Introduction

The insurance industry—historically resistant to change and notorious for opacity—is now changing fast. AI is rewriting how insurers assess risk, process claims, and talk to customers.

For policyholders, that shift cuts both ways. Industry research shows 70% of home insurers now use or plan to use AI, and early adopters are generating returns 6.1 times higher than laggards. Insurers are getting sharper tools. The question is whether consumers get fairer outcomes alongside them.

If you're tired of opaque pricing and policy language designed to confuse, these AI developments will directly affect what you pay and what protection you actually receive.

Key Takeaways

- Underwriting, claims, fraud detection, and customer service are all faster thanks to measurable AI-driven gains

- Machine learning enables risk assessment in seconds, cutting timelines that once took days

- Consumer-facing AI tools shift power dynamics, exposing overpayments and coverage gaps

- Agentic AI represents the next frontier with autonomous multi-step workflows

- Regulatory bodies like EIOPA and Denmark's Finanstilsynet are developing active AI oversight frameworks

AI-Powered Underwriting and Smarter Risk Assessment

Machine learning models now analyze vast datasets—IoT sensors, telematics, behavioural signals, third-party sources—to assess risk with precision that traditional actuarial tables never achieved. The result is a fundamental shift from slow batch processing to real-time decision-making.

Real-World Adoption and Speed Gains

The NAIC reports 70% of home insurers currently use, plan to use, or are exploring AI and machine learning for renewal evaluations, policy verification, and rate calculations. Insurers are reducing quote turnaround from days to minutes, and Accenture forecasts AI use in underwriting will jump from 14% today to 70% within three years.

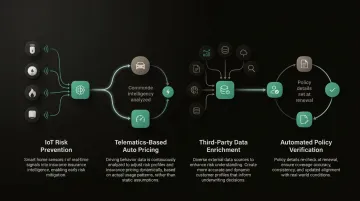

Key applications include:

- IoT integration for proactive risk prevention (smart leak detectors, fire sensors)

- Telematics-driven auto pricing based on actual driving behaviour

- Third-party data enrichment for more accurate risk profiles

- Automated policy characteristic verification at renewal

Consumer Impact: Fairer Pricing for Lower-Risk Customers

These underwriting advances directly affect what consumers pay. More accurate risk profiling means lower-risk customers escape blunt demographic pricing — instead of paying inflated premiums based on their postal area or age group, consumers with demonstrable safe behaviours receive fairer, more competitive rates.

Why this trend is accelerating:

- Competitive pressure to offer instant digital quotes

- Consumer expectations shaped by faster services in other industries

- Rapid growth in behavioural and sensor data from connected devices

- Cost efficiency gains that directly improve insurer margins

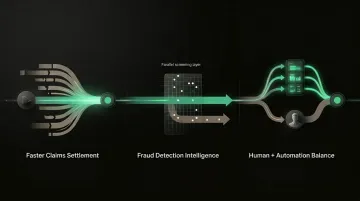

Automated Claims Processing and AI-Powered Fraud Detection

AI now handles the full claims lifecycle — submission, damage assessment via computer vision, coverage verification, and settlement — cutting the manual workload for adjusters significantly. Machine learning, running in parallel, catches fraud patterns that rules-based systems routinely miss.

Aviva's 80+ AI Models Cut Processing by 23 Days

UK insurer Aviva deployed more than 80 AI models across claims, cutting liability assessment time by 23 days, improving routing accuracy by 30%, and reducing customer complaints by 65%. The transformation saved Aviva over 522 millioner DKK in 2024.

Allianz's Project Nemo reduces simple food spoilage claims from days to minutes—an 80% reduction in processing time—using seven AI agents that collaborate autonomously across intake, coverage review, fraud checks, and payout preparation.

The 97-Billion-DKK European Fraud Problem

Insurance Europe estimates fraud costs European insurers and customers 97 milliarder DKK om året. In the US, the Coalition Against Insurance Fraud puts the figure at 2.160 milliarder DKK. Machine learning identifies subtle anomalies across hundreds of variables simultaneously—claim timing, linguistic inconsistencies, behavioural patterns—uncovering schemes that evade traditional detection.

Aviva reported a 39% increase in fraud detection in 2023, stopping 1.009 millioner DKK in fraudulent claims, followed by a further 14% increase in 2024, blocking 1.105 millioner DKK.

