Introduction

Many whole life policyholders eventually reach a crossroads: premiums that once fit comfortably into the budget become difficult to sustain. Retirement income replaces a salary, unexpected financial hardship strikes, or life priorities simply shift. The instinct might be to let the policy lapse and walk away—but stopping payments doesn't always mean losing coverage entirely.

This guide explains exactly what reduced paid-up insurance is, how it works in practice, who it makes sense for, and what trade-offs you'll face before making what is often an irreversible decision. Knowing how this nonforfeiture option works helps you avoid walking away from years of accumulated cash value — often unnecessarily.

Key Takeaways

- Reduced paid-up insurance lets you stop paying premiums while keeping a permanently reduced death benefit

- The new benefit is calculated using your accumulated cash value, current age, and premium payment duration

- The tradeoff is significant: your death benefit drops considerably compared to the original policy

- The decision is typically irreversible, and most riders are eliminated upon conversion

- If your coverage needs have shrunk but you still want a permanent safety net, this option is worth weighing carefully

What Is Reduced Paid-Up Insurance?

Reduced paid-up insurance is a contractual nonforfeiture option available on whole life policies. It converts your existing policy into a fully paid-up policy with a lower death benefit, with no further premium payments required.

Why This Option Exists

Insurance law in most jurisdictions requires that whole life policyholders not simply lose all accumulated value if they can't afford premiums. The NAIC Standard Nonforfeiture Law for Life Insurance mandates that insurers provide nonforfeiture benefits—protections that prevent total forfeiture of your policy's value when payments stop.

What Reduced Paid-Up Insurance Is NOT

- Not a new policy you purchase from scratch

- Not a type of term insurance with temporary coverage

- Not the same as surrendering for cash—the coverage remains permanent (whole life), just at a reduced face value

How It Differs from Paid-Up Additions (PUAs)

PUAs are a strategy to actively add value to a policy you're still funding with premiums, typically using dividends to purchase additional small increments of coverage. Reduced paid-up is elected when you want to stop paying premiums entirely. One builds the policy up; the other preserves it at a reduced level. See paid-up additions explained for a full comparison.

Whole life policies offer three standard nonforfeiture options:

- Cash surrender - Take the cash value and terminate coverage

- Extended term insurance - Keep the original death benefit but only for a limited period

- Reduced paid-up insurance - Keep permanent coverage at a lower benefit level

Most U.S. states mandate these options to protect policyholders from losing everything when financial circumstances change.

How Does Reduced Paid-Up Insurance Work?

Reduced paid-up insurance operates through a defined conversion process: your existing policy's accumulated cash value is used as a single lump-sum payment to purchase a new, smaller paid-up whole life policy.

Triggering the Election

The process begins when you contact your insurer and formally request to elect the reduced paid-up nonforfeiture option. This is typically done in writing or through a policy service form.

Key requirements:

- Most insurers require a minimum period of premium payments before the policy qualifies

- According to NAIC Model Law 808, this is typically 3 full years for ordinary insurance, or 5 full years for industrial insurance

- This is a voluntary, policyholder-initiated decision—it's not automatic when payments lapse

- Once elected, the conversion is irrevocable in most cases

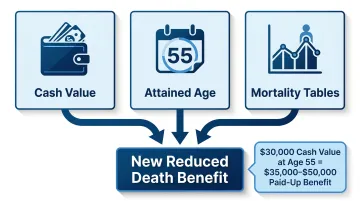

Calculating the Reduced Benefit

The insurer uses three primary factors to determine your new death benefit:

- Current cash value of the policy

- Your attained age at the time of conversion

- Standard actuarial mortality tables (such as the Commissioners 1980 Standard Ordinary Mortality Table)

In simple terms, your cash value acts as a one-time single premium to buy as much permanent coverage as it can at your current age.

To put this in concrete terms: a 55-year-old policyholder with $30,000 in accumulated cash value elects reduced paid-up. The insurer uses that $30,000 to calculate how much whole life coverage it can fund for life. Depending on the insurer's mortality tables and pricing, this might result in a $35,000–$50,000 death benefit—much less than the original policy face amount, but permanent and fully paid.

The exact reduction varies based on age, policy type, and insurer-specific actuarial assumptions.

What Happens to the Policy After Conversion

What changes:

- Death benefit drops to the newly calculated reduced amount

- All riders (disability waiver, critical illness, guaranteed insurability) are typically eliminated

- Policy continues as a standalone paid-up whole life contract

Despite these reductions, several core features of the original policy carry over intact.

What stays:

- Policy remains a permanent (whole life) contract

- Cash value continues to grow, though more slowly without ongoing premiums

- If the insurer is a mutual company, you may still receive dividends—though at a reduced level tied to the lower death benefit

- You retain the right to take policy loans against the cash value

Pros and Cons of Reduced Paid-Up Insurance

Pro 1 — Premium Relief with Retained Coverage

The primary benefit is eliminating all future premium obligations while maintaining permanent life insurance coverage for the rest of your life. That's especially valuable for:

- Retirees on fixed incomes who still want a death benefit for final expenses

- Those facing temporary or permanent financial hardship

- Policyholders who want to preserve a small legacy without ongoing financial commitment

Pro 2 — No New Medical Exam or Underwriting Required

Electing reduced paid-up is a contractual right, not a new insurance application. You don't need to prove insurability, making it accessible regardless of current health status. If you've developed medical conditions since the original policy was issued, this protection matters — you can't be denied based on current health.

