Introduction

By 2026, AI predictive analytics has quietly rewritten who holds the information advantage in insurance. Insurers now access real-time risk data that lets them price policies with granular precision — while most consumers have no idea how their premium was calculated. A 2023 industry survey found 88% of property insurers and over 90% of health insurers globally already use or plan to deploy AI/ML models in their pricing operations.

That gap — between what insurers know and what customers understand — is widening.

For insurers, predictive AI means sharper pricing, lower losses, and a real competitive edge. For consumers, it means paying premiums set by models they've never seen — and with no clear way to know if they're getting a fair deal.

Loyal customers often end up worst off. Algorithmic pricing strategies frequently penalize retention, charging long-term policyholders more than new customers for the same coverage. This article breaks down the leading AI solutions driving these changes in 2026, what they actually do, and how consumers can use that knowledge to push back.

Key Takeaways

- AI predictive analytics forecasts risk, prices policies, detects fraud, and flags churn — faster than manual underwriting can track

- Leading 2026 platforms — DataRobot, Gradient AI, Shift Technology, ZestyAI, and Friss — define insurer-side predictive intelligence

- Satellite imagery, telematics, medical records, and claims history feed these models to produce risk scores in seconds

- While insurers optimize profits using algorithms, consumer-side tools like Inzure help level the playing field by revealing true market rates

- Evaluate solutions based on data integration depth, model explainability, regulatory compliance, and deployment speed

What Is AI Predictive Analytics in Insurance?

Predictive analytics in insurance uses machine learning models trained on historical claims, demographic, behavioral, IoT, and third-party data to forecast future outcomes — including loss probability, fraud risk, churn likelihood, and premium adequacy.

Traditional actuarial models are rules-based and backward-looking. AI models, by contrast, recognize patterns across hundreds of variables, continuously learn from new data, and deliver insights that update in real time rather than annually.

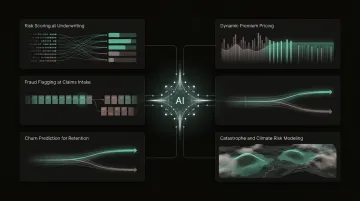

Major use cases include:

- Risk scoring at underwriting

- Dynamic premium pricing

- Fraud flagging at claims intake

- Churn prediction for retention campaigns

- Catastrophe and climate risk modeling

According to Deloitte's analysis, AI enables insurers to rapidly test multiple pricing models, identify key rating variables, and simulate economic scenarios—capabilities traditional actuarial methods cannot match.

The platforms reviewed below were selected based on data depth, model accuracy, and real-world deployment results — representing the most capable insurance-specific predictive modeling tools available in 2026. Worth noting: while these tools help insurers price risk, consumer-facing platforms like Inzure work the other side of that equation — analyzing your existing policies to show whether you're being overcharged relative to actual market rates.

Top AI Solutions for Predictive Analysis in Insurance 2026

These platforms were selected for their demonstrated use in insurance-specific predictive modeling—not generic analytics tools repurposed for the industry.

DataRobot

DataRobot is an enterprise AI platform enabling insurance companies to build, deploy, and monitor predictive models at scale. It covers risk scoring, loss ratio forecasting, pricing optimization, and customer lifetime value prediction, and is widely used by P&C and life insurers globally.

Its AutoML capability allows actuarial and data science teams to build accurate risk models without heavy coding, while model explainability features help compliance teams justify algorithmic decisions to regulators.

Results back this up: VidaCaixa, Spain's largest insurer, uses DataRobot for underwriting and life insurance payouts—automatically making payout decisions in one-third of cases and saving approximately 30 minutes per claim. French insurer Matmut achieved a 3x productivity gain across the end-to-end modeling lifecycle.

| Feature | Details |

|---|---|

| Key Features | AutoML for risk modeling, automated feature engineering, model monitoring, explainability dashboard |

| Best For | Insurers building pricing optimization, loss forecasting, or churn prediction models at enterprise scale |

| Compliance & Integration | Supports model governance, bias detection; integrates with major cloud environments and policy admin systems |

On the compliance side, DataRobot provides SHAP (Shapley Values) and XEMP explanations showing what drives predictions row-by-row. Its bias mitigation workflows test for algorithmic bias and apply corrective measures—such as pre-processing reweighing—to ensure fair treatment of protected classes.