These results point to three concrete shifts reshaping how insurers operate:

- Faster settlements improve customer satisfaction at moments of high stress

- Fraud detection protects premium revenue without penalising legitimate claimants

- Automation frees adjusters to handle complex edge cases requiring human judgment

Hyper-Personalisation and Consumer-Facing AI Transparency

AI enables individualised policies tailored to each policyholder's behaviour and risk profile—think usage-based pricing, predictive alerts, and proactive coverage reviews. Beyond insurer-side optimisation, AI is now working for consumers directly, surfacing pricing gaps and coverage problems that were previously invisible.

From Insurer-Side Personalisation to Consumer Empowerment

Deloitte research shows 78% of consumers want tangible savings from personalisation, and brands delivering standout personalised value report 45% higher conversion and 50% higher engagement.

But the most significant shift isn't just better insurer targeting—it's AI tools that work for the consumer, not the insurer. Platforms like Inzure analyse existing policies in seconds, identifying overpayments, missing coverages, and duplicates, then show consumers the real market price for their insurance. Consumers can now see exactly what they're paying, what they're missing, and what they could pay elsewhere — without relying on the insurer to tell them.

The Loyalty Penalty: 7-8% Higher Premiums for Longstanding Customers

A 2025 Danish Competition and Consumer Authority report found that Danish households spend approximately 16,000 DKK annually on non-life insurance—4.4% of total consumption. Yet customers with ten years of seniority pay 7-8 percentage points more than new customers with identical risk profiles.

Consumer comparison tools in Denmark now cover 86% of the market, forcing insurers to compete on genuine value rather than customer inertia. AI-powered tools like Inzure extend that pressure further — catching not just price differences between carriers, but the premium creep that comparison sites alone don't flag.

Consumer-facing AI delivers:

- Instant policy document analysis (PDF or photo upload)

- Coverage gap identification (missing protections)

- Duplicate coverage flagging (overpayment elimination)

- Real market pricing comparison across carriers

- Ongoing monitoring alerts when better options emerge

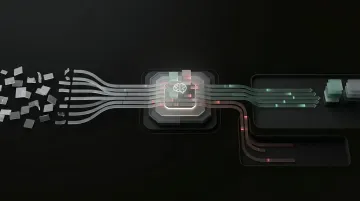

Agentic AI and Fully Automated Insurance Workflows

Agentic AI refers to multi-agent systems capable of reasoning, collaborating, and executing complex multi-step tasks autonomously—far beyond single-function chatbots or simple automation tools.

Multi-Agent Systems Orchestrating End-to-End Processes

Leading insurers now deploy separate AI agents for intake, risk profiling, pricing, compliance review, and decision orchestration, escalating to humans only for genuine edge cases. Allianz's Project Nemo puts this into practice with seven specialized agents working in concert to process food spoilage claims in under five minutes:

- Planner — coordinates task sequencing across agents

- Cyber — assesses digital exposure and fraud vectors

- Coverage — verifies policy terms and applicable clauses

- Weather — cross-references meteorological event data

- Fraud — flags anomalies and suspicious patterns

- Payout — calculates settlement amounts

- Audit — reviews the full decision trail before sign-off

Gartner predicts that by 2029, agentic AI will autonomously resolve 80% of common customer service issues without human intervention.

The Competitive Imperative: 6.1x Higher Returns for AI Leaders

McKinsey research shows AI leaders in insurance have generated 6.1 times the Total Shareholder Return of laggards over the past five years. Insurers running isolated pilots without domain-wide transformation are falling behind, and the gap is widening.

The McKinsey data makes the stakes concrete: carriers that adopted AI across their full operations — not just in isolated pilots — captured that 6.1x return advantage. Those that didn't are now competing against systems that price, process, and settle faster than any human workflow can match.

What's Driving These AI Trends in Insurance

Four converging forces are pushing insurers toward AI adoption — and none of them are slowing down.

Technology Enablers

Key developments making AI viable at scale:

- Massive datasets from IoT sensors, telematics, and digital interactions

- Cheaper, faster cloud computing reducing infrastructure barriers

- Large language models and computer vision enabling document analysis and claims automation

- Open-source frameworks lowering development costs

Gartner forecasts that by 2030, LLM inference costs will drop over 90%, making AI applications economically viable across all insurance functions.

Consumer Expectations and Competitive Pressure

Consumers accustomed to instant, personalised digital experiences in retail, banking, and travel now expect the same from insurance. Early AI adopters are gaining market share by delivering it.

Rising Cost Pressure

The Insurance Information Institute reports loss and loss adjustment expense (LAE) ratios for homeowners insurance reached 73.4% in 2024, with adjusting expenses accounting for 6.6% of premiums. Even marginal AI-driven improvements deliver massive value when applied across millions of policies.

