Denmark. Insurers exchange claims history via an EDI platform under Forsikring & Pension guidelines, but the transfer requires your explicit consent.

Step 5: Activate the New Policy Before Canceling the Old One

CRITICAL RULE: The new policy's start date must be set to the exact day the old policy expires. Never cancel first and buy second.

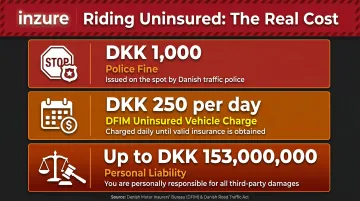

Even a 24-hour gap leaves your motorcycle legally uninsured. Under Danish law, all registered motorcycles must carry third-party liability insurance (ansvarsforsikring). Riding uninsured results in:

- DKK 1,000 police fine if stopped without valid insurance

- DKK 250 per day charge from DFIM for each uninsured day

- Personal liability for all damages if you cause an accident (up to DKK 153 million for personal injury or DKK 30 million for property damage)

The good news: most Danish insurers allow future-dated policy activation, so lining up dates correctly takes minutes. Some insurers, such as If Forsikring, will handle the cancellation of your old policy and coordinate effective dates to avoid gaps entirely.

Step 6: Formally Notify Your Current Insurer and Confirm Cancellation

Once the new policy is confirmed and active, send written cancellation to your old insurer:

Best practice:

- Send via email with read receipt or certified letter (anbefalet post)

- Reference your policy number and exact end date

- If auto-renewal was enabled, confirm in writing that it will not proceed

- Request written confirmation of cancellation and final premium statement

Retain proof of cancellation in case of billing disputes. Under Forsikringsaftaleloven section 16, if you cancel early, your insurer is entitled only to premium for the period during which coverage was active—any overpaid premium must be refunded.

What Can Affect Your New Premium With a Different Provider

Primary Rating Factors

A new insurer will price your policy based on:

Motorcycle characteristics:

- Make, model, and engine size

- Current market value (dagsværdi)

- Model year (årgang)

Rider profile:

- Age and years of riding experience

- Claims history and accumulated NCB

- Completion of safety training (e.g., 5% discount at Tryg for FDM køreteknik kursus)

Usage and location:

- Primary location (urban vs. rural)

- Parking type (covered garage vs. street)

- Annual mileage estimate

- Seasonal vs. year-round coverage

The same rider can receive notably different quotes from different insurers because each company weights these factors differently. For example, one insurer may penalize urban parking more heavily, while another may offer steeper discounts for safety course completion.

Your NCB Transfers, But Loyalty Discounts Don't

When you switch insurers, loyalty discounts from your old provider don't carry over. However, your no-claim bonus does transfer, so requesting your NCB certificate before you leave is essential.

Some insurers offer new-customer discounts that expire at renewal, meaning your first year's premium may not reflect what you'll pay long-term. Always ask for multi-year pricing estimates before committing.

Multi-Policy Bundling Risks

If you insure your motorcycle and other assets (car, home contents, travel) with the same provider, switching only the motorcycle may cause you to lose a multi-policy discount (samlerabat) on your other insurance.

Bundle discount levels in Denmark:

- Tryg: Up to 20% (requires indboforsikring as base, scales with up to 6 policy types)

- If Forsikring: Up to 15% (via If Fordelsprogram)

- Alka: 10% (via PlusKort or union membership such as 3F, HK)

Calculate the net effect across all your policies before switching just one. You may lose more in aggregate discount than you save on a cheaper standalone motorcycle policy.

Common Mistakes to Avoid When Switching at Renewal

Mistake: Auto-Renewing Without Reviewing

The most expensive mistake is doing nothing—accepting the renewal quote without comparing. Insurers rely on customer inertia, and prices for returning customers frequently exceed what a new customer would pay for the same policy.

This "loyalty tax" is well-documented: Forbrugerrådet Tænk found that loyal customers pay 1,200 DKK more annually after 10 years with the same insurer. Yet only 17% of customers who receive price increases actually switch.

Fix: Price-test your insurance every 1-2 years using tools like Forsikringsguiden.dk or Inzure.

Mistake: Comparing Only on Price

Choosing the cheapest policy without checking the claims settlement process, exclusions, and repair shop network can cost you more when it matters. A policy that's 15% cheaper but excludes the most common damage types—or takes weeks to settle claims—is no bargain.

Fix: Use the comparison table in Step 3 to evaluate claims settlement ratio, repair network, and exclusions alongside price.

Mistake: Forgetting to Claim or Transfer the NCB

Many riders assume their no-claim bonus (NCB) disappears when they switch. It doesn't—but you need to act. Riders who skip requesting the certificate, or forget to present it to the new insurer, leave significant discounts unclaimed.

The NCB belongs to you, not the insurer. Always request your NCB certificate before canceling, then submit it to your new provider when activating coverage.

Mistake: Letting Coverage Lapse Even Briefly

Any gap—even one day—means riding without legal insurance coverage. This carries:

- DKK 1,000 police fine

- DKK 250/day DFIM charge

- Personal liability for all damages if you cause an accident

- Future insurers may flag the lapse in your coverage history, potentially raising premiums

Fix: Always activate the new policy before canceling the old one, with the new start date set to the exact day the old policy expires.

Frequently Asked Questions

What happens if you switch insurance before renewal?

Switching mid-term is possible but typically involves a cancellation fee and a pro-rata refund for unused premium. Secure a new policy before canceling and calculate whether the savings outweigh the cancellation cost before proceeding.

Is there a grace period for motorcycle insurance renewal?

Most insurers offer a short administrative window (15-30 days) after expiry for renewal, but during this gap your motorcycle is technically uninsured. Riding during a lapse—even within that window—can void claims and result in fines. The grace period covers administrative renewal only, not active coverage.

Can I transfer my no-claim bonus when switching motorcycle insurance at renewal?

Yes, the NCB is portable and transfers to the new insurer at renewal. Request an NCB certificate from your outgoing insurer and submit it when activating the new policy to secure the discount.

Will switching motorcycle insurance providers affect my future premiums?

Switching itself does not negatively affect premiums—in fact, it often results in lower premiums by accessing new-customer pricing. However, resetting with a new provider means losing tenure-based loyalty discounts from the previous insurer, making NCB transfer the most important step in the process.

How far in advance should I start comparing before my renewal date?

Start 3-4 weeks before your renewal date to allow time to gather formal quotes, compare coverage details, and meet the opt-out or cancellation notice deadline required by your current insurer without feeling rushed.