Introduction

Many Danish motorcyclists face an expensive, confusing problem: managing separate insurance policies for each bike they own. Each policy comes with its own renewal date, separate premiums, and individual claims processes. Worse, most riders don't realise that consolidating their coverage under a portfolio discount (samlerabat) structure could reduce their total insurance spend significantly.

Danish insurers don't offer true "multi-bike policies" the way some international markets do. Instead, you insure each motorcycle individually, then bundle those policies with your other insurance products to unlock discounts. According to Forbrugerrådet Tænk's 2025 report, loyal customers who consolidate and forget often pay up to 5,000 DKK more annually than new customers with identical coverage.

This guide covers:

- How Danish motorcycle insurance bundling actually works

- What coverage components matter for each bike

- How to compare discount structures across providers

- How to avoid the loyalty penalty that inflates your premiums without any notification

Key Takeaways

- Each motorcycle requires its own policy in Denmark; discounts come from bundling multiple policies under one insurer (samlerabat)

- Bundling typically saves 10-20% depending on the provider and total number of policies you consolidate

- Liability coverage (ansvarsforsikring) is mandatory for every bike, while physical damage coverage (kasko) can be tailored per motorcycle

- Compare discount percentages, custom parts limits, and loyalty penalty risks before choosing an insurer

- Use an independent platform to check whether your bundled premium is competitive or subject to quiet price creep

What Is Multi-Bike Insurance and How Does It Work?

"Multi-bike insurance" in Denmark is a misnomer. Unlike the UK or US markets where a single policy covers multiple motorcycles at a tiered discount rate, Danish insurers require each motorcycle to have its own separate policy. What riders actually do is bundle multiple motorcycle policies together with other insurance products—such as home, travel, or accident insurance—to unlock a general portfolio discount (samlerabat).

Each motorcycle is insured individually, with its own premium based on factors like bike value, rider age, and claims history. Once you bundle at least two or three policies under the same insurer, the samlerabat discount applies across your entire portfolio. Discount levels vary by carrier:

| Forsikringsselskab | Samlerabat | Kilde |

|---|---|---|

| Gjensidige | 10% (fra 3 policer) | gjensidige.dk |

| Tryg | Op til 20% | tryg.dk |

| Topdanmark | Op til 12% | topdanmark.dk |

Coverage is set separately for each bike. Liability (ansvarsforsikring) is legally mandatory for every registered motorcycle and covers up to 50 million DKK for personal injury and 10 million DKK for property damage to third parties — but it excludes the driver's own injuries. Physical damage cover (kasko) is optional and chosen per bike. This means you can insure your newer Ducati with full comprehensive (fuld kasko) and your older Honda with just liability, both sitting under the same bundled discount.

Most carriers apply standard eligibility conditions:

- All motorcycles must be titled to the same policyholder

- Bikes must be registered at the same address

- Most insurers require that policies be held under the same household

- Adding a second rider under 30 can trigger surcharges—Bauta applies a 3,550 DKK excess if the bike is lent to a young driver

Bundling also cuts admin time: one insurer for claims, one renewal date across all bikes, one billing cycle. For riders managing three or more motorcycles, that consolidation adds up quickly.

Comparing Multi-Bike Insurance Policy Types: What the Market Offers

Danish motorcycle insurance falls into three broad categories. They differ most on custom parts limits (10,000–50,000 DKK), how flexibly you can set per-bike coverage, and the quality of claims handling when something goes wrong.

Budget/Basic Multi-Bike Policies

These policies come from mass-market insurers like Tryg and Alm. Brand. They cover the mandatory liability requirements across all bikes and offer limited optional add-ons. The samlerabat discount exists but is often less generous than standard or specialist tiers.

| Coverage Scope | Multi-Bike Discount | Best Suited For |

|---|---|---|

| Liability-focused; limited comprehensive/collision options per bike | 10–15% typical range | Owners of older or lower-value bikes where full kasko is not cost-effective |

Budget policies trade flexibility for lower premiums. You get minimal breakdown assistance, no per-bike deductible customisation, and claims handlers who rarely specialise in motorcycle incidents. Custom parts limits reflect this: Tryg caps at 10,000 DKK and Alm. Brand at 15,000 DKK — workable for standard bikes, but a problem if you've invested in modifications.