Regulatory Development

The NAIC adopted the Model Bulletin on AI in December 2023, requiring insurers to develop AI governance programmes. Twelve US states are piloting the NAIC AI Systems Evaluation Tool from March to September 2026, allowing regulators to assess AI models during market conduct exams. In Europe, the EU AI Act classifies certain insurance AI applications as high-risk, requiring transparency and human oversight — a framework that directly shapes how Danish insurers deploy automated decisioning. Together, these developments legitimise broader AI investment while setting clear consumer protection boundaries.

How AI Is Reshaping Insurance: Industry Impacts and Future Outlook

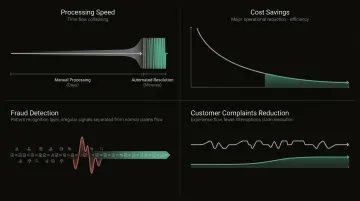

AI's impact on insurance isn't theoretical — it's measurable across claims speed, operating costs, and fraud detection. Here's what the data shows across core functions, competitive dynamics, and the workforce shift already underway.

Operational Impact: Speed, Cost, and Accuracy Gains

Documented improvements across core functions:

- Processing speed: Claims reduced from days to minutes (80% reduction)

- Cost savings: 522 millioner DKK annual savings for major insurers deploying comprehensive AI

- Fraud detection: 39-53% increase in fraudulent claims identified

- Complaint reduction: 65% fewer customer complaints through faster, more accurate claims handling

Business and Competitive Impact: The Widening Performance Gap

The gap between AI leaders and laggards is now a financial one. McKinsey research shows AI-forward insurers have generated 6.1x higher Total Shareholder Returns than peers over five years. Insurers running isolated pilots without enterprise-wide transformation are falling behind — and the distance is growing each quarter.

Workforce and Organisational Impact: The Mid-Career Reskilling Crisis

Accenture research reveals 55% of insurance workers worry about AI-related stress and burnout, while 50% fear job displacement. McKinsey notes around 75% of current roles will need reshaping with new skill mixes as AI embeds across workflows.

The role shift is already visible:

- Manual data processing is being automated, pushing professionals toward judgment and relationship work

- AI oversight and prompt-management skills are becoming standard requirements at mid-career level

- Insurers that delay reskilling programmes are already reporting difficulty filling specialist roles

Organisations that treat this as a people problem — not just a technology rollout — are seeing faster adoption and fewer implementation failures.

Future Signals to Watch

Three near-term developments reshaping insurance:

- Real-time, continuous risk monitoring replacing annual policy review cycles—IoT sensors enabling dynamic pricing adjustments based on actual behaviour

- Normalisation of agentic AI in end-to-end onboarding and claims, with multi-agent systems handling 80%+ of standard workflows autonomously

- Growing consumer demand for independent AI tools that audit insurer pricing, surface loyalty penalties, and flag coverage gaps — shifting power toward consumers who know what their policy should actually cost

Frequently Asked Questions

How is AI currently used in the insurance industry?

AI is embedded across the insurance value chain. Core applications include:

- Underwriting risk models that price policies more accurately

- Claims processing using computer vision and machine learning

- Fraud detection through anomaly analysis

- Customer service via chatbots and virtual assistants

Adoption ranges from simple automation to sophisticated multi-agent systems.

Will AI replace insurance agents and underwriters?

AI augments rather than replaces human roles. It handles routine data tasks while humans focus on complex judgment, relationship management, and edge cases requiring empathy. Around 75% of roles will be reshaped, not eliminated.

What are the main risks of using AI in insurance?

Key risks include algorithmic bias creating unfair pricing, data privacy concerns with sensitive personal information, regulatory compliance complexity across jurisdictions, and over-reliance on automated decisions without adequate human oversight or explainability.

How does AI in insurance benefit consumers directly?

AI delivers faster claims settlements (hours instead of weeks), fairer pricing based on actual behaviour rather than demographic stereotypes, 24/7 service availability, and the emergence of independent AI tools that help consumers identify overpayments and coverage gaps.

What is agentic AI and why does it matter for insurance?

Agentic AI refers to systems where multiple specialised agents collaborate autonomously across complex, multi-step workflows. Unlike single-function tools, these systems handle end-to-end process automation, escalating to humans only for edge cases.

How are regulators responding to AI use in insurance?

The NAIC adopted the Model Bulletin on AI in December 2023, requiring AI governance programmes. Twelve states are piloting the AI Systems Evaluation Tool in 2026. Insurers remain responsible for compliance regardless of whether decisions are made by humans or AI.