The stakes are real. Switching carelessly can mean coverage gaps, unexpected fees, or trading one bad deal for another equally poor one. But switching strategically — with the right information — can save thousands of kroner annually while improving your actual protection. This guide covers the five most critical considerations before switching, so you can make a confident, well-informed decision without falling into common traps.

Key Takeaways

- Switching insurance is about finding better value, not just a lower premium

- Always compare coverages, limits, and exclusions side-by-side before deciding

- Never cancel your old policy before confirming your new one is active

- Loyal customers pay 7-8% more than new customers at the same insurer, so it pays to check your rate every year

- Factor in cancellation fees, open claims, and loyalty perks before you commit to switching

Why People Switch Insurance Providers

The most common triggers for switching are straightforward: premium increases at renewal, poor claims handling, major life changes (new home, growing family), or discovering you've been overpaying compared to market rates. What catches most Danes off guard is the hidden price creep that happens automatically.

Many insurers raise premiums each year through automatic wage indexation — tied to private-sector wage growth — without directly notifying customers. According to research by Konkurrence- og Forbrugerstyrelsen (KFST), these automatic increases suppress switching because customers never see a clear "your price has changed" notification.

A Forbrugerrådet Tænk survey found that most respondents don't even know whether their premiums are rising automatically.

The financial impact is substantial:

- The average Danish household pays over 5,000 kr more per year for non-life insurance than if prices had followed general inflation

- After 10 years with the same insurer, loyal customers pay 7-8 percentage points more than new customers with identical risk profiles

- Some individual policies show price differences of over 400 kr between long-term and new customers for the same coverage

Switching, done correctly, isn't risky. It does require knowing what to check before you move — and that's what the rest of this guide breaks down.

5 Key Considerations When Switching Insurance Providers

The difference between a smart switch and a costly mistake comes down to evaluating five specific factors. Each one connects directly to real financial and coverage outcomes that only become visible when you need to file a claim or cancel a policy.

Consideration 1: Compare Coverage Depth, Not Just Premium Price

A lower premium is worthless if it reflects fewer protections, higher deductibles, or narrower terms. Price-only comparisons are dangerous because the gaps only become visible when you file a claim and discover critical exclusions.

What to compare side-by-side:

- Does the new policy cover liability, legal aid (retshjælp), bicycle theft (cykeltyveri), and every protection your current policy includes?

- A liability cap of 5 million kr is fundamentally different from 10 million kr, even if both policies use the same label

- A 500 kr deductible versus 2,000 kr changes your out-of-pocket cost every time you file a claim

- Check exclusion clauses for specific situations like dog ownership, drone use, or hosted events — these often only appear in fine print

Common gaps identified in Danish policies:

- Missing legal aid insurance, which is among the most frequently used protections

- Inadequate bicycle coverage for high-value e-bikes or cargo bikes

- Family members not registered (newborns, partners) despite being eligible for coverage

- Liability exclusions that only appear in fine print

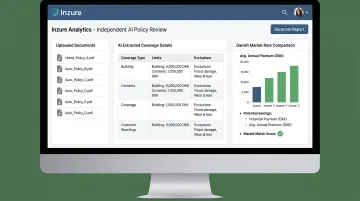

Inzure's AI-powered policy analysis reads your current policy's fine print in 60 seconds, mapping out exactly what you're covered for today. This gives you a clear benchmark to compare against new offers, ensuring you're not trading comprehensive protection for a superficially lower price.

Consideration 2: Understand Cancellation Fees and Refund Rights

Switching mid-policy can trigger fees at some insurers, while others allow penalty-free cancellation. Check your current policy terms before assuming you can leave without cost.

Your legal rights under Forsikringsaftaleloven:

- Section 16 mandates that insurers refund unused premiums on a pro-rata basis when you cancel mid-term

- If you've prepaid for six months of coverage but cancel after three months, you're entitled to a refund for the remaining three months

Typical administrative fees in practice:

- Customers with 1+ year of tenure: approximately 60 kr cancellation fee

- Customers with less than 1 year: up to 500 kr fee

- Cancellation at renewal: free, with one month's notice required

Always confirm your refund amount in writing before canceling. If your new policy saves you 3,000 kr annually but your old insurer charges a 500 kr cancellation fee, you'll still come out ahead — most switchers recoup that fee within the first month of savings.

