This decision matters beyond convenience. It affects your total premium spend, coverage continuity, and how much control you retain over your policy. Insurance companies don't make this comparison easy because complexity protects their margins. According to TV2's April 2025 investigation, loyal Danish customers pay an average of 240 kr more per year for home contents insurance (which includes bicycle cover) than new customers at the same risk profile. That's the loyalty penalty in action — and it compounds quietly over time.

Key Takeaways

- Annual bike insurance offers lower upfront cost and the freedom to switch or adjust coverage yearly

- Multi-year policies lock in premiums and reduce lapse risk, though Danish insurers don't currently offer them

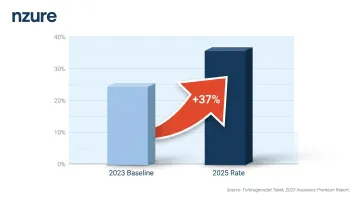

- Danish insurance prices rose up to 37% between 2023-2025, making price protection increasingly valuable

- 75% of Danish insurance customers accept renewals without negotiating or comparing alternatives

- Neither option is universally superior — the right choice depends on your ownership plans and renewal discipline

Annual vs Multi-Year Bike Insurance: Quick Comparison

Policy Duration

Annual insurance covers your bike for exactly one year and must be renewed each policy period. You track expiry dates carefully to avoid lapses, and each renewal is a separate decision each time.

Multi-year insurance would cover you for two to five consecutive years under a single purchase, eliminating the annual renewal cycle entirely. However, no Danish insurer currently offers multi-year bicycle insurance — the entire market operates on annual auto-renewal contracts under the Danish Insurance Contracts Act.

Premium Cost

Annual premiums are recalculated at each renewal and can increase due to market rate changes, inflation, or regulatory adjustments. Forbrugerradet Tænk's 2025 insurance package test documented price increases of up to 37% across bundled personal lines insurance between 2023 and 2025. While this figure covers broader insurance packages (house, contents, car, accident), bicycle coverage is embedded within indboforsikring, so premium movements in that product line directly affect bicycle cover costs.

Multi-year plans, where available in other markets, lock in the rate at purchase and protect against price increases mid-policy. In Denmark's current market structure, this protection doesn't exist for bicycle insurance.

Flexibility

Annual policies allow you to:

- Switch insurers at each renewal

- Adjust coverage levels based on bike value changes

- Add or remove riders as your needs evolve

- Take advantage of competitive market offers

Multi-year policies would be more rigid — add-ons chosen at the start generally stay fixed for the term. Switching insurers mid-term typically requires policy cancellation, partial refunds, and administrative complexity.

No Claim Bonus (NCB)

NCB is a discount earned for claim-free periods. In motor insurance markets, this operates as a formalized percentage discount ladder. However, Danish bicycle insurance does not use a documented NCB system. Instead, insurers adjust pricing based on claims history across all products held by a customer, creating a "total risk profile" rather than a transparent bonus structure.

With annual policies, your claims history affects renewal pricing — but there's no published NCB percentage to track or protect. Multi-year policies would shield you from market-wide pricing adjustments each year, though your own claims history would still affect pricing at renewal.

Lapse Risk

Annual policies create recurring opportunities to forget renewal deadlines. Danish law defaults to auto-renewal, which significantly lowers accidental lapse risk — but only if payment continues successfully. If payment fails or you actively cancel without arranging replacement cover, you're legally uninsured.

Multi-year policies would eliminate this risk for their entire duration. Since none currently exist in Denmark, the auto-renewal mechanism serves as the default protection against coverage gaps.

What Is Annual (Single-Year) Bike Insurance?

Annual bike insurance provides coverage for one year from the start date, after which it automatically renews unless you actively cancel. It covers the same areas — own damage, third-party liability (where required), and theft protection — as any multi-year plan would. The difference lies purely in duration and pricing structure.

