Introduction

Picture this: You're renewing your home insurance, glancing at the premium and thinking, "That's just what it costs." Behind that number, though, an AI algorithm may have already analyzed your risk profile, predicted how likely you are to switch providers, and priced your policy accordingly.

Insurance companies have invested heavily in AI for years. The technology promises speed and efficiency — but those benefits don't automatically reach you.

In fact, loyal customers in Ireland paid 32% more for home insurance than new customers—a gap AI pricing models can amplify.

That loyalty gap is no accident — and it's not unique to Ireland. This guide breaks down exactly how AI is reshaping insurance pricing, what's happening behind the scenes when your premium is calculated, and what you can do to stay on the right side of those algorithms.

TLDR: Key Takeaways

- AI already sets prices, processes claims, and detects fraud across Danish insurers—this is happening now

- Personalized pricing cuts premiums for low-risk customers but raises them for others—your data profile determines which camp you're in

- Simple claims resolve in minutes; complex cases still need human review, and automated errors do occur

- AI tools can scan your existing policies for overpricing and coverage gaps before your next renewal

- Long-term customers often pay up to 32% more than new customers for the exact same coverage

How AI Is Already Working Inside Your Insurance

AI isn't just powering chatbots—it's embedded across the entire insurance value chain. Here's where Danish consumers encounter it most:

Underwriting and Risk Assessment

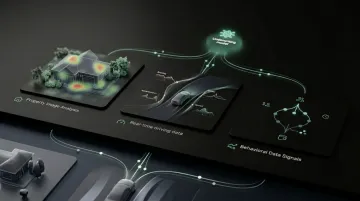

AI now analyzes far more data points than traditional actuaries ever could:

- Property images: Self-guided mobile inspection apps like Tractable's AI Property and Yembo's ScanMyHome let you photograph your home via smartphone, eliminating on-site inspectors

- Telematics data: Driving behavior tracking records acceleration, braking, speed, and cornering

- Behavioral signals: Click patterns, time spent reviewing quotes, and policy renewal timing all feed risk models

This granular analysis assigns each individual a precise risk score, moving beyond broad demographic categories toward personalized pricing.

Customer Service and Chatbots

Major Nordic insurers are deploying generative AI for 24/7 customer support:

- If Insurance's IfGPT: Launched in September 2025, handling over 8,000 customer interactions by Q4 2025

- Rule-based vs. generative AI: Traditional chatbots follow decision trees; generative AI understands context and produces natural responses

- Scale: These systems are projected to handle 200,000+ queries annually

Rule-based bots recognize keywords and route you to pre-written answers. Generative AI comprehends your question and drafts a custom response—a meaningful distinction when you're trying to resolve a complex claim.

Claims Processing

AI can now summarize complex legal settlements and assess damage instantly:

- Document summarization: 85% of enterprise GenAI adoption includes text generation, specifically for summarizing documents

- Speed gains: Allstate uses GPT models to draft nearly all of its 50,000 daily claims emails before human review

- Photo-based assessment: Upload car damage photos, and AI estimates repair costs in seconds

Minor claims that once took days now resolve in hours. That speed comes with a caveat: algorithms are increasingly making coverage decisions with minimal human oversight.

Fraud Detection

AI analyzes patterns across massive datasets to flag suspicious claims:

- Projected savings: Deloitte estimates AI-driven fraud analytics could save P&C insurers 560-1.120 milliarder DKK by 2032

- Current detection rates: 20-40% for soft fraud, 40-80% for hard fraud, with AI potentially boosting these by 20-40%

- Consumer benefit: Less fraud means lower overall premium costs for honest policyholders

The downside is false positives. When the algorithm flags a legitimate claim as suspicious, real policyholders face delays—sometimes for weeks—while the insurer investigates.

AI and Your Premium: Will You Pay More or Less?

AI doesn't automatically mean cheaper insurance. Instead, it enables more granular, individualized pricing—which can work in your favor or against it, depending on your profile and behavior.

Usage-Based and Behavior-Linked Pricing

Telematics programs in Europe consistently demonstrate AI's pricing impact:

| Insurer | Country | Premium Impact |

|---|---|---|

| HUK-Coburg | Germany | 10% upfront discount; up to 30% savings at renewal for safe driving |

| UnipolSai | Italy | 10-15% discounts based on kilometers and driving habits |

| ERGO | Europe | 10% upfront discount with further reductions for good habits |

Low-risk drivers save 10-30%, but higher-risk profiles face increases. AI shifts from static annual assessments toward dynamic, real-time pricing based on actual behavior.

Smart-home sensors follow similar logic. Monitor your property, prove you're low-risk, and premiums drop. Decline to share data, and you'll likely pay what insurers call an "uninformed risk" premium instead.

The Loyalty Penalty Problem

AI can actually work against long-term customers. Algorithms identify who's least likely to switch providers and price renewals accordingly.