Gradient AI

Gradient AI is a Boston-based insurtech specializing exclusively in AI for insurance. Its SAIL™ platform is trained on a proprietary data lake of tens of millions of policies and claims across workers' compensation, group health, and commercial lines.

Unlike general-purpose analytics platforms, its models are pre-trained on industry-specific data—delivering more accurate loss predictions with shorter time-to-value. The company secured $56.1 million in Series C funding in July 2024.

The performance numbers are specific: CCMSI reduced workers' compensation claim costs by 10%—translating to more than $300 million in savings for clients—by using Gradient AI to flag at-risk claims. A separate workers' comp study showed the platform reduced legal involvement in lost-time claims by 15%, yielding a 5% reduction in claim costs (approximately $3.5 million annually for studied insurers).

| Feature | Details |

|---|---|

| Key Features | Predictive loss scoring, underwriting risk evaluation, claims cost prediction, straight-through processing support |

| Best For | Workers' comp, group health, and commercial P&C insurers needing fast, accurate loss ratio predictions |

| Data Advantage | Proprietary industry data lake with tens of millions of insurance-specific claims and policy records |

Shift Technology

Shift Technology is an AI platform focused on claims and fraud intelligence. It uses predictive modeling to identify suspicious claims before payouts occur and to forecast claim severity and processing complexity at intake.

Its fraud detection models analyze behavioral patterns, geolocation inconsistencies, cross-carrier claim history, and image metadata—delivering predictive fraud scores in real time. Shift serves 115+ customers across 25 countries and has analyzed over 2.6 billion policies and claims.

Client results reflect the scale: AXA Switzerland renewed its partnership with Shift for five years in 2026 to detect suspicious activity in real time at first notice of loss. A separate client achieved a 4x ROI in year one by preventing unwarranted payments.

| Feature | Details |

|---|---|

| Key Features | Real-time fraud risk scoring, claim complexity prediction, anomaly detection, multi-carrier data analysis |

| Best For | P&C and health insurers looking to reduce fraudulent payouts and automate claims triage |

| Deployment | Integrates with core claims management systems; used by major global carriers across Europe and North America |

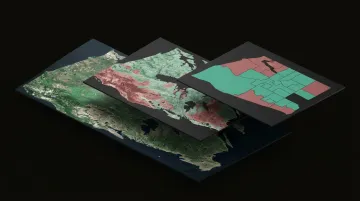

ZestyAI

ZestyAI uses computer vision applied to satellite and aerial imagery, combined with machine learning models trained on decades of catastrophe events, to produce property-level risk scores for wildfire, wind, hail, and flood.

The core differentiator is granularity: ZestyAI moves insurance beyond ZIP code-level risk buckets to parcel-level precision—enabling underwriters to price properties individually rather than by geographic averages. Berkshire Hathaway Homestate Companies deployed Z-FIRE™ across 12 states, confirming the model "outperformed our homegrown wildfire risk model."

Z-FIRE™ is trained on more than 1,400 wildfire events across 20+ years of historical loss data, using over 200 billion data points. The model outperforms traditional regional models by 44x in predictive power and correctly identified 94% of the area impacted by the Palisades Fire and 87% of the Eaton Fire as high or very high risk.

| Feature | Details |

|---|---|

| Key Features | Satellite imagery analysis, wildfire and climate risk scoring, vegetation and roof condition assessment, catastrophe modeling |

| Best For | Property and casualty insurers underwriting in climate-exposed regions with high wildfire, flood, or hail risk |

| Data Depth | Models trained on historical catastrophe events and billions of property-level data points from aerial imagery |

Friss

Friss is a purpose-built insurance AI platform delivering real-time risk scoring and fraud detection across the policy lifecycle—from application intake to claims settlement.

Where Friss stands out is coverage breadth: its predictive scores address application fraud at policy intake—not just claims—reducing the risk of insuring bad actors before any claim occurs. It integrates directly with core insurance systems for straight-through risk decisioning.