Annual plans offer real flexibility:

- Lower initial payment makes coverage accessible

- Full freedom to shop the market at every renewal

- Ability to modify coverage, deductibles, or add-ons each year

- Easy adjustments as your bike's value depreciates

That flexibility comes with a catch. Annual renewal creates a recurring decision point — and Danish auto-renewal law protects against accidental lapse, but not against passive overpayment. Research cited by TV2 shows 75% of Danish insurance customers don't negotiate prices with their insurer — accepting renewal notices even as premiums climb year after year.

Use Cases of Annual Insurance

Annual insurance tends to work well when your situation is likely to change:

- Riders planning to sell or upgrade within 1-2 years

- Seasonal riders whose usage patterns shift year to year

- Disciplined shoppers who actively compare rates at renewal

- Those whose bike value is depreciating and needs coverage adjustments

It's a weaker fit if any of these apply:

- You're unlikely to track market pricing every renewal cycle

- Your bike is essential for daily transport and coverage gaps aren't an option

- You've historically accepted renewal notices without comparing alternatives

What Is Multi-Year Bike Insurance?

Multi-year bike insurance covers your bike for two to five consecutive years under a single agreement, removing the annual renewal cycle and locking in pricing at today's rates for the full term.

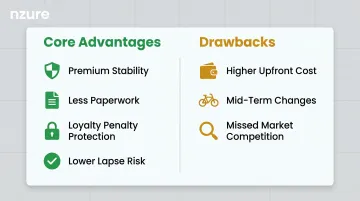

Core advantages:

- Premium stability — no year-on-year rate increases within the policy term

- Less paperwork and fewer renewal reminders to track

- Automatic protection against the loyalty penalty

- Lower lapse risk over the coverage period

Drawbacks:

- Higher upfront cost creates a barrier

- If your riding situation changes mid-term (selling the bike, relocating, switching to an EV), cancellation involves refund complexity

- You lose the annual opportunity to benefit from market competition or new entrants

In practice, no Danish insurer currently offers this product. The Danish Insurance Contracts Act (Forsikringsaftaleloven) Section 31 establishes auto-renewal as the default, and market practice centers firmly on one-year terms. Extensions beyond one year require specific insurer notification 1-3 months before the cancellation deadline, a procedure that is not standard in the bicycle insurance market.

Use Cases of Multi-Year Insurance

Best fit:

- Owners planning to keep their current bike long-term

- Those who have historically struggled with renewal awareness

- Riders in markets where insurance premiums are rising consistently

Multi-year policies work less well for riders who expect their situation to change soon:

- Short-term ownership plans

- Riders who want to actively shop the market annually

- Those anticipating significant changes in riding patterns or bike value

Annual vs Multi-Year: Which One Is Right for You?

The "right" answer depends on four variables: how long you'll keep the bike, how disciplined you are about renewals, whether premium rates are trending upward, and how much flexibility you want over coverage choices.

Financial Comparison

Let's walk through a realistic scenario. Assume a rider pays 2,000 kr/year for bicycle theft coverage in year one. Based on Tænk's documented trend of up to 37% increases over two years across insurance packages, a conservative annual increase of 10% gives us:

- Year 1: 2,000 kr

- Year 2: 2,200 kr (10% increase)

- Year 3: 2,420 kr (10% increase)

- Total over 3 years: 6,620 kr

If a multi-year lock-in at 2,000 kr/year were available:

- Total over 3 years: 6,000 kr

- Savings: 620 kr over three years

No bicycle-specific premium trend data is published in Denmark, so treat these numbers as directional. The principle holds: lock in today's rate and you avoid compounding increases.

Situational Recommendation

Choose annual if:

- Flexibility and lower upfront cost are priorities

- You may sell the bike within 1-2 years

- You're disciplined about comparing options at renewal

- You want to reassess insurer quality yearly

Choose multi-year if (and when available):

- You value stability and predictability

- You're confident in your insurer's service quality

- You plan to keep the bike long-term

- You want to eliminate renewal complexity

The Overlooked Risk

Many riders on annual plans don't actually compare options at renewal. They accept the renewal notice without checking if better value exists elsewhere. This is where loyal customers consistently overpay year after year.