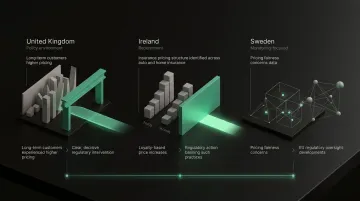

Quantified impact across Europe:

| Jurisdiction | Penalty | Regulatory Action |

|---|---|---|

| UK | 6 million loyal customers overpaid ca. 10,4 milliarder DKK in 2018 | Banned price walking (Jan 2022), estimated to save ca. 36,5 milliarder DKK over 10 years |

| Ireland | Customers of 9+ years paid 14% more for auto, 32% more for home insurance | Banned price walking (July 2022) |

| Sweden | Loyal policyholders subjected to "unmotivated and unfair" price increases | Monitoring EU developments |

Why this happens: AI models predict which customers will auto-renew regardless of price increases. If you've been with the same insurer for years and never shopped around, the algorithm knows—and your premium reflects it.

Opaque Pricing and Transparency Problems

When AI sets a price, the reasoning can be nearly impossible to explain or challenge:

- Consumer experience: 76% of consumers experienced premium increases, but only 18% could link the increase to changes in their personal situation

- The gap: Most policyholders don't understand why their renewal jumped 8-15% when nothing changed

This creates a transparency problem: you have the right to ask why your premium increased, but insurers may struggle to explain decisions made by complex AI models.

Regulatory Dimension

The opacity problem is precisely why regulators have moved to set guardrails. EU and Danish frameworks are increasingly specific:

- GDPR Article 22: Grants the right not to be subject to decisions based solely on automated processing that produce significant effects, unless necessary for a contract

- EU AI Act: Classifies AI for life and health insurance risk assessment as high-risk, requiring strict governance

- Danish Finanstilsynet (2024): Requires companies to document the balance between model performance and explainability, especially when rejecting claims

Enforcement is still catching up with practice — but Danish consumers already have documented rights to challenge AI-driven pricing decisions under GDPR, and those rights are expanding.

Faster Claims, Smarter Fraud Detection

Simple Claims, Near-Instant Resolution

For straightforward claims, AI delivers genuine speed:

- Admiral Seguros (Spain): Processed 12,000 touchless property and vehicle claims in 2021, with 98% completed in under 15 minutes

- Beesafe (Poland): Uses Tractable AI to assess damage in seconds, making immediate payment offers during the first interaction

- If Insurance (Denmark): Photo inspection service used 71,819 times in 2025, with 64% of customers reporting claims digitally

Consumer benefit: Minor home damage, delayed luggage, or travel claims now resolve in hours instead of days.

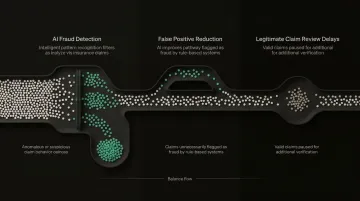

Fraud Detection and False Positives

AI fraud detection lowers costs overall — but false positives can delay your legitimate claim:

- A 2025 study analyzing 75,000 insurance claims found AI achieved 92.5% accuracy in fraud detection

- The same system reduced false positives by 31% compared to rule-based systems

- Still, your legitimate claim might be flagged as suspicious and delayed

Recommendation: Document claims thoroughly with photos, receipts, and detailed descriptions to reduce false positive risk.

Human Oversight Still Matters

For complex claims — injuries, disputed coverage, or significant property damage — human adjusters remain essential:

- AI assists by summarizing documents and flagging patterns

- Final decisions still involve people

- You have the right under GDPR to request human review of automated decisions

Knowing when to ask for human review — and what your rights are — is as important as understanding how the automated system works in the first place.

The Risks: Where AI Can Work Against You

Bias and Discrimination Risk

AI models are trained on historical data, which may embed historical biases:

- Sweden's welfare fraud AI was suspended in 2024 after investigations found it disproportionately flagged women, people with foreign backgrounds, low-income earners, and those without university degrees

- Allstate paid 175 millioner DKK to settle allegations of using "price optimization" to overcharge safe, loyal customers by ca. 7,2 milliarder DKK between 2012 and 2021

Geographic location, property age, and demographic correlations embedded in historical data can leave certain groups systematically overpriced — with no clear explanation provided.

Data Privacy Concerns

AI depends on extensive personal data collection:

What insurers collect:

- Property images and floor plans

- Driving behavior (speed, braking, acceleration)

- Behavioral signals (click patterns, time spent reviewing quotes)

- Location data and travel patterns

Your GDPR rights:

- Access what data is collected about you

- Correct inaccurate information

- Limit how your data is processed by automated systems

- Request human review of automated decisions

Action step: Don't assume compliance. Ask your insurer directly about their data practices and exercise your rights.