Standard Multi-Bike Policies

Mainstream insurers like Topdanmark and Gjensidige offer dedicated motorcycle products with per-bike customisation of collision and comprehensive coverage. These policies include standard add-ons like roadside assistance (vejhjælp) and offer moderate bundling discounts.

| Coverage Scope | Multi-Bike Discount | Best Suited For |

|---|---|---|

| Full liability plus per-bike collision and comprehensive with customisable limits | 10–12% base; up to 22% with affinity memberships | Mixed fleets where per-bike flexibility matters (e.g., one high-value bike, one commuter) |

Key differentiating features:

- Whether the insurer allows different deductible levels per bike

- Accessories and modification limits: Topdanmark caps custom parts at 20,000 DKK; Gjensidige covers audio/tele equipment up to 30,000 DKK

- Topdanmark offers 22% off for MCTC members, stacking with their 12% samlerabat

Specialist/Premium Multi-Bike Policies

If Forsikring and specialist brokers build policies exclusively around motorcycles and high-value vehicles. Coverage reflects this: custom parts up to 50,000 DKK, nyværdi (new-value) payouts within the first 12 months, and claims teams with genuine motorcycle expertise.

| Coverage Scope | Multi-Bike Discount | Best Suited For |

|---|---|---|

| Higher custom parts limits, nyværdi payout window, optional trailer and gear coverage | 12–15% typical range; loyalty diminishing deductible programmes | Enthusiasts, collectors, or owners of newer/customised bikes where full replacement value matters |

Why specialist policies justify a higher premium:

- If Forsikring offers 50,000 DKK custom parts coverage — 5x the budget tier

- Nyværdi clauses pay out the cost of a brand-new equivalent if the bike is totalled within its first 12 months

- After 12 months, payouts revert to depreciated market value (handelsværdi), but specialist insurers use more favourable valuation methods

The gap between tiers is widest on custom parts and claims quality — two factors that rarely appear on a standard price comparison. Tools like Inzure can analyse your existing policy documents and show exactly where your current tier leaves you exposed before you commit to renewing.

Key Coverage Components Every Multi-Bike Policy Should Include

Liability coverage (ansvarsforsikring) is the legally required foundation. Under Færdselsloven §105, every registered motorcycle must carry liability insurance covering up to 50 million DKK for personal injury and 10 million DKK for property damage.

The state minimum may not be enough for riders managing multiple high-value bikes — consider higher limits if your total fleet value exceeds 500,000 DKK. Note that mandatory liability explicitly excludes coverage for the driver's own injuries; you must add a separate driver accident policy (førerulykkesforsikring) to protect yourself.

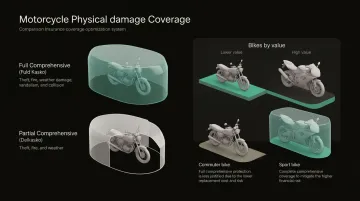

Physical damage coverage per bike comes in two tiers:

- Full comprehensive (fuld kasko): Covers theft, fire, weather, vandalism, and collision damage

- Partial comprehensive (delkasko): Covers theft, fire, and weather but excludes collision

Evaluate this per bike based on current market value. A 2015 commuter worth 30,000 DKK may not justify the cost of fuld kasko, while a 2024 sport bike worth 180,000 DKK should be fully covered.

Protection against uninsured drivers is not standard in Denmark. Check whether your insurer includes this or offers it as an add-on — particularly relevant if you ride frequently on rural roads or in areas with lower insurance compliance.