Scale reflects adoption: Friss has completed over 300 implementations across 45+ countries. UNIQA Insurance Group achieved total fraud savings of $21 million within the first two years of deployment, with rollout averaging four months per country. Fraud savings per investigator grew from $550,000 to $2 million.

| Feature | Details |

|---|---|

| Key Features | Real-time risk scoring at application and claim, behavioral analytics, third-party data integration, transparent scoring rationale |

| Best For | Insurers seeking end-to-end predictive fraud prevention from policy issuance through claims settlement |

| Compliance | Provides explainable AI scoring rationales to support regulatory transparency requirements |

How We Chose These AI Solutions

These five platforms were selected based on four criteria:

Insurance specificity: Platforms built for insurance from the ground up — not general analytics tools adapted after the fact. Gradient AI and ZestyAI, for example, train exclusively on insurance data, delivering accuracy that general-purpose tools cannot match.

Predictive model performance: Demonstrated accuracy in real insurer deployments. We prioritized vendors with verifiable client outcomes—like CCMSI's $300 million in savings or ZestyAI's 44x improvement over traditional models.

Data integration depth: Ability to ingest structured and unstructured data from multiple sources. Leading solutions process satellite imagery, telematics, medical records, and behavioral data—not just policy admin system outputs.

Regulatory readiness: Model explainability and compliance with standards like NAIC AI principles or EU AI Act requirements. The EU AI Act classifies life/health pricing as "high-risk," and 25 U.S. states had adopted the NAIC Model Bulletin by early 2026. Opaque models that cannot explain their decisions face increasing regulatory rejection in both markets.

Understanding these criteria also reveals where buyers commonly go wrong. The most frequent mistakes include:

- Choosing general-purpose ML platforms without insurance-specific training data

- Underestimating time to value if models must be trained from scratch

- Ignoring model explainability—which regulators increasingly require for automated underwriting or claims decisions

Conclusion

In 2026, AI predictive analytics is no longer a differentiator in insurance—it is the baseline. The platforms covered here show how far insurers have moved toward automating risk decisions, fraud detection, and pricing—and how quickly that gap between insurer capability and consumer visibility is widening.

As insurer-side AI grows more sophisticated, the information gap between insurers and policyholders widens. Insurers know exactly how a risk profile has been scored; most consumers never see that picture. That asymmetry is where consumer-side tools matter. Inzure, for example, applies AI to your existing policies to show whether you're paying a fair market price, flag coverage gaps, and surface duplicate coverage—in about 60 seconds.

The next frontier is real-time adaptive pricing and agentic AI—systems that don't just score risk once at underwriting, but continuously adjust coverage recommendations as your circumstances change. For consumers, that means the price you accepted last year may already be outdated. Knowing how these systems work, and having tools to check your position against the current market, is the practical advantage that matters.

Frequently Asked Questions

Which AI is best for predictive analytics?

There is no single "best" platform—the right choice depends on your use case. For insurance-specific loss prediction, Gradient AI leads; for property risk, ZestyAI; for fraud, Shift Technology or Friss; for enterprise multi-use modeling, DataRobot. Insurance-specific training data typically outperforms general-purpose tools.

How does AI predictive analytics affect my insurance premium?

Insurers use AI models to score individual risk based on claims history, telematics, property condition, and behavioral patterns. Premiums reflect individualized risk rather than broad demographic averages. This benefits low-risk individuals but can disadvantage loyal long-term customers through price optimization practices.

What data do insurance companies use for AI-powered risk scoring?

Common data inputs include:

- Historical claims records and credit scores

- Telematics and IoT sensor data

- Satellite property imagery

- Medical records (health/life lines)

- Social patterns and third-party databases

The breadth of data used varies by line of business and local regulations.

Can AI in insurance lead to unfair pricing for consumers?

Yes—algorithmic bias and price optimization (charging loyal customers more because models predict they won't switch) are recognized risks. EU regulators are actively scrutinizing AI pricing models for fairness, and U.S. counterparts (NAIC) are following suit. Consumers can protect themselves by regularly benchmarking premiums against the market.

What is the difference between predictive analytics and traditional actuarial methods in insurance?

Traditional actuarial methods use historical averages and statistical tables to group policyholders into broad risk categories. AI predictive models identify non-linear patterns across hundreds of variables to produce individualized risk scores. They update continuously as new data arrives, rather than waiting for annual model refresh cycles.

How is AI changing underwriting speed in insurance?

AI has compressed standard underwriting decisions from days to minutes in many lines. Hiscox reduced underwriting time from 3 days to 3 minutes using Google Cloud, while John Hancock's GenAI "Quick Quote" slashed preliminary assessments from 1 day to 15 minutes. Predictive models handle routine risk assessment automatically, freeing underwriters to focus on complex cases.