Consideration 3: Evaluate the New Provider's Claims Handling Record

A lower premium means nothing if the insurer delays claims, underpays settlements, or rejects valid requests. When you file a claim, the quality of that process determines whether the policy was worth buying in the first place.

Where to check claims reputation:

- Ankenævnet for Forsikring publishes per-insurer complaint statistics, showing how many disputes each company faces and how they're resolved

- EPSI Rating satisfaction scores: The 2024 study shows a 6.7-point spread between top-rated insurers (GF Forsikring at 78.9) and bottom-rated ones (Codan at 72.2)

- Customer reviews on Trustpilot or independent forums

Questions to ask a prospective insurer:

- What is your average claims processing time?

- Do you offer direct claims reporting via app or online portal?

- How many claims were disputed or escalated to Ankenævnet last year?

In 2025, Ankenævnet handled 2,074 complaints. Rulings are binding on insurers unless they formally reject within 30 days — meaning an insurer's silence constitutes acceptance, which gives you a concrete legal foothold in any dispute.

Consideration 4: Eliminate the Risk of a Coverage Gap

Even a single day without active insurance exposes you to significant risk: rejected claims, future premium increases, and potential mortgage violations. Some mortgage agreements explicitly require continuous coverage, and a lapse can trigger penalties or legal issues.

The rule of thumb:

- Activate your new policy before canceling the old one

- Aim for at least a one-day overlap to ensure continuous coverage

- Get written confirmation of both the new policy start date and the old policy cancellation date

What happens during a gap:

- Any incident during the lapse period is entirely uninsured

- Insurers may penalize you with higher premiums if they see a coverage gap in your history

- If your policy is tied to a mortgage, a gap could violate loan terms

Under Forsikringsaftaleloven sections 86-87, policies tied to mortgages include a built-in 14-day buffer: cancellation only takes effect for the mortgage lender 14 days after they've been notified. That buffer reduces your legal exposure, but the safest move is still to avoid any gap entirely.

Once you've secured seamless continuity, there's a longer-term financial risk worth addressing before you commit to any new provider.

Consideration 5: Audit for Loyalty Penalties and Duplicate Coverages

The loyalty penalty is real and well-documented in Denmark. KFST's analysis of 7.4 million policies confirmed that after 10 years, customers pay 7-8 percentage points more than new customers with identical risk profiles. The penalty is even steeper for customers over 65 and those with lower educational attainment.

How the loyalty penalty works:

- Insurers offer aggressive discounts to attract new customers

- Long-term customers face automatic annual price increases that aren't clearly disclosed

- Over time, loyal customers subsidize discounts for new sign-ups

Duplicate coverage waste:

Switching is an ideal time to audit for redundant protections that inflate premiums without adding value:

- Travel insurance: Often covered by credit cards (e.g., MasterCard), the Danish public health card (det gule sundhedskort) for EU travel, or bundled with home contents insurance

- Bicycle theft: May be duplicated across home insurance and standalone policies

- Roadside assistance: Frequently bundled in auto policies and purchased separately

- Cancellation insurance: Often already included in travel or home insurance

A 2026 GF Forsikring survey found that 16% of Danes either purchase overlapping travel insurance or travel with no coverage at all.

Common Mistakes to Avoid When Switching

Switching providers can backfire in predictable ways — and the consequences range from coverage gaps to paying more than you saved. These are the three mistakes worth avoiding:

1. Canceling the old policy before the new one is confirmed active

This is the single most expensive mistake. A coverage gap — even one day — can lead to rejected claims, higher future premiums, and mortgage violations. Always secure written confirmation of your new policy's start date before canceling the old one.