AI Errors and Their Consequences

AI can misread images, misclassify risk, or reach incorrect underwriting decisions — and the consequences can be significant:

- A US court allowed discovery into whether an insurer used AI to override physician judgment, ruling that denying a claim via AI with minimal human review could constitute bad faith

- A lawsuit against UnitedHealthcare found that 90% of claim denials generated by its "nH Predict" algorithm were reversed on appeal

Always review automated decisions carefully. Under Danish and EU law, you have the right to request human review of any decision made about you by an automated system.

How Consumers Can Use AI to Fight Back

AI isn't exclusively in the insurer's hands anymore. You now have access to AI-powered tools that put policy analysis, market pricing, and coverage audits directly in your hands.

The Problem Consumer Tools Solve

Most policyholders:

- Don't read insurance fine print

- Don't know the actual market rate for their coverage

- Aren't alerted when loyalty premiums quietly inflate annual costs

- Miss coverage gaps until they file a claim

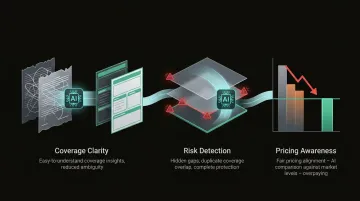

AI can do this automatically—analyzing policies, identifying gaps, and benchmarking prices against the real market in seconds. One platform built specifically for Danish consumers does exactly that.

Inzure: Independent AI for Danish Consumers

Inzure is Denmark's first independent AI-driven insurance platform that reads and analyzes policies across all Danish insurers in 60 seconds.

How it works:

- Submit your policy documents as PDFs or photos from any insurance company

- The platform reads the fine print, extracts coverage details, and compares your pricing against the broader Danish market

- Receive a full analysis flagging coverage gaps, duplicate policies, and unwarranted price increases

Key difference: Unlike insurer-owned chatbots that work for the insurance company, Inzure is fully independent and works for you.

Documented savings: Early users have saved between 2.800 kr and 48.000 kr annually:

- Lise Nielsen (86): Discovered she had no home insurance for 10 years, added coverage, and still saved 2.800 kr/year (24% reduction)

- Hans Henrik Beck (62): 8-year Tryg customer achieved 46% premium reduction, saving 48.000 kr/year

- Thomas Stolborg (58): Achieved 35% reduction, saving 25.000 kr annually

Practical Consumer Action Steps

Compare before auto-renewing. Check your renewal price against market rates first. A 2024 Statistics Denmark study found the average Danish household spent 22.281 kr on insurance—your current price may be well above that.

Ask your insurer to explain any premium increases. Under GDPR, you have the right to understand automated pricing decisions. If nothing changed in your situation, demand a clear answer.

Run an independent AI analysis. Platforms like Inzure audit your coverage and overpayments without bias toward any specific insurer. The analysis is free—you only pay (20% of savings) if you switch and save money.

Check for duplicate coverage. Travel insurance is often already bundled into credit card policies, employee benefits, or bank accounts. AI tools flag these overlaps in seconds.

Shop around every two years. Danish consumer authorities recommend comparing prices at least every two years to avoid loyalty penalties—what used to take 10 hours now takes 60 seconds.

Frequently Asked Questions

Do insurance companies use AI for underwriting?

Yes, most major insurers already use AI in underwriting to assess individual risk profiles faster and with more data points than traditional methods. This includes analyzing property images, driving behavior via telematics, and behavioral signals like how long you spend reviewing quotes.

Can you use AI for car insurance?

AI is widely used in car insurance for pricing (including telematics-based driving behavior analysis), claims assessment (photo-based damage evaluation), and fraud detection. Independent AI tools also exist to help consumers compare premiums across Danish providers for many types of coverage.

Will AI make my insurance cheaper or more expensive?

It depends on your individual risk profile. AI enables more precise pricing, which can lower premiums for low-risk policyholders but raise them for others. Loyal customers who don't shop around face the greatest risk of being overcharged—research across European markets suggests loyal customers can pay 20–40% more than new customers for identical coverage.

Can AI deny my insurance claim?

While AI can flag or initially assess claims, final decisions—especially on complex or disputed claims—still involve human review. Consumers in Denmark have the right to request human oversight of automated decisions under GDPR Article 22.

Is my personal data safe when insurers use AI?

GDPR gives Danish consumers the right to know what data is collected, how it's used in automated decisions, and request corrections if it's inaccurate. That said, actively ask your insurer about their data practices rather than assuming compliance.

How can I tell if I'm overpaying for insurance because of AI pricing?

Compare your renewal price against independent market benchmarks, look for unexplained year-on-year increases, and use independent AI-driven tools to audit your policies against current market rates. If you've been with the same insurer for 5+ years without shopping around, there's a high probability you're paying a loyalty penalty.

Final Thought: Insurers are already using AI to price, assess, and segment you. The practical step is using independent tools to check whether what you're paying reflects your actual risk—or just how long you've stayed put.