The UK's Financial Conduct Authority found that in 2018, 6 million loyal UK home and motor insurance policyholders would have saved a collective £1.2 billion had they paid the average price for their actual risk. The FCA's remedies were projected to save UK consumers £4.2 billion over 10 years. Denmark has not implemented a similar price walking ban.

In Denmark, the loyalty penalty is well-documented. TV2's investigation revealed that customers with 10+ years of tenure pay an average of 240 kr more per year for indboforsikring than new customers. One customer loyal to Tryg for 20 years saved 8,000 kr annually by switching insurers after a single policy increased by 487 kr (12%) in one year.

How to Make an Informed Choice

Before deciding, run an independent comparison of your current policy against market options — not just on price, but on what's actually covered.

Inzure's AI-powered analysis reads your existing bike insurance policy and identifies whether you're paying a fair market rate in 60 seconds. Upload your policy as a PDF or screenshot, and the platform benchmarks your coverage against equivalent options from Danish insurers like Tryg, Alka, Topdanmark, and standalone providers like Qover.

You'll discover:

- Whether your bicycle is adequately insured

- If you're missing theft protection for high-value bikes (e.g., e-bikes, cargo bikes)

- Whether you're overpaying compared to market rates

- If there are coverage exclusions that put you at risk

The analysis is free. You only pay a 20% commission if Inzure finds a better deal and you choose to switch.

Real-World Scenario

Consider a bike owner who auto-renews for three years without reviewing their policy. By year three, their premium has climbed from 2,000 kr to 2,420 kr — a cost a multi-year lock-in would have avoided entirely.

The same owner, however, noticed their insurer's claim service deteriorate after year two: delayed responses, unclear documentation requirements, and a rejected theft claim on a technicality. An annual plan gave them the freedom to switch at renewal. A multi-year commitment would have trapped them in poor service for the full term.

The 620 kr in savings isn't worth much if you're stuck with an insurer you can't trust. Both plan types carry trade-offs — the right choice depends on how confident you are in your insurer today.

Conclusion

Annual and multi-year bike insurance serve different needs. If you value long-term savings, consistency, and less admin overhead, a multi-year structure has clear advantages — where available. If your circumstances are likely to shift (bike ownership, coverage needs, budget), an annual plan keeps your options open.

Either way, don't let the decision default to whichever option your insurer makes easiest. In Denmark's market, staying in control means:

- Understanding how auto-renewal works on your current policy

- Tracking your premium from year to year

- Comparing alternatives before accepting any renewal notice

That last point is where most people fall short. Use Inzure's free AI analysis to benchmark your current bike insurance against the Danish market in 60 seconds — and see exactly what a fair price looks like for your coverage.

Frequently Asked Questions

Are multi-bike policies cheaper?

Multi-bike or multi-vehicle policies can offer savings through bundled discounts, but pricing depends on the insurer and individual risk factors. However, Forbrugerradet Tænk warns that bundle discounts often don't pay off and can make it harder to switch individual policies. Always compare bundled versus separate policies independently.

Is monthly or yearly insurance better?

Monthly payments typically cost more in total than annual payments because insurers charge a premium for the installment option. Annual payment is generally cheaper overall, while multi-year (where available) offers the best long-term rate lock-in — but each suits different budget situations.

When should I renew my bike insurance?

Begin the renewal process at least 30 days before your policy expiry date. Renewing early ensures continuous coverage, avoids lapse penalties, and gives you time to compare alternatives instead of accepting the renewal automatically. Danish law requires 30 days' notice to cancel.

Which plan is better for bike insurance?

Multi-year plans aren't available in Denmark, so annual policies are the standard. Within that, your choice comes down to priorities: annual payment costs less upfront, while monthly installments offer flexibility at a higher total cost. Pick the structure that matches your budget and how long you plan to keep the bike.

Can I switch bike insurance mid-policy in Denmark?

Yes. Danish insurance law gives you the right to cancel with 30 days' written notice. If you've found a better deal, you can switch at renewal or mid-term — just ensure the new policy starts before the old one lapses to avoid a coverage gap.