Add-ons worth evaluating:

- Roadside assistance (vejhjælp) — essential for multi-bike owners who ride year-round

- Custom parts and accessories coverage — limits vary from 10,000 DKK to 50,000 DKK; match to your total aftermarket modifications

- Riding gear coverage — some insurers cover helmets, jackets, and boots damaged in an accident

- Trailer coverage — useful for collectors transporting bikes to events or shows

How We Evaluated Multi-Bike Insurance Policies

Danish insurers are not legally required to make samlerabat discounts transparent or standardised. This means the burden of comparison falls entirely on you. The policies above were assessed on four dimensions:

- Can each bike be customised independently, or are you forced into a one-size-fits-all structure?

- Is the multi-vehicle saving clearly stated upfront, or buried in fine print and applied inconsistently?

- Are eligibility rules reasonable for typical multi-bike owners, or do they exclude common scenarios like adding a spouse as a secondary rider?

- How does the insurer handle motorcycle-specific incidents like custom parts damage or winter storage claims?

Knowing how policies were evaluated is only half the picture. These are the mistakes that cost riders the most:

- Assuming the cheapest combined premium is automatically the best deal without checking per-bike coverage limits

- Not comparing the bundled policy total against the sum of individual policy quotes from competing insurers

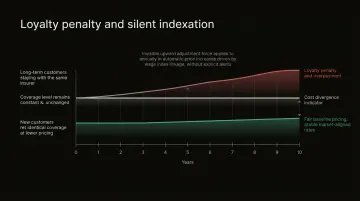

- Failing to check whether loyalty discounts erode over time as insurers quietly raise premiums

Forbrugerrådet Tænk's 2025 report revealed that consumers who remain with the same insurer for 10 years pay approximately 100 DKK more per month than new customers receiving identical coverage. This "loyalty penalty" is driven by silent indexation—insurers automatically raise premiums annually based on wage indices without explicitly notifying customers.

Benchmark your bundled premiums every 1-2 years. Inzure's policy analysis scans and compares policies across Danish insurers in under 60 seconds, flagging hidden costs, coverage gaps, and price discrepancies before they compound.

Conclusion

The smartest motorcycle insurance strategy in Denmark is bundling individual policies to unlock samlerabat discounts while matching the right coverage level to each bike. A rider with a 2024 BMW R 1250 GS and a 2010 Yamaha XT660 shouldn't pay for fuld kasko on both, but shouldn't sacrifice essential coverage just to lower the combined premium either.

Before committing, get quotes for a bundled policy structure and compare the total against separate individual quotes for the same bikes. Factor in per-bike coverage flexibility, custom parts limits, add-ons like vejhjælp, and the insurer's claims process, not just the headline price.

If comparing policies across Danish insurers manually feels overwhelming, Inzure's platform can analyse your existing policies, identify whether you're overpaying due to silent indexation, and show you what the market actually charges. There's no obligation to switch.

Frequently Asked Questions

Is it cheaper to insure multiple motorcycles?

Bundling under a samlerabat structure is typically cheaper than separate policies, as most insurers add additional bikes at a discounted rate. The actual saving depends on the insurer, the bikes involved, and the coverage levels chosen.

Can I insure multiple bikes?

Yes, most Danish insurers allow you to bundle two or more motorcycles under a portfolio discount structure. Common eligibility requirements include same owner and same registered address.

What does a multi-bike insurance policy typically cover?

Liability coverage applies across all bikes on your bundled portfolio, while physical damage coverage is set individually per bike—so you can choose fuld kasko for a newer model and ansvarsforsikring for an older one under the same discount structure.

How many bikes can be on one motorcycle insurance policy?

The limit varies by insurer—common limits are three to five motorcycles per bundled portfolio. Tryg, Topdanmark, and If typically allow up to four bikes; specialist insurers may accommodate larger collections. Check with your provider for specific limits.

Do all bikes on a multi-bike policy need the same coverage level?

No, physical damage coverages are bike-specific and can be set differently per motorcycle. This flexibility is one of the key advantages of bundling—allowing owners to tailor coverage to each bike's value while still benefiting from the samlerabat discount.

What restrictions typically apply to multi-bike motorcycle insurance?

All bikes usually must be owned by the same policyholder, registered at the same address, and stored at the same location. Some insurers apply surcharges if a rider under 30 uses any bike in the portfolio, and all policies must remain active to maintain the samlerabat discount.