2. Switching based on price alone without checking pending claims

If you have an open claim, switching mid-process can create delays and disputed timelines. Your old insurer must still process any claims filed during your active policy period, but new insurers may delay activation until the claim is resolved. Wait until claims are settled before switching if you can.

3. Overlooking loyalty discounts, bundles, or no-claims bonuses

Before switching, check whether your current provider offers any of the following:

- Multi-policy discounts (for example, bundling home and accident insurance — common with Danish carriers like Tryg or Alka)

- No-claims bonuses for accident-free years

- Group discounts through your employer, union, or bank

These benefits should factor into your true cost comparison. If switching eliminates a 15% bundle discount, your new policy's savings need to exceed that loss — not just match it.

How Inzure Can Help You Switch with Confidence

The insurance industry makes policy comparison deliberately difficult. Policies use dense legal language, coverage details hide in fine print, and comparing prices means benchmarking dozens of variables across multiple providers manually.

Inzure is Denmark's first AI-driven, independent insurance platform built to solve this problem. It has no affiliation with any insurer, earns no commissions, and doesn't favor any carrier over another.

How Inzure's AI analysis works:

- Upload your current policies as PDFs or screenshots

- The AI reads and analyzes your coverage in 60 seconds, extracting details like limits, exclusions, and deductibles

- You receive a clear breakdown of what you're actually covered for, what's missing, and whether you're paying above market rate

- The system compares your policy against real-time data from major Danish insurers (Tryg, Topdanmark, Alka, Codan, and others)

Key features:

- No insurer affiliations — fully independent analysis every time

- Stores your policy documents securely on EU servers, GDPR-compliant

- Analyze your policies for free with no obligation to switch

- Only charges 20% of your annual savings if you choose to switch

The results speak for themselves. Hans Henrik Beck saved 48,000 kr per year after eight years with Tryg, cutting his premiums by 46%. Lise Nielsen discovered she had been without home contents insurance for over a decade — Inzure helped her add proper coverage and still save 24% annually.

Conclusion

Switching insurance providers can deliver real financial benefits — saving thousands of kroner per year while improving your actual protection — but only when approached with the right information. The lowest quote isn't always the best deal if it comes with coverage gaps, exclusion clauses, or a provider with a poor claims record.

The five considerations in this guide give you a framework for making a confident, well-informed decision:

- Comparing coverage depth, not just price

- Understanding cancellation fees and notice periods

- Evaluating claims handling reputation

- Eliminating coverage gaps during the transition

- Auditing for loyalty penalties on existing policies

Insurance needs shift over time. Treating this as an ongoing habit — not a one-time event — is what keeps you from drifting back into overpaying. A platform like Inzure can run a full policy analysis in 60 seconds, making it straightforward to check whether your current coverage still makes sense before your next renewal date.

Frequently Asked Questions

What should I consider before switching insurance providers?

Compare coverage details (not just price), check for cancellation fees and pro-rata refunds, ensure no gap in coverage between policies, and factor in loyalty benefits or open claims before making the move.

Can I switch insurance companies mid-policy, and what happens if I do?

You can typically switch at any time. Early cancellation may trigger an administrative fee (60-500 kr), and your old insurer remains responsible for claims filed during the active period. Unused premiums are refunded pro-rata under Forsikringsaftaleloven (the Danish Insurance Contracts Act) section 16.

Can I switch insurance if I have an open claim?

Yes, but wait until the claim is resolved to avoid administrative complications. Your original insurer is still obligated to process claims filed under the active policy, but new insurers may delay activation.

Will switching insurance providers affect my credit score?

No. Switching itself does not impact your credit score. Some insurers may run a soft credit check for quoting purposes, which does not affect your score.

How do I make sure there is no gap in coverage when switching?

Confirm your new policy's start date before canceling the old one. Overlap coverage by at least one day and get written confirmation of both the new activation and old cancellation dates.

How often should I review my insurance policies?

Review annually — ideally 30 days before renewal — and after any major life event (new vehicle, home purchase, family changes).