Con 1 — Significant and Permanent Reduction in Death Benefit

The death benefit can drop substantially compared to the original policy. The exact reduction depends on accumulated cash value and your age, but it's rarely close to the original face amount.

Example of potential impact:

A $500,000 whole life policy with $75,000 in cash value might reduce to $100,000–$150,000 in coverage when converted at age 60. While this still provides meaningful protection, it's 70-80% less than the original benefit your dependents were expecting.

Con 2 — Irreversibility and Loss of Riders

Once elected, this decision cannot be undone in most policies. You cannot:

- Return to the original policy terms

- Reinstate eliminated riders

- Resume contributing premiums to grow the policy

Riders such as disability waiver of premium, critical illness coverage, or guaranteed insurability options are generally discontinued upon conversion. Review every active rider on your policy before making this call — once they're gone, you can't get them back.

Reduced Paid-Up vs. Other Nonforfeiture Options

Reduced paid-up is one of three main nonforfeiture paths. Here's how they compare:

| Feature | Cash Surrender | Extended Term | Reduced Paid-Up |

|---|---|---|---|

| Coverage duration | None (policy ends) | Limited years only | Lifetime (permanent) |

| Death benefit | None | Original face amount | Reduced amount |

| Future premiums | None | None | None |

| Cash value | Paid out immediately | Consumed over time | Continues to grow |

| Dividends | N/A | Usually not available | Continues (if participating) |

| Policy loans | N/A | Usually not available | Available |

| Riders | N/A | Generally discontinued | Generally discontinued |

The right choice depends on your priorities right now:

- Cash surrender works if you need liquidity immediately and already have coverage elsewhere

- Extended term fits when you need the full death benefit for a defined period — say, until a mortgage is paid off or children finish college

- Reduced paid-up suits you if permanent, lifelong coverage matters more than the coverage amount, and you're done paying premiums

There's also a structural difference worth understanding. With extended term, the cash value is consumed over time and coverage ends when it runs out. With reduced paid-up, the policy is contractually paid in full and cash value continues to grow — making it the stronger choice if you're building long-term cash value.

On the tax side, electing reduced paid-up is generally not a taxable event because the policy stays in force. Cash surrender triggers taxes if the cash value exceeds total premiums paid — a meaningful cost to factor in before choosing that route.

Who Should (and Shouldn't) Choose Reduced Paid-Up Insurance

Best Suited For

Reduced paid-up insurance makes sense if you:

- Are entering retirement and no longer need the full original death benefit (children are grown, mortgage is paid off)

- Are experiencing financial hardship and cannot sustain premiums

- Want to maintain some lifelong death benefit without further financial commitment

- Have accumulated meaningful cash value in the policy (typically after paying premiums for at least 5-10 years)

Before making this decision, confirm your policy's current cash value with your insurer. This single number determines how much death benefit you'll retain — and whether the reduced amount is actually worth keeping.

Not Suited For

This option is not the right fit if you:

- Have a newer policy that has built little cash value (the resulting reduced benefit may be negligibly small)

- Depend heavily on riders attached to the original policy (such as disability waiver or critical illness coverage)

- Have significant outstanding financial obligations whose dependents would need maximum coverage

- Expect your financial situation to improve in the near future

Consider Alternatives First

Before electing reduced paid-up, review premium offset (also called "premium vacation"). This strategy uses dividends and cash value to cover ongoing premiums, eliminating out-of-pocket payments while preserving more flexibility.

Premium offset is typically reversible—if your financial situation improves, you can resume paying premiums and continue building the policy. Reduced paid-up, by contrast, is permanent.

Frequently Asked Questions

How does reduced paid-up insurance work?

Your accumulated cash value is used as a single lump-sum payment to purchase a permanent whole life policy with a lower death benefit, requiring no future premiums. The amount of coverage depends on your cash value, age, and the insurer's actuarial tables.

What can you do to reduce the premium you pay for insurance?

On whole life policies, you can elect reduced paid-up (stops premiums but reduces coverage), use premium offset (dividends cover premiums), or downsize coverage through policy modification. Comparing market options can also reveal more cost-effective alternatives.

Do I get all my money back with ROP?

No. Reduced paid-up insurance is not a return-of-premium (ROP) product. With reduced paid-up, the cash value funds continued coverage rather than being returned to you. If you want a full cash return, cash surrender is the option to explore.

Can I reverse the decision to elect reduced paid-up insurance?

In virtually all cases, electing reduced paid-up status is irrevocable. Once converted, you cannot return to the original policy terms or resume premium payments to grow the policy.

What happens to my riders when I elect reduced paid-up insurance?

Most riders on the original policy—disability waiver of premium, critical illness, guaranteed insurability—are eliminated upon conversion. Review which riders you'd lose before making the decision.

What is the difference between reduced paid-up insurance and extended term insurance?

Extended term keeps the original death benefit amount but only for a fixed number of years funded by your cash value. Reduced paid-up lowers the death benefit but keeps coverage permanent for life. Extended term is better for maintaining maximum near-term coverage; reduced paid-up is better for lifelong coverage with ongoing cash value growth.